Re-energising Europe’s global green reach

Giovanni Sgaravatti is a Research Analyst, Simone Tagliapietra a Senior Fellow, and Cecilia Trasi a Research Analyst, all at Bruegel

Executive summary

The goals of decarbonisation, competitiveness and strategic autonomy will underpin the implementation of the European Green Deal during the 2024-2029 European Union institutional cycle. To strike the right balance between these sometimes conflicting objectives, EU policymakers should focus on both domestic and international aspects of the Green Deal.

Domestically, they must ensure implementation of the agreed climate plan, avoiding inaction or delay. Internationally, they must establish a new green-diplomacy and partnerships strategy, which will support global decarbonisation while addressing competitiveness and strategic autonomy concerns.

The current EU approach to green diplomacy is uncoordinated, lacking a clear strategy and appropriate resources. Given the EU’s limited share of annual global emissions, supporting decarbonisation abroad is fundamental to meet the global net zero emissions goal. The EU’s green diplomacy and partnerships need to be strengthened and expanded in a pragmatic and coherent manner.

The main priorities include focusing on the implementation of international emissions reduction pledges, a new diplomatic push for carbon pricing and international green taxation, the creation of streamlined partnerships for green industrialisation with major partner countries and the promotion of new global trade and climate agreements. To succeed in these, a revision of the current governance of EU global green action will be required.

1. Why the EU needs a clear global green reach strategy

The need to reduce global greenhouse gas emissions is becoming ever more pressing. The remaining carbon budget consistent with limiting global warming to 1.5 degrees Celsius above pre-industrial levels is shrinking rapidly, estimated at 200 gigatonnes of carbon dioxide in early 2024, down 60 percent from the 500 gigatonnes estimated in 2020 (Forster et al 2024).

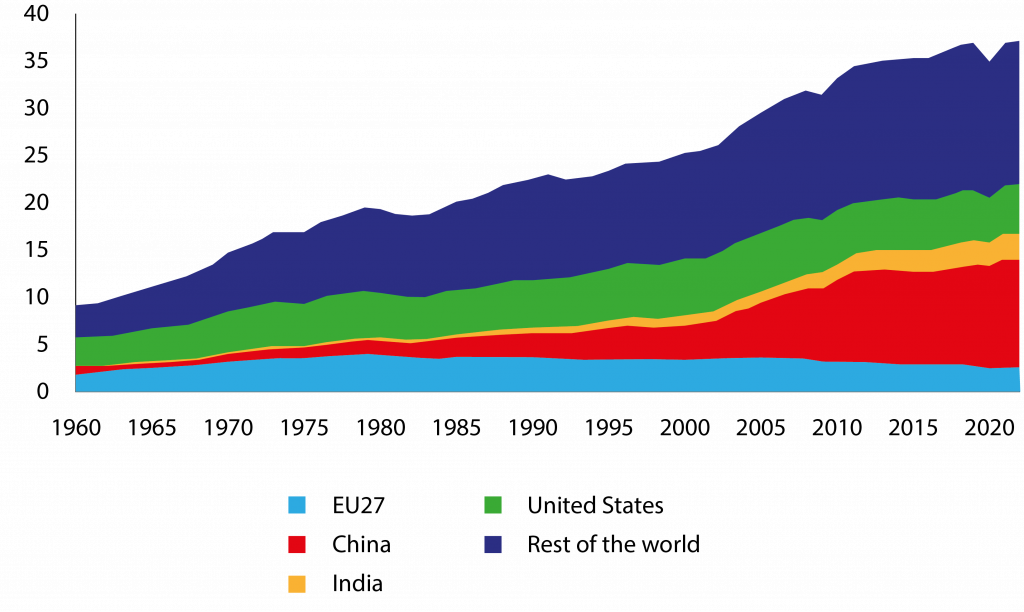

The European Union’s annual emissions are only about 7 percent of the world total (Figure 1) but the EU nevertheless seeks to foster global decarbonisation by leading by example with domestic action. This however is not enough. The EU must also develop a stronger external strategy to foster international green collaboration and collective climate action.

The EU must also maximise the effectiveness of its global green reach strategy because all countries are required to present their updated Nationally Determined Contributions (NDCs) ahead of the United Nations climate summit (COP30) in 2025.

These will outline national emissions-reduction plans up to 2035 and will determine to a great extent whether the world can get onto an emissions trajectory in line with the goals of the Paris Agreement. These updates have been called “the most important documents to be produced in a multilateral context so far this century.”1

The EU should work to catalyse action and help turn the NDCs into workable national green-transition plans. In the case of emerging markets and developing economies (EMDEs), goals might be linked to international climate finance disbursements. To play a meaningful role, the EU’s green reach strategy will need to use a broad range of levers – trade, economic and financial – to build equitable partnerships that will help partners make deeper emissions cuts.

Figure 1. Global CO2 emissions 1960-2022 (GtCO2)

Note: Cumulative emissions are the sum of CO2 emissions produced from fossil fuels and industry. Land use and land-use change is not included.

Source: Bruegel based on Our World in Data, Global Carbon Budget and IPCC.

The EU has already identified four main drivers for its green diplomacy (Council of the EU, 2024): 1) supporting multilateralism with an emphasis on Paris Agreement implementation, 2) addressing the repercussions of climate change for global peace and security, 3) driving local efforts while raising global ambitions, and 4) enhancing international climate cooperation through comprehensive advocacy and outreach.

In practice, there are additional motivations, including: 5) anticipating the repercussions of the EU’s domestic actions on trade partners, 6) promoting European clean-tech exports and foreign green investment, and 7) projecting soft power by shaping the international climate agenda.

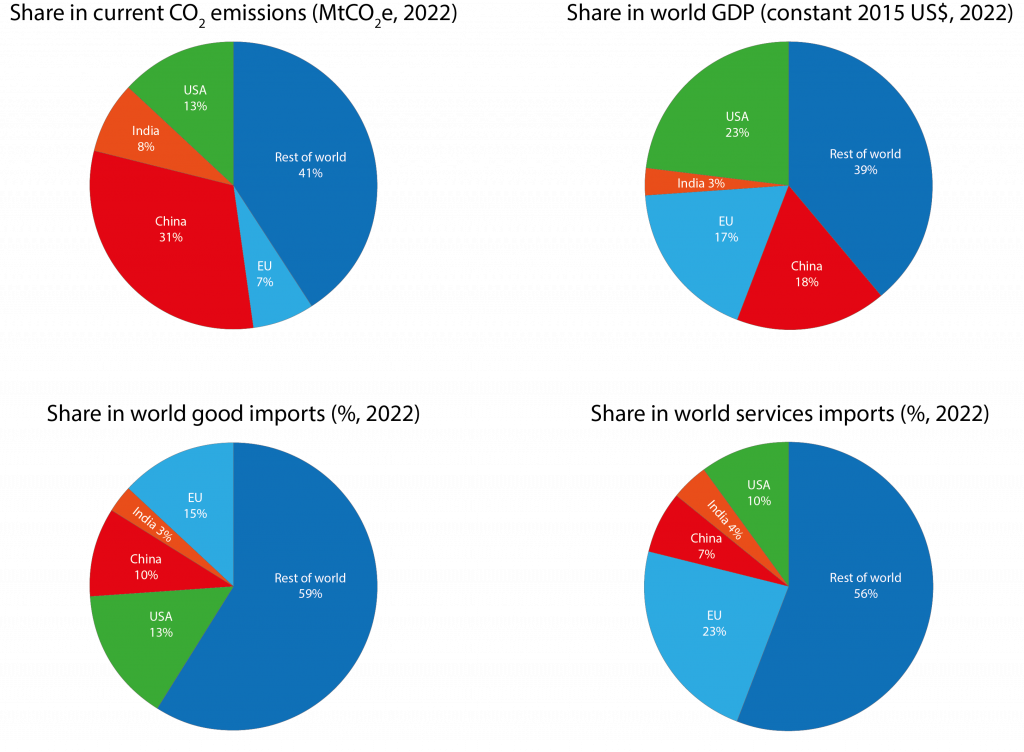

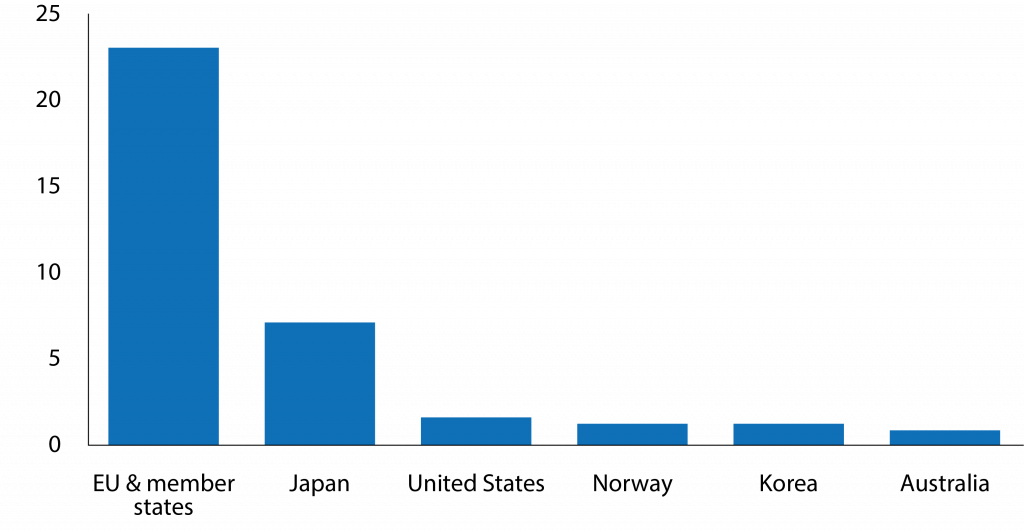

These considerations are both legitimate and unavoidable. The EU accounts for 17 percent of global GDP, 15 percent of the global goods trade and 23 percent of global services trade (Figure 2). The EU’s push for domestic decarbonisation has repercussions for trade partners worldwide, which need to be adequately addressed. The EU’s large share of global trade is also important leverage that can be used to promote green growth domestically and in partner countries.

Figure 2. EU shares of global emissions, GDP and trade (%, 2022)

Notes: CO2 emissions refer to the use of coal, oil and gas (combustion and industrial processes), gas flaring and the manufacture of cement. GDP is expressed in constant 2015 dollars.

Source: Bruegel based on Global Carbon Budget, World Bank, WTO.

The urgency of an effective EU global green reach strategy is further emphasised by the EU’s gradually eroding influence in several regions, especially the Global South. Mistrust, accusations of hypocrisy and shifting power dynamics all contribute to this erosion. There is growing scepticism from EMDEs about Western initiatives, including those spearheaded by the EU. The EU also faces accusations of climate hypocrisy, a sentiment exacerbated in the 2022 energy crisis, when the EU gave out mixed signals on the role of gas in the transition.

Meanwhile, the geopolitical landscape is being reconfigured, with nations including Brazil, India and the Gulf countries seeking greater strategic autonomy and becoming less inclined to align with Western powers. The EU needs to recalibrate accordingly.

This policy brief sets out a framework for doing this. It first discusses the shifting drivers of EU green diplomacy and partnerships. Second, it evaluates the current EU green-diplomacy architecture. Third, it identifies limitations within this framework. It then offers recommendations on addressing these shortcomings and advancing a new EU global green reach strategy.

2. The shifting drivers of EU green external action

EU green external action is being influenced by two new factors: 1) the need to manage the repercussions for trade partners of its own domestic actions, and 2) the need to take into account the priorities of competitiveness and strategic autonomy, alongside decarbonisation.

2.1 Managing the repercussions for trade partners of EU domestic actions

The European Green Deal – the EU’s overarching plan to achieve net-zero emissions by 2050 – has generated an unprecedented wave of legislation to foster the necessary transformation of the European economy. Assuming the Green Deal is implemented as planned, the implications of this work will increasingly become visible, both domestically and internationally.

Three examples of how the European Green Deal will tangibly impact trade partners in the near future are: 1) the entry into full force of the Carbon Border Adjustment Mechanism (CBAM), 2) the reduced need for oil and gas imports, and 3) the increasing need for critical raw materials (Leonard et al 2021).

CBAM has been introduced to complement the EU emissions trading system by imposing a charge on the carbon content of selected carbon-intensive imports2, thereby mirroring the domestic cost of carbon in the EU. This has been done to prevent carbon leakage – the relocation of industry to less environmentally regulated jurisdictions – as free carbon allowances for EU industry are phased out. The CBAM pilot phase started on 1 October 2023, with full entry into force in January 2026.

CBAM is one of the most internationally contested measures approved under the European Green Deal. The period ahead of its full application will likely be marked by increased political and trade tension between the EU and partners. Managing these tensions will require much stronger ‘CBAM diplomacy’ and more joined-up application of EU trade, climate and development policy instruments when dealing with partner countries affected by CBAM.

Meanwhile, in 2022, the EU’s shares of worldwide oil and gas demand were, respectively, 11 percent and 9 percent (Energy Institute, 2023). But EU demand for oil and gas is expected to drop from about 800 million tonnes per year in 2022, to 650 million tonnes in 2030 and 330 million tonnes in 2050 (IEA, 2023).

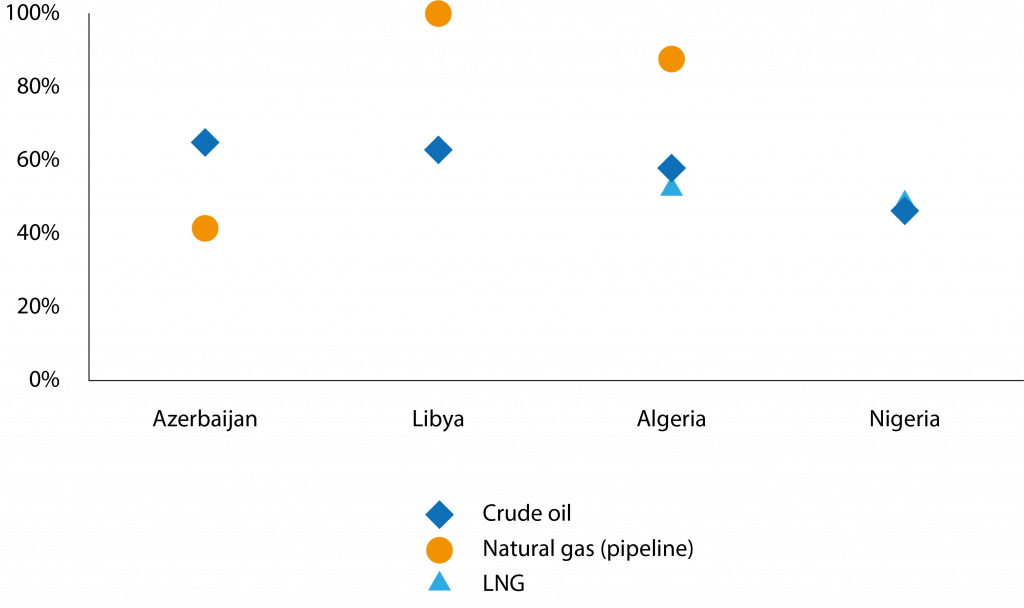

Reduced demand from the EU is likely to lower global oil and gas prices, reducing the revenues of major exporters. This could directly affect the EU’s main fuel suppliers, including Algeria, Azerbaijan, Libya and Nigeria, potentially destabilising these countries economically and politically (Figure 3). Managing these consequences will require renewed, stronger EU external action.

Figure 3. Shares of oil and gas exports going to the EU from selected exporting countries (%, 2020-2021)

Note: Crude oil exports are to OECD Europe. Crude oil and LNG exports refer to 2020; natural gas exports by pipeline to 2021.

Source: Bruegel based on EIA Country Profiles and BP’s Statistical Review of World Energy 2022.

The green transition also implies heightened demand for clean technologies and the raw materials used in them. A clean-energy system is much more minerals- and metals-intensive than a conventional fossil-fuel energy system.

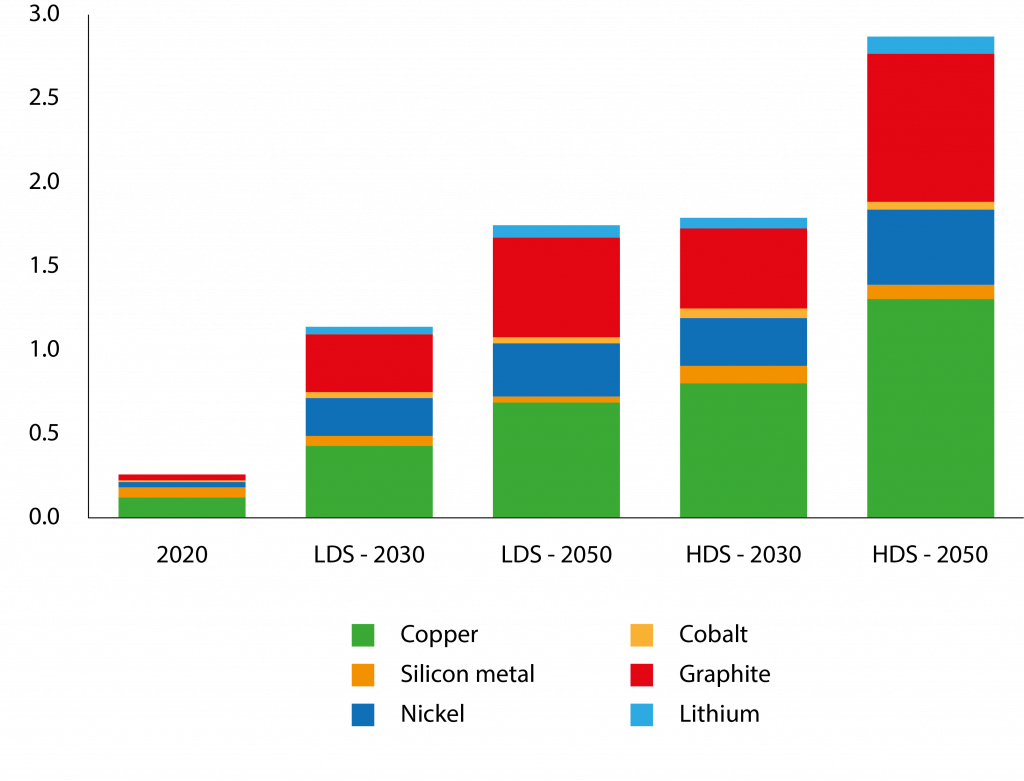

Even with increased circularity in use and reuse of resources, the implications are enormous for the extraction of raw materials and for global competition to secure access to them. EU demand for critical raw materials (CRMs) up to 2030 and 2050 can be expected to increase substantially.

EU demand for some of the most used raw materials, including copper, silicon metal, nickel, manganese and lithium, is expected to increase elevenfold3 by 2050 (Figure 4) (Carrara et al 2023). Meeting this surging demand in a secure and affordable manner requires third-country partnerships that effectively incentivise investment from the private sector.

Figure 4. Selected materials demand forecast in the EU (Mt/y, 2030 vs 2050)

Note: Forecasts of material demand in low-demand and high-demand scenarios (LDS/HDS) for 2030 and 2050 for all sectors.

Source: Bruegel on Carrara et al (2023).

2.2 Addressing the new priorities of competitiveness and strategic autonomy alongside decarbonisation

Competitiveness and strategic autonomy, alongside decarbonisation, have become critical priorities for the EU and are set to determine the strategy for the next five years.

Developments including the United States Inflation Reduction Act and China’s predominance in cheap solar panels and electric vehicles highlight the competition and security concerns in the clean-tech race. For example, while the Inflation Reduction Act will likely benefit emission reductions at the global level, its local content requirements pose significant challenges to the EU’s industrial competitiveness (Kleimann et al 2023).

Similarly, very cheap solar panels and EVs produced in China are a boon to global climate mitigation efforts but create competitiveness and security concerns, both in the EU and the US.

The EU’s main policy responses are the Net-Zero Industry Act4 and the European Critical Raw Materials Act5. However, these laws have been criticised for being protectionist in spirit and for potentially delivering only marginal results (Le Mouel and Poitiers, 2023; Tagliapietra et al 2023).

Any further EU green industrial policy legislation during the new EU institutional cycle (2024-2029), should have both domestic and external parts. While developing the external part, the main question for the EU will be how to prioritise collaboration with which countries, taking into account the complex interplay between decarbonisation, competitiveness and strategic autonomy, and the potential trade-offs between them.

The war in Ukraine has highlighted EU dependence on external suppliers, prompting a shift from economic efficiency and open trade to an emphasis on economic security, reflected in the European Economic Security Strategy published in June 2023 (European Commission, 2023).

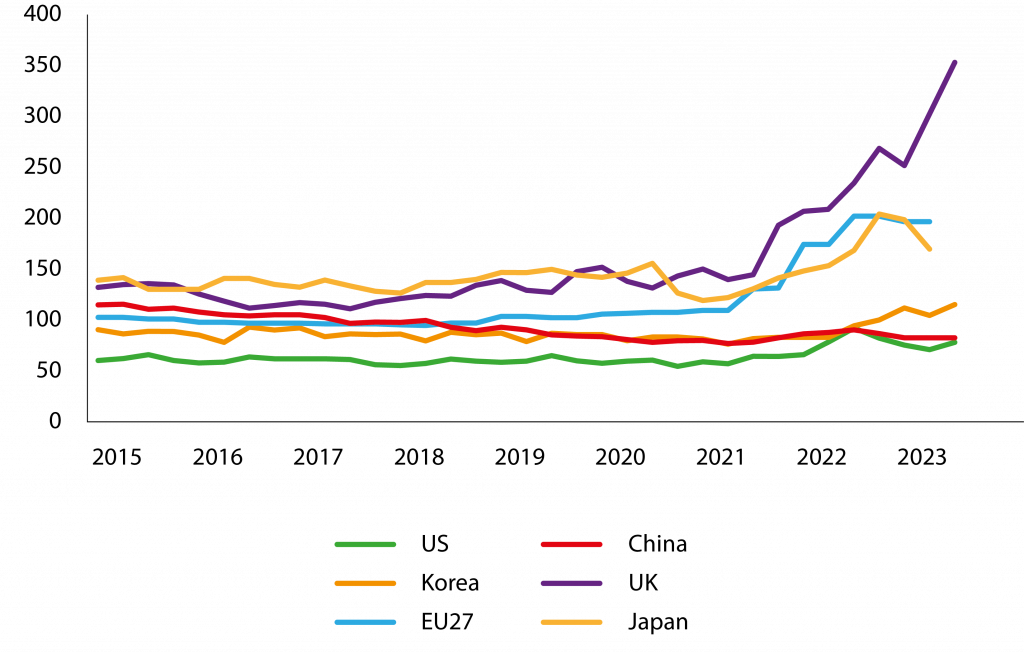

Meanwhile, rising energy prices between summer 2021 and summer 2023 raised questions about the economic viability of energy-intensive industries within the EU (Figure 5).

Figure 5. Industrial retail electricity prices (€/MWh, quarterly averages, 2015-2023)

Note: European Central Bank conversion rates.

Source: Chief Economist Team/DG ENER/European Commission.

Yet the normalisation of energy prices since 2023 has not resulted in a recovery in industrial production in major energy-intensive sectors. Notable declines in production levels have been seen compared to 2021, with basic metals down by 22 percent, non-metallic minerals down by 12 percent, iron and steel down by 17 percent and non-ferrous metals down by 14 percent. For energy-intensive industries, the energy shock in Europe increased the attractiveness of countries with low energy prices.

During the energy crisis, governments managed to contain relocation of energy-intensive production abroad only by providing massive subsidies, with Germany providing €71 billion in state aid to its domestic companies in 2022 alone (Cannas et al 2023).

Notwithstanding subsidies, some relocation is happening; German chemical giant BASF, for example, announced in 2023 the closure of its ammonia plants in Ludwigshafen and of other chemical units, partly because of high energy costs6.

Instead of authorising expensive and often ineffective subsidies (Losz and Corbeau, 2024), the EU might, as part of its green diplomacy push, want to help establish international green value chains. This would mean the relocation of certain energy-intensive production processes abroad to countries with abundant renewable energy resources – starting with countries in North Africa.

Such a strategy could be a better approach than massive investments in importing green hydrogen7 or cheap electricity8, and would not have the new-colonialism aftertaste of natural resources exploitation. For example, importing a tonne of green ammonia would be much easier than importing the equivalent amount of hydrogen needed to produce that one ton of green ammonia (Moritz et al 2023).

The potential savings obtained by some energy-intensive industries through relocation are sizable. Better access to natural resources, including renewable energy, could cut green industrial production costs by as much as 18 percent for steel, 32 percent for urea and 38 percent for ethylene (Verpoort et al 2024).

This is because operational costs for renewables are very low and in countries with high solar irradiation capacity and wind power density, energy production is cheaper than in countries where the sun does not shine and the wind does not blow as much, and their cheaper electricity prices trickle down in the form of cheaper green-energy-intensive commodities.

While relocation is politically very difficult to support, guiding it would help contain it to only some production processes, for which the repercussions on employment and value added would not be very sizable (Sgaravatti et al 2023).

An EU strategy to import more intermediate energy-intensive products while focusing on higher value-added goods would reduce production costs and in turn emissions, as cheaper green products reduce the green premium companies and consumers need to pay, fostering sales.

This would also offer an industrialisation pathway for EMDEs seeking to move up the supply chain – for example moving from the extraction of minerals to refining and manufacturing of intermediate products – and to retain more value domestically.

All in all, to manage these two new factors, the EU will need to revise and strengthen its global green reach toolkit. In the following, we describe the current toolkit, illustrate its main shortcomings and propose a new geoeconomic plan.

The 2024-2029 institutional cycle provides an opportunity for the EU to solidify its leadership and drive transformative change in global green diplomacy and partnerships

3. EU green global reach: the current toolkit

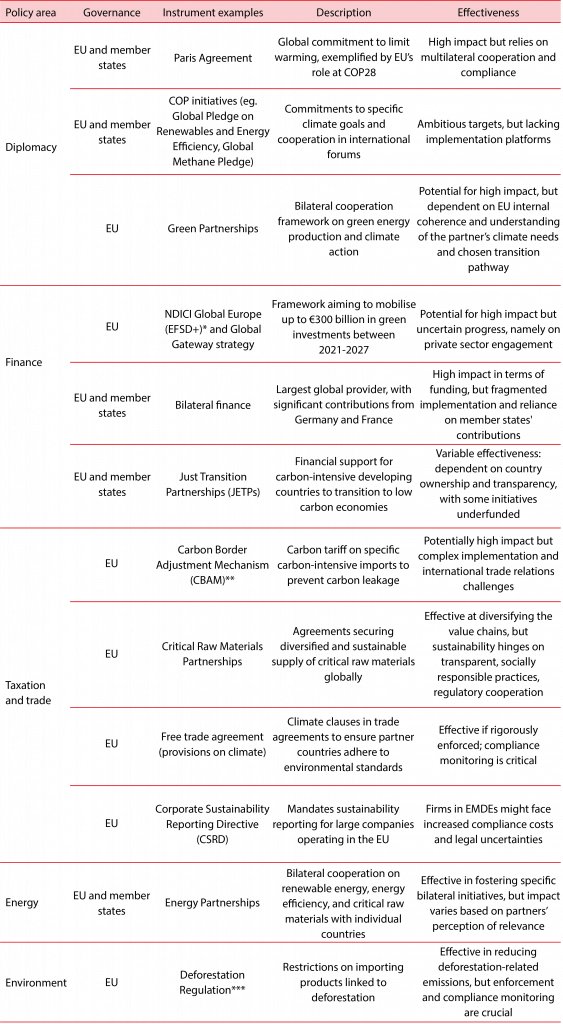

To achieve its green diplomacy and partnerships goals, the EU has progressively developed a complex architecture that extends beyond traditional climate diplomacy, incorporating financial instruments, trade regulations, taxation and energy agreements (see the annex).

This framework includes adherence to international commitments on emissions, climate finance, climate-related provisions in trade agreements and the proliferation of different sorts of bilateral partnerships.

At the heart of the EU’s green diplomacy and partnerships efforts lies the Paris Agreement. The EU’s commitment9 to limiting global warming through multilateral action is shown by its role at COP28 at the end of 2023 in Dubai, where it promoted and facilitated the Global Pledge on Renewable Energy Sources and Energy Efficiency10.

Countries at COP28 pledged to collaborate to triple installed renewable energy capacity to 11,000 gigawatts by 2030 (for comparison, total global electricity capacity in 2022 was 8,900 GW11) and to double the global average annual rate of energy efficiency improvements to 4 percent by 2030.

Bilaterally, the EU engages in different types of strategic partnership: energy, green and critical raw materials partnerships. Energy partnerships promote bilateral cooperation on renewable energy and energy efficiency, extending to hydrogen and critical raw materials, promoting green practices in industries including steel and aluminium production.

Green Partnerships are bilateral frameworks designed to enhance cooperation between the EU and major partners on green-energy production and climate action. For example, the partnership with Morocco12 aims to diversify the EU energy supply and restructure value chains, while the partnership with Korea13 promotes cooperation in climate finance to support developing countries in implementing climate policies. It also facilitates cooperation on adaptation, carbon pricing and methane emissions.

Finally, partnerships for critical raw materials are trade and investment agreements between the EU and third countries aimed at diversifying and securing the EU’s supply of essential materials through cooperation on extraction, processing and recycling. Such partnerships include those with Argentina14, Australia15, Canada16, Chile17, Namibia18, Norway19, Kazakhstan20, Ukraine21, the Democratic Republic of Congo and Zambia22.

The principle of common but differentiated responsibilities, central to the Paris Agreement, is reflected in the climate finance pledge made by rich nations to EMDEs. At COP15 in Copenhagen in 2009, developed countries committed to a collective goal of mobilising $100 billion per year by 2020 for climate action in developing countries, a goal which was formalised at COP16 in Cancun and reiterated at COP21 in Paris.

Although this target was not met by 2020, it was in 2022 with the mobilisation of $115.9 billion, up from $89.7 billion in 2021 (OECD, 2024).

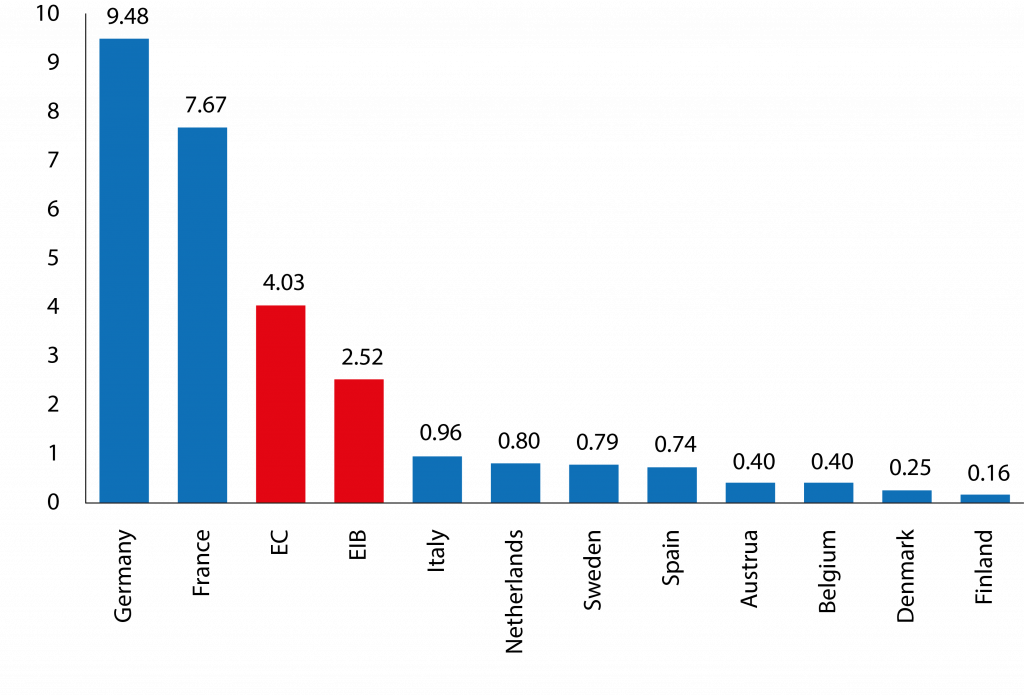

The EU is the largest provider of climate finance globally (Figure 6). In 2022, the EU and its member states collectively allocated €28.4 billion to climate finance, and mobilised an additional €11.9 billion from the private sector23 (EEA, 2023). The provision of climate finance is primarily national: Germany and France contributed €9.5 billion and €7.7 billion respectively, while the EU from its own funds contributed €6.5 billion (Figure 7).

Figure 6. Top providers of climate finance (€ billions, 2021)

Note: Figures include climate-related development finance from bilateral and multilateral contributions. Both concessional and non-concessional activities are included. Guarantees are excluded. We use 2021 data for consistency between EEA and OECD estimates.

Source: Bruegel based on European Environment Agency and OECD DAC.

Figure 7. EU climate finance by provider (€ billions, 2022)

Note: The figures refer to climate finance provided to developing countries as reported by to the EEA by EU countries. The bars in red indicate the EU institutions, the bars in blue the member states. Only the top ten member-state providers are shown.

Source: Bruegel based on European Environment Agency.

The EU’s so-called Team Europe Initiatives approach24 pools resources and expertise from member states and EU institutions, underpinning the Global Gateway strategy25, which aims to mobilise up to €300 billion in investment to support projects worldwide in green infrastructure, digitalisation, transport, health, education and research (European Commission, 2021).

The Just Transition Partnerships (JETPs), launched at COP26 in 2021, provide tailored financial assistance to specific countries, combining public and private funding from G7 countries to support power-sector decarbonisation strategies.

Current agreements include South Africa, worth approximately $8.5 billion, Vietnam, worth $15.5 billion, Indonesia, worth $20 billion and Senegal, worth €2.5 billion. Proposals for JETPs in other countries are under consideration. JETPs are primarily funded by France, Germany, the United Kingdom, the US and the EU, with significant involvement from development banks.

These agreements are country-specific, ensuring they are context-sensitive. While JETPs are promising, their effectiveness is hampered by insufficient ambition, inadequate funding, a lack of explicit policy-action links and the need for improved governance and monitoring frameworks (Bolton et al 2024).

4. Main shortcomings of the current toolkit

While the EU has asserted a strong presence in international climate negotiations, its capability to move beyond ambitious rhetoric and target-setting in order to steer implementation at global level remains unclear.

Evaluating the barriers to effective implementation is crucial. There are essentially two: 1) fragmentation of the current architecture; 2) deficiencies in implementation of bilateral and multilateral agreements of varying nature.

4.1 Fragmentation of the current architecture

At EU level, governance fragmentation within the European Commission itself represents a significant challenge. Several directorates-general (DGs) are responsible for different parts of the EU global-reach architecture: Climate Action (DG CLIMA) oversees climate negotiations; Energy (DG ENER) is responsible for international energy partnerships; Environment (DG ENV) works on deforestation; International Partnerships (DG INTPA) manages development finance (a primary source of EU climate finance); Internal Market, Industry, Entrepreneurship and SMEs (DG GROW) is in charge of the critical raw material partnerships; Taxation and Customs Union (DG TAXUD) manages CBAM; Trade (DG TRADE) handles trade-related issues; and finally the European External Action Service (EEAS) houses a Special Envoy for Climate and Environment Diplomacy.

While this division of responsibilities is understandable, it might lead to coordination difficulties and a compartmentalised approach, often undermining both domestic and international policy coherence (Oberthür and Dupont, 2021).

Moreover, the lack of an integrated vision across these DGs risks creating confusion in third countries that might deal with different officials for different policy areas at the same time (eg. development and trade).

However, the role of the EU is significantly limited compared to the flexibility of individual countries and faces coordination challenges arising from the differing priorities of EU countries. These also affect the Team Europe Initiatives (TEIs), where the lack of clarity in goals, funding, timelines and long-term operational value leads to disjointed efforts.

The misalignment of various components within TEIs reduces their collective impact, making it challenging to coordinate and synergise actions across different EU member states and their respective initiatives. Ensuring inclusiveness in TEIs, given the varying capacities of member states to co-finance and fully participate, remains a significant challenge (Keijzer et al 2023).

Additionally, mobilising private investment for infrastructure projects in EMDEs often encounters obstacles of both financial and regulatory nature, a problem also faced by similar initiatives such as the US’s Partnership for Global Infrastructure and Investment.

4.2 Implementation deficiencies

Lack of coherence and failure to include local stakeholders fuels scepticism of, and resistance to, EU green policies in third countries. EU policies are often perceived as unilaterally imposed trade barriers rather than collaborative efforts in favour of a greener economy.

While the extent of the damage imposed by these regulations on third countries is debatable, the common problem with them is often their perceived protectionist nature at the expense of third countries – prompting observers to condemn a ‘neo-colonialist approach’26.

For example, CBAM raises concerns about its impact on international trade, especially among the main exporters of carbon-intensive goods to the EU. Countries including China, the UK and the US are top exporters of CBAM-covered products to the EU, but the mechanism’s impact varies depending on each country’s economic reliance on exports to the EU and how carbon-intense their exports are (Overland and Sabyrbekov, 2022).

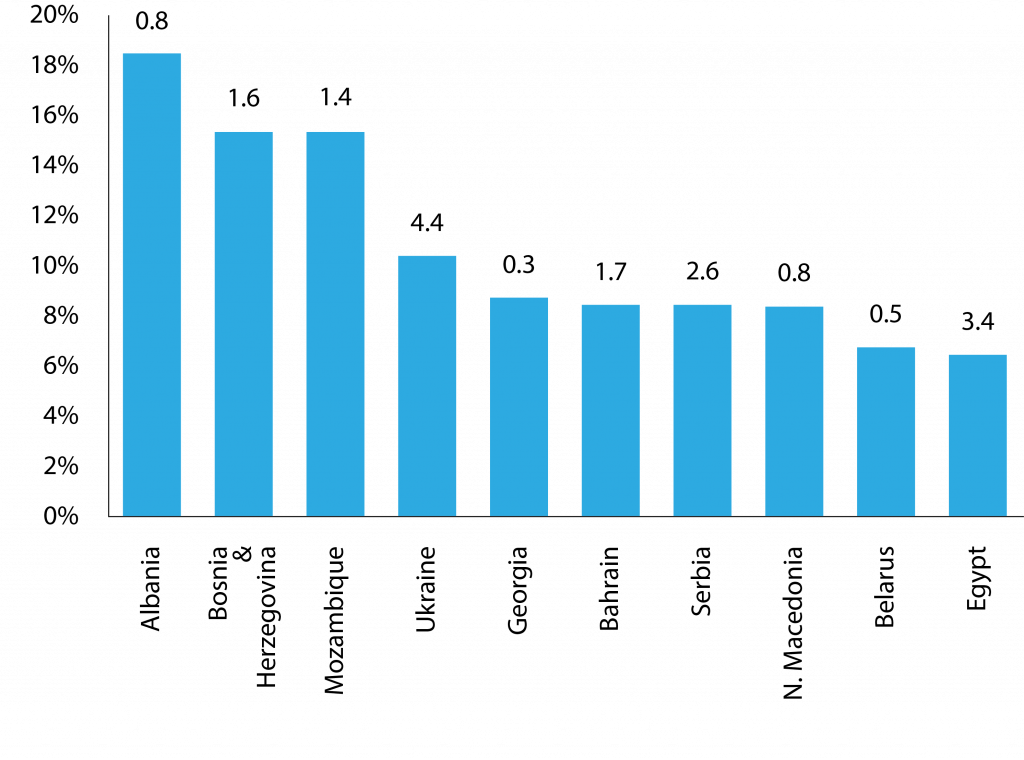

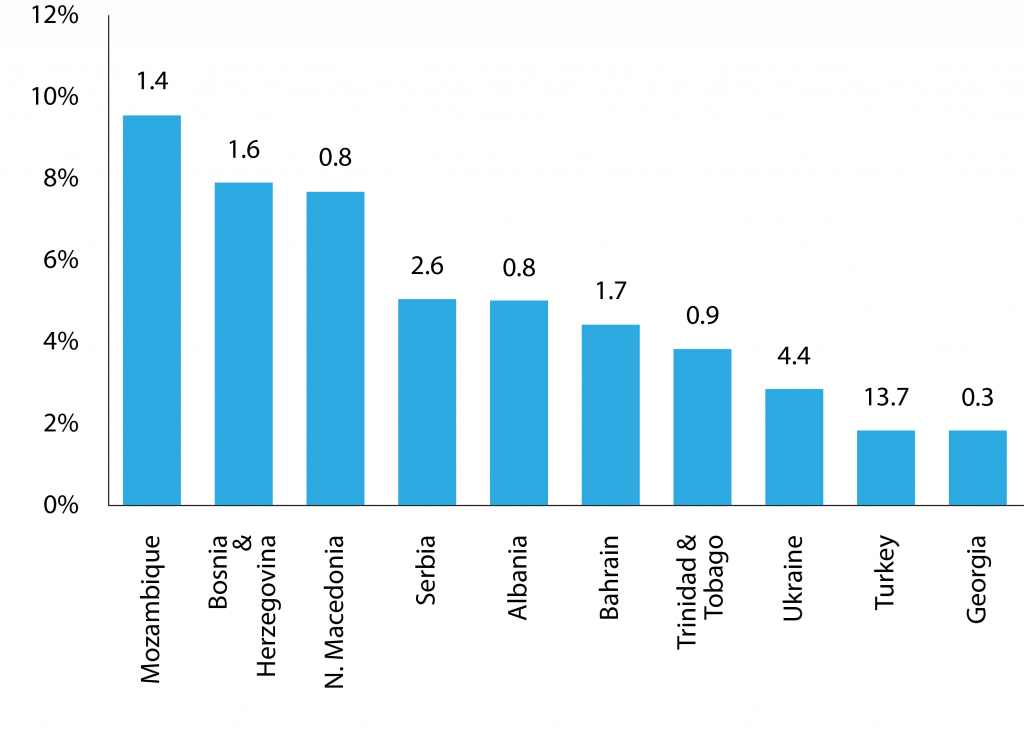

Smaller economies, such as Mozambique, which relies heavily on aluminium exports (Magacho et al 2022), are particularly vulnerable. Depending on the weight of the EU market in their total exports and the possibility for countries to re-route the affected exports, Western Balkan countries, Mozambique, Bahrain and Ukraine are likely to be most exposed to CBAM (Figure 8).

Figure 8. CBAM exports to the EU as percentage of total exports (top panel) and GDP (bottom panel), $ billions, 2022

Note: Countries with CBAM exports to the EU lower than 300,000 tons are omitted. Figures at the top of the bar show absolute values in $ billions.

Source: Bruegel based on CBAM regulation and CEPII’s dataset BACI.

Other Green Deal regulations also face resistance from third countries, affecting international trade relations. The inclusion of emissions from maritime shipping in the EU emissions trading system applies to large ships departing from and arriving at EU ports, regardless of their flag. Non-EU shipping companies argue that this should be addressed at the level of the International Maritime Organisation to ensure fair competition across the industry.

Additionally, concerns have arisen about the allocation of money generated by the scheme, with some advocating for reinvestment in R&D to facilitate technological and infrastructure improvements supporting industry-wide decarbonisation27.

The Corporate Sustainability Reporting Directive (CSRD, Directive (EU) 2022/2464), meanwhile, requires businesses to disclose the social and environmental impacts of their activities, imposing significant compliance burdens on both EU and non-EU firms.

The EU regulation on deforestation-free products (Regulation (EU) 2023/1115) requires products entering the EU market to not contribute to deforestation, posing challenges for developing countries where agriculture is a major source of employment, and prompting a reaction from WTO members concerned that the regulation disregarded local conditions28.

Similarly, the EU Farm to Fork Strategy on sustainable food systems has raised concerns about its impact on global food prices and food security (Dekeyser and Woolfrey, 2021).

These measures have sound climate and environment goals that can result in European and global benefits. To clean up production processes that serve European markets, EU legislation will inevitably affect also non-EU parts of the supply chain.

Therefore, such measures have value in themselves, but need better communication and dialogue with third countries, providing partner countries and businesses with the know-how and technological expertise needed to manage the transition to greener production methods.

Then, despite the EU’s position as the primary provider of climate finance, the actual impact of EU financial flows for climate adaptation and mitigation has yet to be assessed, leaving open questions about where and how to better direct climate finance.

The new European Commission for 2024-2029 will inherit both the strides made and the challenges yet to be surmounted. With the evolving geopolitical landscape and emergent socio-economic challenges, a new approach will be essential to address these shortcomings and enhance the effectiveness of the EU’s global green reach strategies.

5. A new EU green global reach strategy

The EU should adopt a pragmatic and cohesive plan for the new cycle of the European Green Deal. Recognising that trade-offs may persist, the priorities should be: 1) re-focus from global target-setting to implementation; 2) proactive diplomacy on carbon pricing and international green taxation; 3) streamline the partnership approach into single partnerships for green industrialisation; 4) establish a new international trade and climate deal, and 5) strengthening EU governance mechanisms.

5.1 Re-orienting green diplomacy from targets to implementation

To address the challenges of decarbonisation, security and competitiveness effectively, a paradigm shift is necessary in climate diplomacy, moving away from merely setting targets towards ensuring implementation. This recommendation encompasses several main actions:

Establishment of monitoring secretariats: COP targets need effective implementation. Therefore, dedicated secretariats should be established to monitor and accompany implementation within international institutions, such as the International Energy Agency and the International Renewable Energy Agency (IRENA). These secretariats would be tasked with monitoring progress and fostering coordination, ensuring that commitments made at COPs translate into tangible actions.

The Climate and Clean Air Coalition29, functioning as the secretariat for the Global Methane Pledge, illustrates how this can be done. The EU should advocate for the replication of these monitoring bodies for initiatives such as the Global Renewable Energy and Energy Efficiency Pledge.

Transformation of NDCs into comprehensive national green-transition plans: Nationally Determined Contributions (NDCs) need to evolve into comprehensive national green-transition plans, integrating concrete projects and initiatives. By linking these plans to climate-finance disbursement, particularly in EMDEs, incentives can be created for robust development and implementation.

This linkage will ensure that financial support is aligned with the priorities outlined in national transition plans, facilitating effective climate action. This is very important in view of COP30 in Brazil in November 2025, when countries will have to submit their new updated NDCs.

Promotion of bottom-up initiatives: engaging stakeholders beyond governments is crucial. Private-sector alliances and cities often possess significant innovative potential and can play pivotal roles in accelerating the transition to a low-carbon economy.

By fostering partnerships and initiatives at grassroots level, the EU can tap into diverse expertise, resources and networks, enhancing the effectiveness and inclusivity of its climate diplomacy efforts. Additionally, by promoting bottom-up initiatives, the EU can create a more dynamic and adaptive approach to addressing climate change.

These initiatives are often more agile and responsive to local needs and contexts, allowing for more targeted interventions. Moreover, by empowering stakeholders at grassroots level, the EU can build broader support and ownership for its climate goals, increasing the likelihood of successful implementation and long-term sustainability.

Assessment and strengthening of climate-finance mechanisms: an evaluation of EU climate finance efforts is essential to determine their effectiveness and impact. This assessment should encompass various mechanisms, including Official Development Assistance (ODA), NDICI Global Europe and the European Fund for Sustainable Development Plus (EFSD+) (see the annex).

Main considerations include whether these efforts are yielding tangible results and whether there is a need for increased EU contributions or enhanced coordination among EU countries. For this, it is imperative to carry out impact assessments to evaluate the results achieved and possibly to correct course.

Furthermore, increasing the impact of EU action requires not only bringing in private sector investments but also ensuring they are effectively complemented by EU efforts.

5.2 New carbon pricing and international green-taxation diplomacy

Addressing the intricate balance between decarbonisation, security and competitiveness needs a robust approach to diplomacy related to carbon pricing and international green taxation. The EU has established a taskforce on international carbon pricing and markets diplomacy (European Commission, 2024).

The taskforce’s main objective is to provide EU expertise to support the adoption of carbon-pricing systems in third countries, while also fostering international trade in carbon allowances. This is a positive development that in our view might be structured into three main workstreams:

1. Pivot the works around Article 6 of the Paris Agreement: to contain temperature rises within 1.5 to 2 degrees Celsius, global emissions must be reduced by 43 percent by 2030 and by 60 percent by 2035 (UNFCCC, 2024). Appetite for the use of international carbon markets to move at the required speed is high, with 143 of the 154 UNFCCC parties being willing to use carbon credits under Article 6 of the Paris Agreement, which allows countries to voluntarily cooperate and transfer carbon credits to help each other achieve their emission reduction targets30.

At COP28 in 2023 the EU played a more proactive role than in the past in fostering an agreement on Article 6, while being careful to not undermine the credibility of established mandatory carbon markets, such as the EU ETS.

At the next COPs, starting with COP29 in Baku in November 2024, the EU can contribute to the international efforts to hammer down the outstanding disagreements31 around Article 6, including the need to finalise detailed rules for carbon credit trading to ensure environmental integrity and transparency, and to address concerns about double counting of emissions reductions.

2. Bring to fruition international carbon taxes: the 2021 Organisation for Economic Co-operation and Development agreement on a 15 percent minimum corporate tax and recent developments to end bank secrecy show that ambitious international tax agreements are difficult but achievable.

A COP28 declaration called explicitly “for accelerating the ongoing establishment of new and innovative sources of finance, including taxation”32, while Kenya, Barbados and France have launched an international tax taskforce to explore how to raise finance for sustainable development and climate action through tax policies33.

Potential avenues include levies on aviation, maritime shipping, trade in fossil fuels, financial transactions and extreme personal wealth. Some arguably easier options, such as introducing compulsory minimum excise duties on the fossil fuels used by aviation and maritime shipping, or levying climate taxes on business-class flights, could be viable ways to generate revenue to help poorer countries in their efforts on climate mitigation and adaptation34.

The EU can help advance this process, starting with a push for better carbon accounting and more effective action from the two sectoral bodies, the International Civil Aviation Organisation and the International Maritime Organisation (Sgaravatti, 2023).

3. CBAM diplomacy: the implementation of CBAM is a test of the EU’s ability to deliver and manage the international repercussions of EU climate policy. While the EU should continue with the implementation of CBAM, it should also be adaptable in its approach as CBAM significantly affects partner countries in different ways.

CBAM not only promotes a greener industrial landscape within the EU, but also encourages international partners to adopt low-carbon practices. Countries exporting carbon-intensive goods to the EU are incentivised to implement their own carbon-pricing mechanisms or taxation, to raise revenues at the national level instead of handing them over to the EU.

Since the adoption of CBAM, many countries have started considering establishing domestic emissions trading systems, including Brazil, Chile, India, Indonesia, Malaysia, Vietnam, Thailand and Turkey (Delbeke, 2024).

However, it is equally crucial to intensify CBAM diplomacy in partner countries. Additionally, targeted interventions through direct EU development assistance are essential to mitigate potential adverse impacts on least-developed countries (LDCs).

Finally, there is merit in evaluating the possibility of expanding CBAM to incorporate a new market for carbon removals certificates. This expansion could, for instance, be linked to targeted actions such as the closure of coal-fired power plants, thereby aligning economic incentives with environmental objectives.

5.3 New green industrialisation partnerships

The trend of signing an increasing range of diverse partnerships (ie. on energy, green and critical raw materials) needs consolidation into a single, unified green-industrialisation approach for each partner country.

Promotion of bilateral green-industrialisation partnerships with selected EMDEs: recognising the role that EMDEs play in the global transition to a low-carbon economy, the EU should prioritise the promotion of bilateral green-industrialisation partnerships with significant countries.

These partnerships should facilitate the transition of the selected EMDEs up the supply chain, advancing from mere extraction to refining and value-added processes emphasising sustainability and efficiency.

This transition requires strategic investment in projects aimed at enhancing environmental performance and technological innovation. Collaboration with the private sector is essential to ensure the success of these partnerships.

While direct intervention by EU governments may be limited, they can play important roles by supporting private investment through financial guarantees and export credits, to mitigate country and currency risks.

Alongside national promotional banks, the European Commission and the EIB should strengthen their roles by mobilising resources and providing technical assistance, and can also help on the demand side, by promoting guaranteed offtake agreements.

5.4 New international trade and climate deal

The looming risk of a green trade war between the US, China and the EU poses a significant threat to global decarbonisation efforts. To mitigate this risk and foster a conducive environment for sustainable trade, the EU should advocate for plurilateral agreements on green subsidies and tariffs.

These agreements would ensure that trade policies align with environmental objectives, while preventing the emergence of protectionist measures that undermine global decarbonisation efforts. Collaboration with major partners, particularly the US and China, is essential in this endeavour.

The EU should engage in constructive dialogue with these partners to explore options for cooperation through existing mechanisms such as the WTO, or through plurilateral agreements involving like-minded nations.

5.5 Stronger EU governance

Addressing the EU’s domestic challenges of fragmentation, lack of authority and strategies is imperative for effective global climate and energy action. This recommendation emphasises the need for a more cohesive and authoritative EU governance structure, accompanied by a stronger and more coherent narrative.

The Executive Vice President for the Green Deal should focus on both its internal and external dimension: the current governance structure within the European Commission suffers from significant fragmentation and dispersion of responsibilities. While understandable from an internal functional perspective, this division of labour should not underpin the coherence and effectiveness of the EU green action – both domestically and internationally.

To help steer coordination and coherence a dedicated position of Executive Vice President for the Green Deal should be empowered to oversee both the domestic and international climate and energy agendas. This consolidation of authority would streamline decision-making processes and foster coherent policy implementation.

It could also give the EU a stronger, more authoritative voice in the world when it comes to green-related issues, including COP diplomacy, green industrial partnerships, CBAM diplomacy and energy partnerships.

Develop a strong and coherent narrative: articulating a compelling vision, objectives and strategies for EU climate and energy policies are essential. This narrative should resonate with stakeholders and communicate the EU’s leadership role in addressing climate change and promoting sustainable development.

Emphasising the importance of collaboration, coherence and effectiveness in EU governance to achieve climate and energy goals is vital. By fostering a shared understanding and sense of purpose, the EU can strengthen its position as a global leader in climate action.

Enhance Team Europe Initiatives for effective coordination: to achieve this, the EU should increase buy-in by member states through inclusive decision-making and clear communication about the benefits of coordinated action. Benefits include increased impact, greater cost efficiency and enhanced diplomatic leverage.

Providing financial incentives or matching funds and highlighting the role of the EU countries joining each TEI will also encourage participation. Additionally, coordinated actions in partner countries might follow the Green Frontline Missions35 model adopted by Danish embassies that aims to ensure the presence of a climate ambassador who focuses on promoting the green agenda in countries considered crucial for the global transition.

The presence of a dedicated desk that would coordinate the TEI efforts, prioritising support for European businesses, economic development in partner countries and social equity. This involves engaging local stakeholders, providing comprehensive support, including policy advice and technical assistance, and integrating expertise and political dialogue.

6. Conclusion

The EU faces the difficult challenge of implementing the European Green Deal while dealing with its global repercussions, increased geopolitical tensions and the pressure of ensuring simultaneously both competitiveness and economic security.

In facing these challenges the EU must resist the temptation of protectionist inward-looking policies. In fact, the external dimension of the Green Deal is as important as the domestic one and should be brought to the forefront of EU’s climate strategy.

Failure to support decarbonisation abroad risks compromising not only the Green Deal but global climate targets. The 2024-2029 institutional cycle provides an opportunity for the EU to solidify its leadership and drive transformative change in global green diplomacy and partnerships.

Our policy recommendations chart a pragmatic path to enhance the EU’s green global reach, to ensure that Europe remains at the forefront of global efforts to combat climate change, while maintaining its global influence in doing so.

Annex: The current EU external green action toolkit

Notes: * The European Fund for Sustainable Development Plus (EFSD+) is one of the financing instruments of the Neighbourhood, Development and International Cooperation Instrument-Global Europe (NDICI-GE); it provides technical assistance, guarantees and blended finance to improve mobilisation of financial resources from the private sector towards economic development projects in partner countries. ** CBAM is currently in its transitional phase until 2025, and it will apply in its definitive regime from 2026. *** The regulation came into effect on 29 June 2023. Companies have until 30 December 2024 to comply, except for micro- and small enterprises which have until 30 June 2025.

Source: Bruegel.

Endnotes

1. See UNFCC press release of 14 March 2024, ‘Building Support for More Ambitious National Climate Action Plans’.

2. The sectors covered by the initial application of CBAM are aluminium, cement, electricity, fertilisers, hydrogen, iron and steel.

3. This refers to high-demand scenario (HDS) estimates that assume rapid technology deployment and a combination of market shares and material intensities that results in a sharp increase in materials demand.

4. Finalised in May 2024. See Council of the EU press release of 27 May 2024, ‘Industrial policy: Council gives final approval to the net-zero industry act’.

5. Finalised in March 2024. See Council of the EU press release of 18 March 2024, ‘Strategic autonomy: Council gives its final approval on the critical raw materials act’.

6. Patricia Nilsson, ‘BASF outlines further cost-cutting and 2,600 job losses as it downsizes in Germany’, Financial Times, 24 February 2023.

7. A significant challenge in the hydrogen supply chain is its transportation. Because hydrogen has a low energy density it often needs to be compressed or liquefied, both of which require additional energy and infrastructure.

8. Such as the possible £16 billion Xlinks power cable between the UK and Morocco.

9. Cecilia Trasi, Giovanni Sgaravatti and Simone Tagliapietra, ‘Europe’s time to lead on climate action’, Euractiv, 20 December 2023.

10. See the Global Renewables and Energy Efficiency Pledge.

11. See the US Energy Information Administration website.

12. European Commission news of 18 October 2022, ‘The EU and Morocco launch the first Green Partnership on energy, climate and the environment ahead of COP 27’.

13. European Council press release of 22 May 2023, ‘EU and Republic of Korea launch a Green Partnership’.

14. European Commission press release of 13 June 2023, ‘Global Gateway: EU and Argentina step up cooperation on raw materials’.

15. European Commission press release of 28 May 2024, ‘EU and Australia sign partnership on sustainable critical and strategic minerals’.

16. European Commission press release of 21 June 2021, ‘EU and Canada set up a strategic partnership on raw materials’.

17. European Commission press release of 18 July 2023, ‘Global Gateway: EU and Chile strengthen cooperation on sustainable critical raw materials supply chains’.

18. European Commission press release of 8 November 2022, ‘COP27: European Union concludes a strategic partnership with Namibia on sustainable raw materials and renewable hydrogen’.

19. European Commission press release of 21 March 2024, ‘EU and Norway sign strategic partnership on sustainable land-based raw materials and battery value chains’.

20. European Commission press release of 8 November 2022, ‘Strategic Partnership between the European Union and Kazakhstan on sustainable raw materials, batteries and renewable hydrogen value chains’.

21. European Commission press release of 13 July 2021, ‘EU and Ukraine kick-start strategic partnership on raw materials’.

22. European Commission press release of 26 October 2023, ‘Global Gateway: EU signs strategic partnerships on critical raw materials value chains with DRC and Zambia and advances cooperation with US and other key partners to develop the Lobito Corridor’.

23. Council of the EU press release of 23 November 2023, ‘Climate finance: Council approves 2022 international climate finance figures’.

24. See European Commission, ‘What is Team Europe’.

25. See European Commission, ‘Global Gateway’.

26. Alan Beattie, ‘The colonialist overtones of EU’s green trade crusade’, Financial Times, 25 April 2024.

27. See for example a joint letter (undated) of maritime industry associations on earmarking of ETS revenues.

28. See World Trade Organisation, ‘Joint Letter – European Union proposal for a regulation on deforestation-free products – Submission by Indonesia and Brazil’, 29 November 2022.

29. See https://www.ccacoalition.org/.

30. See UN Environment Programme, ‘Carbon Markets’, undated.

31. Carbon Brief, ‘COP28: Key outcomes agreed at the UN climate talks in Dubai’, 13 December 2023.

32. See ‘UAE leaders’ declaration on a global climate finance framework’.

33. Laurence Tubiana, ‘Taxing Polluters Is the Key to Climate Justice’, Project Syndicate, 9 April 2024.

34. This is equivalent to phasing out fossil-fuel subsidies that counteract the effectiveness of taxes in changing price incentives.

35. See Denmark Climate Diplomacy, undated.

References

Bolton, P, AM Kleinnijenhuis and J Zettelmeyer (2024) ‘The economic case for climate finance at scale’, Policy Brief 09/2024, Bruegel.

Cannas, G, S Ferraro and K van de Casteele (2023) ‘The use of crisis State aid measures in response to the Russian invasion of Ukraine’, Competition State Aid Brief 1/2023, European Commission.

Carrara, S, S Bobba, D Blagoeva, P Alves Dias, A Cavalli, K Georgitzikis … M Christou (2023) Supply Chain Analysis and Material Demand Forecast in Strategic Technologies and Sectors in the EU: A Foresight Study, JRC Science for Policy Report, Joint Research Centre, European Commission.

Council of the EU (2024) ‘Council Conclusions on Green Diplomacy’, 7865/24, 18 March.

Dekeyser, K and S Woolfrey (2021) ‘A Greener Europe at the Expense of Africa? Why the Eu Must Address the External Implications of the Farm to Fork Strategy’, Briefing Note 137, European Centre for Development Policy Management (ECDPM).

Delbeke, J (2024) ‘How the EU Can Support Carbon Pricing at Global Level’, STG Policy Papers, Florence School of Transnational Governance.

EEA (2023) ‘Climate Finance to Developing Countries’, dataset, European Environment Agency.

Energy Institute (2023) Statistical Review of World Energy 2023.

European Commission (2021) ‘The Global Gateway’, JOIN(2021) 30 final.

European Commission (2023) ‘European Economic Security Strategy’, JOIN(2023) 20 final.

European Commission (2024) ‘Europe’s 2040 climate target and path to climate neutrality by 2050 building a sustainable, just and prosperous society’, COM(2024) 63 final.

Forster, PM, C Smith, T Walsh, W Lamb, R Lamboll, B Hall … P Zhai (2024) ‘Indicators of Global Climate Change 2023: annual update of key indicators of the state of the climate system and human influence’, Earth System Science Data Discussions 6(16): 2625–2658.

IEA (2023) World Energy Outlook 2023 – Analysis, International Energy Agency.

Keijzer, N, I Olivié, M Santillán O’Shea, S Koch and G Leiva (2023) ‘Working Better Together? A Comparative Assessment of Five Team Europe Initiatives’, Elcano Policy Paper, November, Real Instituto Elcano.

Kleimann, D, N Poitiers, A Sapir, S Tagliapietra, N Véron, R Veugelers and J Zettelmeyer (2023) ‘How Europe should answer the US Inflation Reduction Act’, Policy Contribution 04/2023, Bruegel.

Le Mouel, M and N Poitiers (2023) ‘Why Europe’s critical raw materials strategy has to be international’, Analysis, 5 April, Bruegel.

Leonard, M, J Pisani-Ferry, J Shapiro, S Tagliapietra and G Wolff (2021) ‘The geopolitics of the European Green Deal’, Policy Contribution 04/2021, Bruegel.

Losz, A and A-S Corbeau (2024) ‘Anatomy of the European Industrial Gas Demand Drop’, Commentary, 18 March, Center on Global Energy Policy at Columbia University.

Magacho, G, A Godin and E Espagne (2022) ‘Impacts of CBAM on EU trade partners: Consequences for developing countries’, Working Paper, Agence française de développement.

Moritz, M, M Schönfisch and S Schulte (2023) ‘Estimating global production and supply costs for green hydrogen and hydrogen-based green energy commodities’, International Journal of Hydrogen Energy, 48(25): 9139–54.

Overland, I and R Sabyrbekov (2022) ‘Know your opponent: Which countries might fight the European carbon border adjustment mechanism?’ Energy Policy 169: 113175.

Oberthür, S and C Dupont (2021) ‘The European Union’s international climate leadership: towards a grand climate strategy?’ Journal of European Public Policy 28(7): 1095-1114.

Sgaravatti, G (2023) ‘The struggle to cut emissions from international aviation and shipping’, Analysis, 25 September, Bruegel.

Sgaravatti, G, S Tagliapietra and G Zachmann (2023) ‘Adjusting to the energy shock: the right policies for European industry’, Policy Brief 11/2023, Bruegel.

Tagliapietra, S, R Veugelers and J Zettelmeyer (2023) ‘Rebooting the European Union’s Net Zero Industry Act’, Policy Brief 15/2023, Bruegel.

UNFCCC (2024) ‘Simon Stiell: Remarks at the 2024 Petersberg Dialogue’, 25 April.

Verpoort, PC, L Gast, A Hofmann and F Ueckerdt (2024) ‘Impact of global heterogeneity of renewable energy supply on heavy industrial production and green value chains’, Nature Energy 9(4): 491–503.

The authors are grateful to Heather Grabbe, Marc Vanheukelen and Georg Zachmann for the extensive comments on earlier drafts. They are also grateful to the participants in an March 2024 workshop held at Bruegel to discuss this issue. Financial support from the European Climate Foundation is gratefully acknowledged. This article is based on Bruegel Policy Brief Issue n˚11/24 | June 2024.