How the GMT changes the taxation of MNEs

Felix Hugger and Ana Cinta González Cabral are Economists, Massimo Bucci is a Tax Economist, Pierce O’Reilly is a Senior Tax Economist, all at the OECD, and Maria Gesualdo is with the European Commission – Joint Research Centre

The Global Minimum Tax (GMT) represents a major advance in international cooperation regarding the taxation of multinational enterprises. It aims to ensure that large multinational enterprises (MNEs) with revenues above €750 million are subject to a 15% minimum effective tax rate in every jurisdiction where they operate and to place a floor on corporate tax competition (OECD 2021a).

At present, a steadily increasing number of jurisdictions are implementing the GMT domestically. Based on the jurisdictions that have already implemented or are taking steps to do so, 90% of large MNEs globally will be in-scope of the GMT by the end of 2025.

This is due to the design of the GMT which ensures that it is effective, even if not all jurisdictions implement the rules. If a jurisdiction does not assert its taxing rights over low-taxed profit, ie. profit taxed at an effective rate below 15%, others will have the right to collect the top-up tax (details on the design of the rules are summarised in OECD 2021b).

In this column, we provide an overview of the expected implications of the GMT for the international taxation of MNEs. The column builds on earlier OECD work that analysed the impact of the two-pillar solution (OECD 2020) and recent work that estimated the size and global distribution of low-taxed profit (Hugger et al 2023, 2024b).

The analysis is largely based on aggregated Country-by-Country Reporting data, complemented with information from additional sources, for the years 2017-2020. The analysis uses these data to assess the impact of the GMT on tax rate differentials, profit shifting, low-taxed profit, and tax revenues. Details on the methodology are outlined in Hugger et al (2024a).

The GMT cuts tax rate differentials between jurisdictions

As the implementation of the GMT is progressing, the effective taxation of MNE profit will increase in many jurisdictions. The effect is expected to be largest in jurisdictions which historically taxed MNE profits at comparably low or even zero rates. As a result, the differences in effective tax rates between jurisdictions fall.

Overall, the GMT is estimated to reduce tax rate differentials by around 30%. The reduction in tax rate differentials between investment hubs (jurisdictions with FDI to GDP ratios above 150%) and non-hub jurisdictions is even larger with the average differential falling by almost half, from 14.2 percentage points to 7.5 percentage points.

Narrower differences in the effective taxation of MNEs across jurisdictions may elevate the importance of non-tax factors for investment decisions and could provide room to reconsider the role of the tax system in the investment policy mix. This could in turn lead to a more efficient allocation of capital globally.

While the implementation of the GMT is already underway, some uncertainty remains with respect to the full extent of implementation by jurisdictions

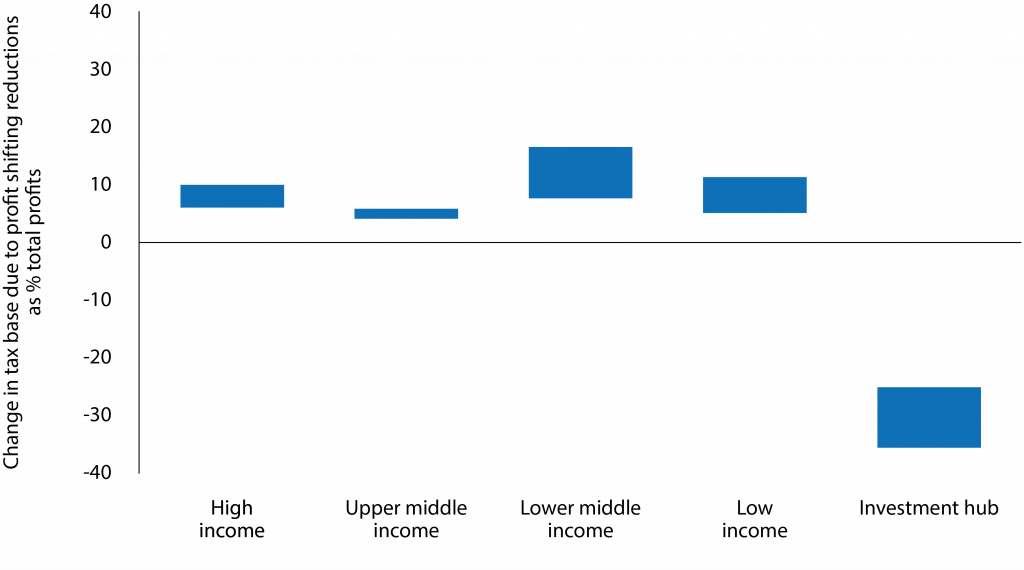

The GMT lowers incentives to shift profits to investment hubs

Profits have been shown to be sensitive to tax rate differentials between jurisdictions (eg. Bratta et al 2021, Ongena et al 2021, Wier et al 2018; or Beer et al 2020 for a summary of the academic literature). As tax rate differentials between jurisdictions fall by way of GMT implementation, the gains from shifting profits to investment hubs are reduced.

Accordingly, total shifted profit is expected to decline. Across a range of different scenarios, shifted profits are estimated to fall by around 50%. This results in tax base gains in non-hub jurisdictions across all income groups, and a reduction of the tax base in investment hubs by around 30% (see Figure 1).

While these effects may take time to materialise, reduced profit shifting implies that more profit will be located where MNEs have substantial economic activities. Developing countries, may particularly benefit since academic research has suggested that these countries are more exposed to profit shifting (Johannesen et al 2020, Cobham and Janský 2018).

However, the GMT is an unprecedented, coordinated reform to the taxation of MNEs. Extrapolations based on existing estimates of the responsiveness of profit shifting to tax rate differentials should be treated with caution.

Figure 1. Change in tax base due to profit shifting reduction, by jurisdiction group

Note: Average changes in total profit by income group following the implementation of the GMT. Bounds are constructed using six scenarios with different assumptions regarding profit shifting reductions. Data includes non-Inclusive Framework member jurisdictions. Profit from investment funds in UPE jurisdictions are assumed to be unaffected by the decline in profit shifting incentives since investment funds as UPEs are excluded from the GMT. Other exclusions apply but are not modelled. Total profit is profit before accounting for profit shifting.

Source: Hugger et al (2024).

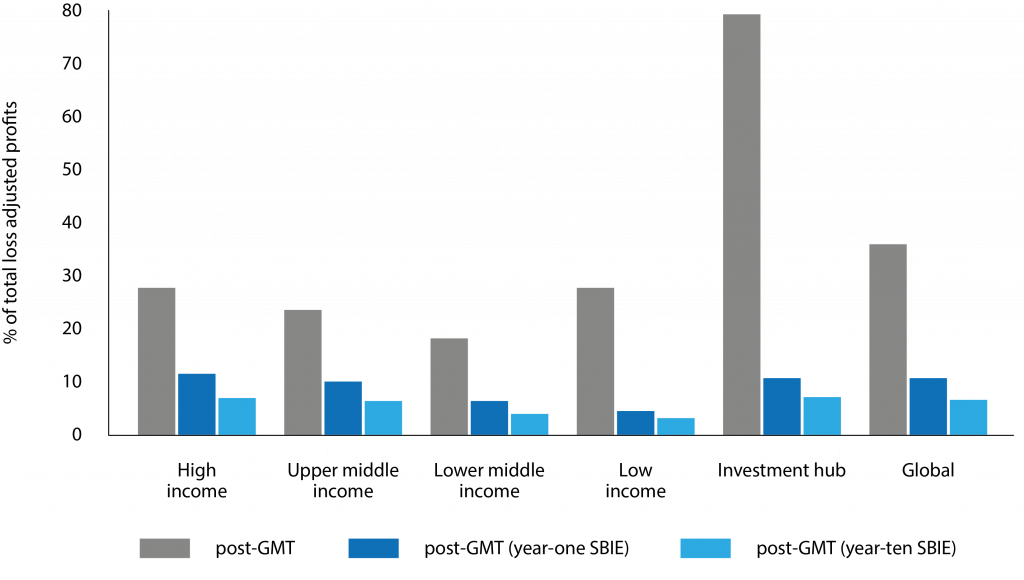

The GMT reduces global low-taxed profit

Before the introduction of the Global Minimum Tax, more than a third of the total global profit of large MNEs was taxed at effective tax rates below 15% (Hugger et al 2024b). The GMT is estimated to reduce existing global low-taxed profit by more than 80% in the longer run (see Figure 2). The reduction in low-taxed profit comes from the application of top-up taxes and the reduction in profit shifting activity.

This reduction in low-taxed profit is estimated to take place in all income groups, but is expected to be most pronounced in investment hubs, which have highest incidence of low-taxed profit prior to the reform.

Remaining low-taxed profit is largely due to a feature of the Global Minimum Tax that carves out a fixed return on economic substance: the Substance-Based Income Exclusion (SBIE). The SBIE excludes a ‘routine’ return on assets and payroll from the base of the GMT, but the size of the SBIE declines over the first 10 years.

As the share of MNE profit subject to the minimum tax increases, less profit remains low-taxed. The blue bars indicate the low-taxed profit remaining under the SBIE just after the introduction of the SBIE (‘year-one SBIE’), and after the reduction of the SBIE to its final level after ten years (‘year-ten SBIE’).

Figure 2. Share of low-taxed profit as a percentage of total profit, by jurisdiction group

Note: The chart reflects the share of total profit that is low taxed by income group. ‘Global’ refers to all jurisdictions. Low-taxed profit is defined as profit taxed at loss-adjusted effective tax rates lower than 15%. The ‘Pre-GMT’ scenario reflects the current distribution of profit absent any GMT effects. The ‘Post-GMT’ scenarios capture the distribution of profit under reduced profit shifting and after the application of the GMT is accounted for. Two scenarios of the substance-based income exclusion (SBIE) are considered. Global low-taxed profit falls from 36% to 11% in the year-one SBIE scenario and to 7% in a year-ten SBIE scenario.

Source: Hugger et al (2024).

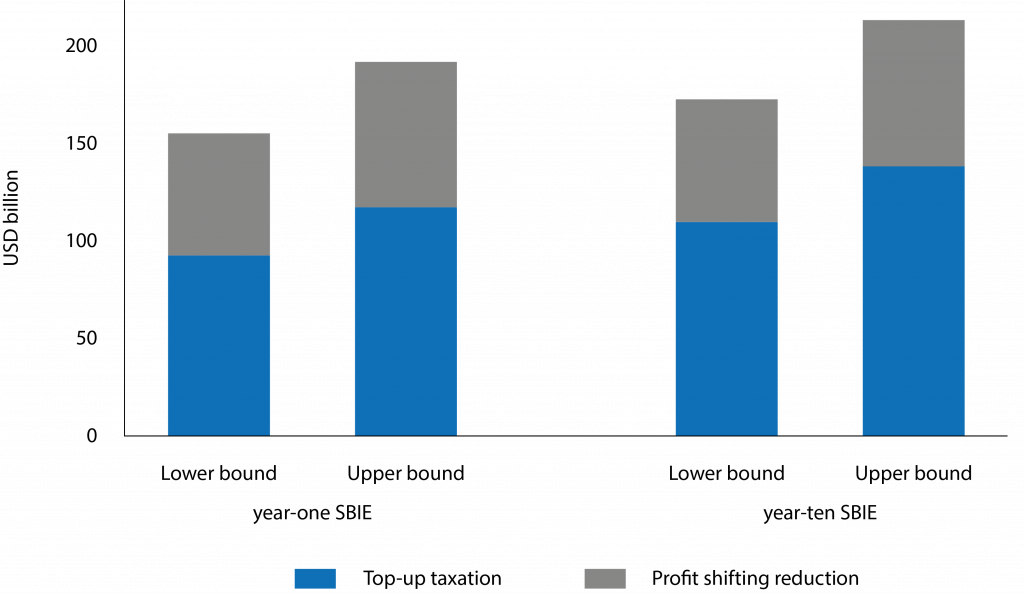

The GMT increases corporate tax revenue

Global corporate income tax revenues are expected to increase in the aftermath of the GMT due to the application of top-up taxes and reduced profit shifting. The GMT is estimated to raise additional global corporate income tax revenues of $155-192 billion annually under the year-one SBIE, which is equivalent to between 6.5% and 8.1% of global corporate income tax revenues in the sample period of 2017-2020 (see Figure 3).

Around two thirds of these estimated revenue gains are attributed to top-up taxation, the remaining one third is estimated to come from a reduction in profit shifting. The reduction of the SBIE over time, is expected to generate a modest increase in these tax revenue gains.

Revenue gains are expected to accrue to jurisdictions from all income groups, with the exact distribution of revenue gains among jurisdictions depending on the assumptions on governments’ implementation and MNE’s behavioural reactions.

Figure 3. Global revenue gains by implementation scenario

Note: The estimates are presented as an average of the 2017-2020 results. Estimates are presented for Inclusive Framework (IF) member jurisdictions only. Estimates include both direct and indirect revenue gains and account for variation in the sensitivity of profit shifting. Estimates in the scenario presented assume that 70-100% of all IF member jurisdictions implement the GMT, except for zero-tax jurisdictions who (i) do not have any corporate income tax infrastructure and (ii) have not taken any public steps to implement as of 27 October 2023. Non-IF member jurisdictions are assumed to not implement. Estimates are presented for the SBIE year-one scenario (10% on payroll and 8% on tangible assets). Estimates are presented net of any lost revenue from CFC regimes modelled.

Source: Hugger et al (2024).

Conclusion

Our analysis contributes to a growing literature that assesses the impact of the GMT. At the same time, it is subject to a variety of caveats and based on various assumptions. While it uses a comprehensive data infrastructure, mapping global MNE profit and activity at the jurisdictional level, the aggregated nature of the data implies that certain MNE-specific adjustments relevant for the GMT calculations cannot be made.

In addition, while the implementation of the GMT is already underway, some uncertainty remains with respect to the full extent of implementation by jurisdictions. Similarly, given the unprecedented nature of this reform, the behavioural reactions of MNEs to reduced profit shifting incentives are highly uncertain.

The results presented reflect such uncertainty under a range of scenarios involving different MNE and government responses. Further work could continue to examine MNE and jurisdictions’ behavioural reactions, the GloBE tax base, and the drivers of low-taxed profit.

References

Beer, S, R de Mooij and L Liu (2020), “International Corporate Tax Avoidance: A Review of the Channels, Magnitudes, and Blind Spots”, Journal of Economic Surveys 34(3): 660-688.

Bratta, B, V Santomartino and P Acciari (2021), “New patterns of profit shifting emerge from country-by-country data”, VoxEU.org, 28 June.

Cobham, A and P Janský (2018), “Global distribution of revenue loss from corporate tax avoidance: re-estimation and country results”, Journal of International Development 30(2): 206-232.

Hugger, F, A González Cabral and P O’Reilly (2023), “Effective tax rates of MNEs: New evidence on global low-taxed profit”, OECD Taxation Working Papers, No. 67.

Hugger, F, A González Cabral, M Bucci, M Gesualdo and P O’Reilly (2024a), “The Global Minimum Tax and the taxation of MNE profit”, OECD Taxation Working Papers, No. 68.

Hugger, F, A González Cabral and P O’Reilly (2024b), “Low-taxed profit of multinational companies does not only exist in low-tax jurisdictions”, VoxEU.org, 21 June.

Johannesen, N, T Tørsløv and L Wier (2020), “Are Less Developed Countries More Exposed to Multinational Tax Avoidance? Method and Evidence from Micro-Data”, The World Bank Economic Review 34(3): 790-809.

OECD (2020), “Tax Challenges Arising from Digitalisation – Economic Impact Assessment: Inclusive Framework on BEPS”, OECD/G20 Base Erosion and Profit Shifting Project.

OECD (2021a), Statement on a Two-Pillar Solution to Address the Tax Challenges Arising from the Digitalisation of the Economy, OECD, Paris.

OECD (2021b), Tax Challenges Arising from Digitalisation of the Economy – Global Anti-Base Erosion Model Rules (Pillar Two): Inclusive Framework on BEPS, OECD/G20 Base Erosion and Profit Shifting Project, OECD, Paris.

Ongena, S, M Delis, L Laaeven and F Delis (2021), “Global evidence on profit shifting: The role of intangible assets”, VoxEU.org, 11 October.

Wier, L, G Zucman and T Tørsløv (2018), “The missing profits of nations”, VoxEU.org, 23 July.

This article was originally published on VoxEU.org.