Smarter EU industrial policy for solar panels

Ben McWilliams is an Affiliate Fellow, Simone Tagliapietra is a Senior Fellow at Bruegel, and Cecilia Trasi is a Research Analyst, all at Bruegel

Executive summary

The European Union plans a major increase in solar PV capacity from 263 GW today to almost 600 GW by 2030. If nothing changes, this expansion will be based almost exclusively on solar panels imported from China, which supplies over 95 percent of solar panels used in the EU. This dependence has raised concerns about EU economic security and geopolitical vulnerabilities, especially in light of recent global disruption.

The EU has agreed in principle a non-binding 40 percent self-sufficiency benchmark for solar panels and other identified strategic technologies, to be approached or achieved by 2030. However, for the solar sector specifically, there is no strong economic justification for an import-substitution approach. Such a strategy risks increasing the costs of solar panels, slowing deployment and creating industries that are over-reliant on subsidies.

EU solar manufacturing subsidies are not appropriate based on criteria of European production alone. Subsidies could, however, be justified on innovation grounds, by supporting new solar products that have a real chance to develop into sustainable industries that contribute to climate goals.

To address concerns about short-term dependence, alternative tools should be employed: accelerated solar deployment, strategic stockpiling and gradually diversifying import sources. In the longer term, recycling of solar panels deserves greater attention and funding.

In terms of strengthening economic resilience relative to China, Europe should implement an industrial policy that intervenes in sectors that are more likely to contribute to sustainable economic growth and alleviate decarbonisation bottlenecks.

1 The ‘kingpin’ of Europe’s energy transition

Solar power promises to be a major engine of Europe’s energy transition. By 2030, European Union countries aim to reach the target of almost 600 gigawatts1 of installed solar photovoltaic (PV) capacity as set out in the European Union’s Solar Energy Strategy (European Commission, 2022a) – up from around 263 GW today2.

If this target is met, solar PV will become the largest source of electricity production in the EU by capacity. Not only that, but the rate of solar deployment will be faster than any other; plans for increasing wind capacity, for example, aim at reaching around 500 GW by 2030, up from 200 GW today (European Commission, 2023a).

This European solar revolution is, and will continue to be, predominantly ‘made in China’. In 2022, over 95 percent of Europe’s solar panels came from China3, which has established itself as the global hub for solar PV manufacturing (IEA, 2023).

Chinese solar panels are becoming cheaper and also more innovative (ETIP PV, 2023). This is good news for the EU as it enables the acceleration of the deployment of solar energy in a cost-effective manner. However, such a high import dependency on a single supplier could expose the EU to the economic risks related to high market concentration and, potentially, to the risks related to an eventual geopolitical use of this dominant position.

Pandemic-related supply chains disruptions, the energy crisis, the increasing assertiveness of Chinese export controls on critical raw materials and competitiveness pressures arising from the United States’s Inflation Reduction Act, have worried and continue to worry European policymakers.

This has led to a fresh debate on how to define and pursue economic security and, more tangibly, to a revival of new industrial policy initiatives aimed at fostering EU competitiveness and geopolitical resilience in clean technologies and critical raw materials (European Commission, 2023b).

In February 2024, the EU institutions agreed in principle on the Net-Zero Industry Act (NZIA), with the aim of supporting domestic manufacturing of clean technologies, such as solar PV, as strategic projects. Part of the NZIA is a plan to ensure that EU manufacturing of strategic net zero technologies ‘approaches or reaches’ a benchmark value of 40 percent of the EU’s deployment needed by4.

This approach risks relying heavily on import substitution. This is controversial because it disregards the costs of promoting self-sufficiency compared to the use of cheaper imports and, more broadly, because it signals a turn towards protectionism (Tagliapietra et al 2023a).

Furthermore, adopting a flat benchmark value for different technologies in which Europe has a very different starting positions and very different growth potentials is not economically rational. In this context, this Policy Brief evaluates specifically the case of solar PV manufacturing.

We start by describing the characteristics of solar PV supply chains, and then outline the diverging historic and current trajectories of Europe and China in solar PV manufacturing. We evaluate the economic case for European intervention to stimulate domestic manufacturing, finding that there are no clear decarbonisation or economic growth benefits from doing so – leaving mitigating the risk of over-dependence on Chinese imports as the only justification. Even this risk should not be exaggerated. Innovation and not domestic content should be the defining criteria for manufacturing subsidies.

2 Solar PV manufacturing and the EU’s situation

2.1 Understanding solar PV supply chains

Any industrial policy strategy in the solar sector should be rooted in an understanding of the complexities of solar PV supply chains. The solar industry encompasses so many manufacturing processes that the concept of ‘public support for solar PV manufacturing’ is an oversimplification.

The production of a solar panel begins with quartz (SiO2), commonly found in sand. This is transformed into polysilicon by an energy-intensive process of melting and purification. Polysilicon is used for the production of solar panels, semiconductors and electronic devices. China accounts for around 80 percent of global polysilicon production capacity (IEA, 2022).

Around 35 percent of global polysilicon production capacity is located in Xinjiang, a Chinese region under international scrutiny for violation of human rights and forced labour involving Uyghurs and other Muslim-majority groups (Box 1).

Europe has 11 percent of global polysilicon production capacity (Bettoli et al 2022), amounting to 26 GW in 2023 (SolarPower Europe, 2023). However, this capacity is largely used to deliver higher quality polysilicon for semiconductor production, not for solar panels (Basore and Feldman, 2022).

Within the solar industry, polysilicon is melted to form ingots, which are then sliced into thin wafers. This is a capital- and energy-intensive process, which benefits heavily from economies of scale. Almost all current ingot and wafer manufacturing is in China, with half of global capacity coming from just eight Chinese plants (Basore and Feldman, 2022).

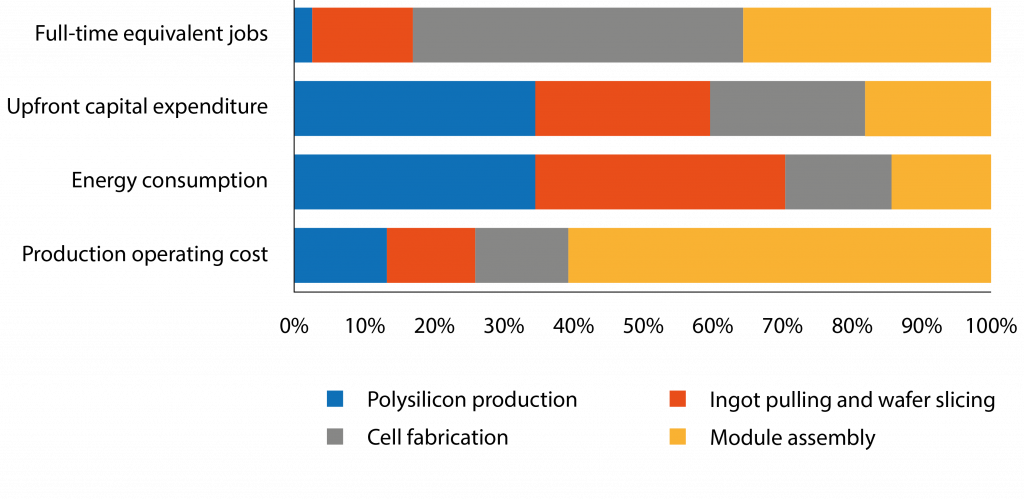

Wafers are then processed to produce cells in a highly automated system. Finally, cells are assembled into modules and sandwiched with other components including glass and aluminium frames. Along this value chain, the earlier stages are capital- and energy-intensive, while later stages account for the greater share of jobs and production cost (Figure 1).

Figure 1. Distribution of economic indicators across the solar manufacturing chain

Source: Bruegel based on Woodhouse et al (2021), ESIA, BNEF.

Box 1. Forced labour in the solar supply chain

Allegations of forced labour have been made about polysilicon factories in Xinjiang, China. State-sponsored work programmes have been criticised for their coercive nature, often under the guise of poverty alleviation and anti-terrorism strategies. Evidence reported by the United Nations indicates that many Uyghur workers are subjected to conditions tantamount to forced labour and enslavement, unable to refuse work without the threat of re-education and internment (OHCHR, 2022). Further research highlighted that several major solar companies are implicated in the use of forced labour. Firms including Daqo, TBEA, Xinjiang GCL and East Hope, which account for more than a third of global solar-grade polysilicon supply, are implicated.

The issue extends beyond China, with evidence of forced labour also found in Malaysian factories5, but the Chinese industry’s dependence on supply from Xinjiang, combined with opaque reporting practices, complicates the avoidance of products produced using forced labour (Crawford and Murphy, 2023). This has led to a call for greater transparency and accountability within the industry.

The international response to these findings has varied. Following the anti-dumping and countervailing duty tariffs in place since 2012, 2015 and 2018, the United States blocked the import of solar panels and components from China with the Uyghur Forced Labor Prevention Act, in force since 2022 (The White House, 2021). The United Kingdom, under its Modern Slavery Act, requires companies with turnover above £36 million to report their efforts to prevent modern slavery in their supply chains.

In 2022, the European Commission (2022b) proposed an EU market ban on products made with forced labour. The regulations require companies to conduct due diligence to ensure that solar panels are produced ethically and sustainably.

Operating at the end of the value chain, module assemblers outside China typically import solar cells – the core component of the module. Module-assembly factories do not require high investment or substantial set-up time (ETIP PV, 2023). Production lines can be deployed in just one or two years.

This means factories can be paused and then restarted quickly and easily. Many of the new factories planned in the EU will focus on module assembly because it is flexible and can adapt quickly to changes in the market or in policy. The EU has 10 GW capacity for assembling modules but this currently operates at only about 10 percent capacity6.

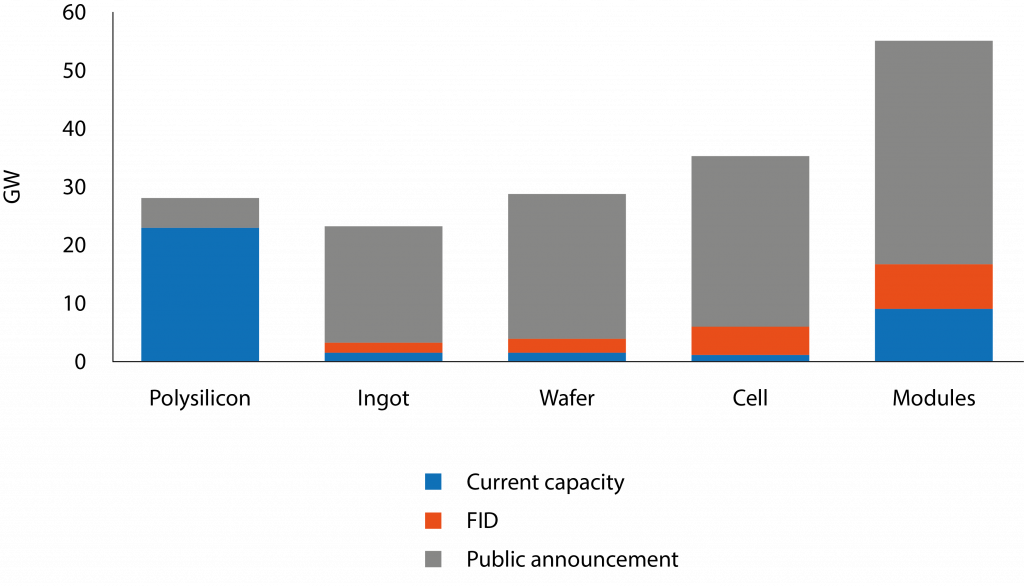

The estimated capacities of European manufacturers at each stage of the value chain are shown in Figure 2. This contrasts with estimated deployment in 2023 of 60 GW.

Figure 2. Solar manufacturing expansion in Europe up to 2026

Note: capacities are estimated as of 2023. FID = final investment decision.

Source: Bruegel European Clean Tech Tracker (forthcoming).

If the EU wishes to use import substitution to reduce dependency on China, it must have a granular industrial policy that supports the development of all stages of the solar manufacturing value chain7. While a sole focus on module assembly will have the biggest jobs and economic impact, it will not improve import resilience as producers would remain reliant on imported cells.

It will be difficult for the EU to develop substantial capacities in earlier value-chain stages, which are capital- and energy-intensive, especially as energy prices have remained somewhat elevated since the 2022 energy crisis (McWilliams et al 2024).

2.2 Solar PV manufacturing: the diverging trajectories of Europe and China

To understand the EU’s lack of developed solar PV manufacturing, one needs to appreciate China’s success.

China’s solar PV industry emerged in the mid-1990s to address domestic needs, but rapidly became global. Chinese regions with favourable solar potential but limited access to other cheap and clean electricity sources started to look with interest at deployment of solar energy as a way to accelerate electrification (Zhang et al 2021). By 2003, China’s solar energy installed capacity had soared to 45 MW, from 7 MW in 1995.

On the manufacturing side, foreign investment bolstered the sector’s expansion. Chinese firms such as Suntech significantly boosted the sector’s growth by raising funds through overseas IPOs. Notably, around 80 percent of China’s solar panels were exported to the European market during this period (Cao and Groba, 2013), driven by the generous feed-in-tariffs provided by EU governments to accelerate the deployment of solar energy (Grau et al 2012).

China’s export-oriented strategy resulted in significant advancements in production capacity and quality, along with substantial cost reductions. These developments played a key role in advancing the global rise of solar power. By 2008, the industry had experienced a tenfold increase in manufacturing capacity, establishing China as the global frontrunner in solar PV manufacturing (Zhang et al 2021).

The 2008 financial crisis led to a downturn in international demand for solar panels, compelling the Chinese government to pivot towards the domestic market. Massive solar energy deployment subsidies were rolled out, resulting in the production of solar PV cells increasing eight-fold between 2009 and 2011, while production of wafers grew tenfold and of polysilicon eighteen-fold (Zhang et al 2021).

These measures reduced manufacturing capacity costs and saw Chinese capacity grow at twice the global rate, solidifying its dominance in global solar PV manufacturing (Grau et al 2012). This rapid expansion resulted in significant oversupply worldwide, which together with a 70 percent drop in polysilicon prices8, led to drastically increased competition in the global solar PV market (Carvalho et al 2017).

This surge in cheap Chinese solar panels became an existential threat to European manufacturers, leading to a significant decline in some segments of Europe’s PV industry. Many European solar panel manufacturers struggled to compete with the low-priced imports, resulting in closures and a reduction in market share.

In 2011, Solarworld (a major German manufacturer) and Prosun (at the time, the representative ogranisation of European solar-panel manufacturers), petitioned the European Commission for anti-dumping and anti-subsidy investigations into Chinese solar panels.

In 2012, the European Commission initiated a major investigation and determined that the appropriate value of a Chinese solar panel sold in Europe ought to be 88 percent higher than its then selling price9.

The Commission proposed the ‘price undertaking’ agreement10, under which Chinese companies were permitted to export solar products to the EU duty free up to an annual limit of 7 GW, provided the price stayed at or above €0.56 per watt.

Exports exceeding this quota or priced below the minimum threshold were subject to anti-dumping duties, intended to increase the selling price of Chinese panels in Europe by an average of 47 percent starting in August 2013.

China responded with anti-dumping and anti-subsidy investigations into EU wine imports but the EU measures were nevertheless renewed in 2015 and 2017, with the duties reduced to 30 percent and the minimum import price adjusted to align with global market rates.

Ultimately, in August 2018, the Commission removed the anti-dumping tariffs, considering it beneficial for the EU after evaluating the needs of producers against those of users and importers of solar panels11. This decision was influenced by the EU’s goal of increasing the deployment of solar energy and by the reduction in the costs of solar components, which allowed import prices to align with world market prices.

Furthermore, the European industry did not gain any advantage from the reduced market presence of Chinese imports that resulted from the imposed measures. Instead, the EU’s solar market share declined further, primarily because of increases in imports from countries in South Asia12.

And yet, every cloud has a silver lining. The competitive pressures, while forcing some Western firms out of the market, also spurred innovation among the remaining European companies, particularly those with a significant pre-existing base in innovation (Carvalho et al 2017; Bloom et al 2021).

Most importantly, the overall decrease in solar equipment costs, largely attributed to Chinese manufacturing, significantly lowered the levelised cost of energy13 for solar PV, making it a formidable competitor to coal and gas in electricity generation (Carvalho et al 2017). In this context, the expansion of Chinese manufacturing had a positive impact on the solar sector at the global level (Andres, 2022; IEA, 2023a).

The European solar revolution is, and will continue to be, predominantly ‘made in China’

2.3 Europe’s solar-panel dilemma: cost-efficiency vs geopolitical resilience

More than 90 percent of solar panels deployed in the EU are still imported from China, primarily because of their low price. In 2022, Chinese solar panels were estimated to be the cheapest in the world at $0.26/watt (Woodhouse et al 2021).

Solar panels produced in Germany were approximately 40 percent more expensive, at $0.38/watt. This disparity was largely driven by higher input costs, both in terms of energy (additional $0.05/watt) and labour (additional $0.04/watt).

Since then, a drop in polysilicon prices has further depressed the price of solar PV modules. In 2023, the price of Chinese solar panels dropped by over 40 percent, likely widening the price gap with the remaining European production. Bettoli et al (2022), prior to the surge in energy prices in Europe, estimated a $0.09/watt gap between European manufacturers and ‘leading industry cost levels’.

The difference was mainly driven by higher input costs in Europe (energy, labour and capital costs) and by lack of access to the critical raw materials needed for these technologies.

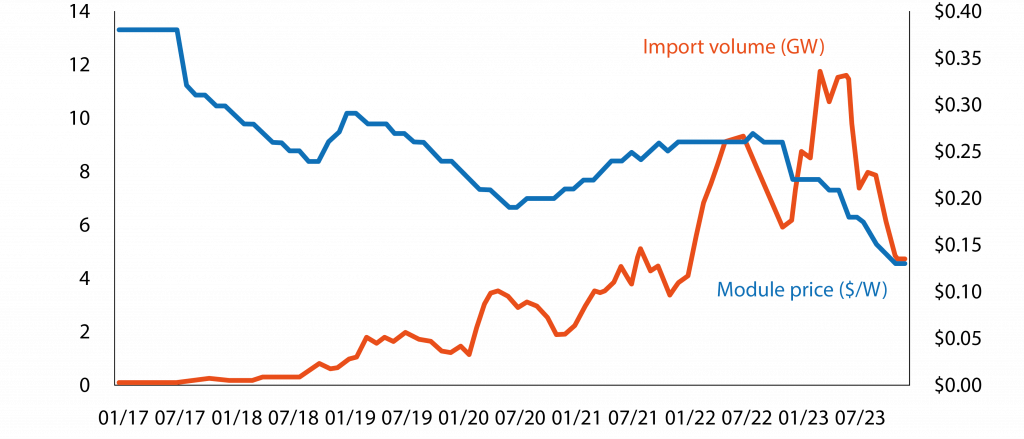

Since the price increases driven by supply-chain shortages between 2020 and 2022, module prices have crashed at record speed, reaching as low as $0.15/watt in September 2023 (Figure 3). Meanwhile, the EU has dramatically increased imports of Chinese solar panels to an average of 9.5 GW per month in the first nine months of 2023. This compares to total deployment in the EU in 2022 of around 36 GW.

Figure 3. EU imports of Chinese solar panels, volume (GW) and price ($/watt)

Source: Bruegel based on Ember dataset of Chinese solar PV exports.

Attempts in the US to stimulate domestic solar PV manufacturing offer another perspective on this cost differential. Support under the US Inflation Reduction Act is estimated at between $0.11 and $0.18 per watt (Bettoli et al 2022), meaning that public support will closely match, and possibly exceed the total cost of producing a solar panel in China. The US has also implemented tariffs on the import of Chinese solar panels14, a step the EU has not taken so far.

For European solar PV manufacturers the current situation is a deja-vu, as competing with their Chinese counterparts has once again become extremely difficult. The examples of Norwegian Crystals and Norsun, ingot and wafer producers respectively, illustrate the challenge.

In August 2023, Norwegian Crystals filed for insolvency15, while the following month Norsun announced a temporary wafer-production suspension because of an oversupply of low-priced Chinese modules causing inventory buildup and disruption in the value chain16.

In January 2024, the European Solar Manufacturing Council wrote to the European Commission asking for emergency measures17. The Council wrote that around half of the EU’s module assembly capacity was at risk of shutting down.

Under current market conditions, European producers can hardly compete with their Chinese counterparts. Solar producer industry groups have called for anti-dumping measures against Chinese solar panels18 and for additional trade measures to prevent solar panels produced with forced labour from entering the EU market (ESMC, 2023). The ghost of the 2013 tariffs on Chinese solar modules is looming again.

However, calls from European solar PV manufacturers for trade measures against Chinese panels are in stark contrast to what importers and installers of solar panels want. They warn the European Commission against initiating a trade defence investigation that could lead to the imposition of tariffs on Chinese solar PV products19.

The primary concern of these European companies is that implementing trade barriers on Chinese products would limit their access to essential, high-quality and affordable components necessary for the EU’s solar-power value chains.

This is particularly crucial given the EU’s limited domestic solar-panel manufacturing capacity. Imposing tariffs on Chinese solar products, they fear, could severely restrict the entire EU solar-power market.

These two contrasting positions illustrate Europe’s dilemma when it comes to solar PV manufacturing: how to strike the right balance between economic efficiency and geopolitical resilience, without slowing-down the green transition. In response, a reflection is needed on the reasons why the EU should or should not support domestic solar PV manufacturing in the first place.

3 Evaluating Europe’s case for solar manufacturing industrial policy

The current political consensus in Europe favours the approach under the Net-Zero Industry Act (see section 1) – that the EU should increase domestic manufacturing for solar and other technologies, setting an indicative benchmark to get close to or achieve a 40 percent share of deployment covered by domestic production.

This suggests, in part at least, an import-substitution strategy that marks a break with traditional European thinking rooted in principles of free trade and markets. A clear economic rationale is necessary to justify this shift.

3.1 Scoring solar against economic intervention criteria

Industrial policy involves government efforts to change the structure of an economy, by encouraging resources to move into sectors deemed desirable for future development, in a way that would otherwise not be driven by market forces alone (Meckling, 2021).

We consider there to be three reasons why the EU might want to support domestic manufacturing of clean technologies: 1) facilitating decarbonisation; 2) fostering green growth and creation of green jobs; 3) boosting geopolitical resilience (or strategic autonomy) in sectors considered to be important for the EU economy.

In the case of solar panels, there is no strong economic case for EU support for the first two justifications, and at best a weak case for the third.

First, the EU does not need domestic solar PV manufacturing to accelerate its decarbonisation. The global solar PV market is vastly oversupplied, and the EU is currently importing twice the volume of solar panels it manages to deploy20, creating a stockpile equivalent to well over one year’s annual deployment.

All indicators point to a further increase in this over-capacity, as Chinese companies expand aggressively, countries including the US and India ramp up their policy support to domestic manufacturing.

Overall, announced solar PV manufacturing expansion suggests that global capacity will double to over 1,000 GW by 2024-25 (Buckley and Dong, 2023), with China expected to maintain its 80 percent to 95 percent share of global supply chains (IEA, 2024). In 2023, global capacity ranged between 800 GW and 1,200 GW for different value-chain stages (IEA, 2023b).

Meanwhile, the IEA has calculated that the world should achieve annual installations of 650 GW solar by 2030 to be on track for net zero by 2050 (IEA, 2021). The speed of EU decarbonisation will continue to be defined by its capacity to speed-up deployment rather than by supply-side bottlenecks.

Second, the EU should not expect solar PV manufacturing to foster job creation and economic growth. In fact, the opposite might be true. Figure 4 shows that most solar-related jobs are in deployment rather than manufacturing. Solar PV manufacturing is not as job-intensive as deployment.

To create jobs in this sector, the EU would thus better focus on accelerating the deployment of solar energy. Imposing trade restrictions on Chinese solar panels would lead to higher costs, slowing deployment of panels and, possibly, a net-negative job effect. That would occur if more jobs were lost from a slowing of deployment than new jobs were created in possible new manufacturing facilities.

When it comes to economic growth, it is difficult to expect solar PV manufacturing to provide a major contribution, given that the EU has no comparative advantage in producing the existing generation of solar panels, and it is not clear where any unrealised advantage might lie.

Figure 4. Full-time equivalent jobs per 1 GW solar PV manufacturing or installation capacity

Source: Bruegel based on Ignaciuk (2023).

This leaves the third reason – resilience – as the only possible justification for supporting domestic manufacturing. The EU is fully dependent on China for solar panels and at least two conventional risks are associated with this.

The first is the economic risk that China might in the future make use of its predominant position in global solar PV manufacturing to distort the market and artificially obtain additional economic rents.

The second is the geopolitical risk that China might restrict solar-panel exports to certain countries to pursue geopolitical goals. The extent of both risks is unclear today.

3.2 The ‘China risk’

There is no evidence that China currently abuses its solar manufacturing market power to artificially extract economic rent. The solar market is vastly over-supplied, and historically profit margins have been tight and even negative.

It is currently more likely that the Chinese state provides an artificial advantage to domestic producers through, for example, cheap land and loans, allowing them to export at lower prices21.

Were China to begin extracting rents from solar exports, the competitiveness position of non-Chinese producers would improve, encouraging a gradual growth in manufacturing capacity elsewhere. An even more dramatic risk would be if there were a sudden interruption of all exports of Chinese solar panels, for whatever reasons.

Consider, for instance, a scenario in which the EU reaches a decision on forced labour in China and decides to ban associated imports of certain products, including solar panels22. Or consider a scenario in which China deliberately restricts the solar panel exports to Europe as a result of flaring geopolitical tensions.

Comparisons with the cut-off of Russian gas to Europe are far-fetched. While the Russian gas disruption created significant and immediate issues because of the need to heating homes and run power plants, an interruption in the supply of a manufactured goods like a solar panel is different. It would lead to a delay in the deployment of new solar panels, but would not affect the functioning of those already installed.

To measure the impact of such an event, one would have to estimate the resulting delay in European deployment of solar panels. This is understood as the time period between the end of Chinese supply and coming online of new supply.

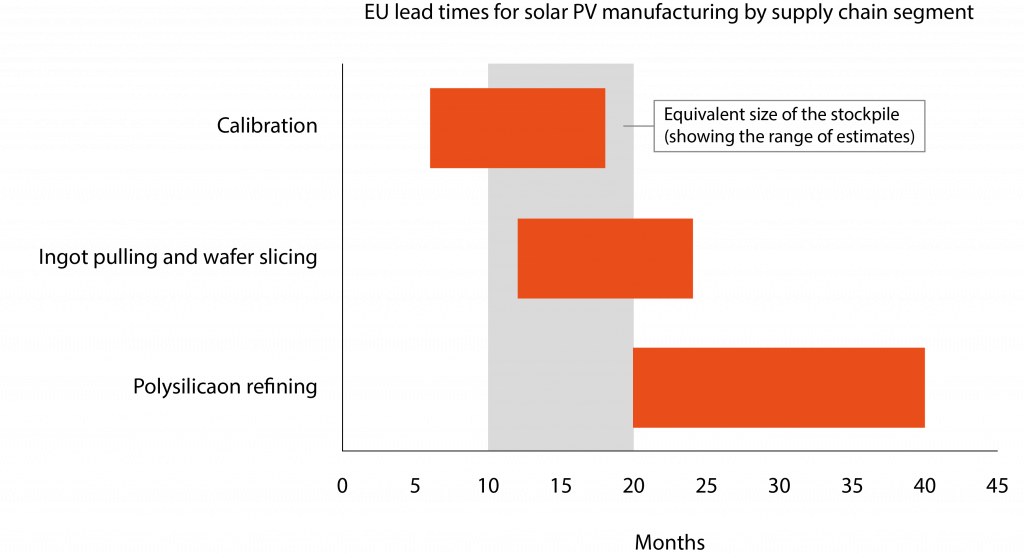

In Figure 5, manufacturing lead times for different stages of the value chain are estimated at between one and four years. These might be expedited in the extreme case of a sudden disruption, much like Europe was able to accelerate the deployment of liquified natural gas infrastructure following the Russian invasion of Ukraine.

4 Resilience priorities for solar policy

4.1 Stockpiling as a buffer solution

European companies already have a stockpile of an estimated 40 GW of solar panels23, equivalent to almost one year of total EU deployment (section 3.1). The resilience benefit of a stockpile is that it provides breathing space for industry to respond in case of a sudden event that disrupts imports while continuing business-as-usual deployment.

Figure 5 shows the size of the current stockpile in terms of current monthly installations, and the estimated time it would take to build new factories for key components of the solar value chain.

The figure shows that if all imports were ended tomorrow, the EU could develop its own manufacturing capacities, while running down its stockpile to continue current deployment rates, facing disruptions counted in months, not years.

Figure 5. The EU’s solar buffer

Notes: The figure shows the size of stockpile in months’ worth of deployment and the months needed to build new facilities.

Source: Bruegel based on IEA (2022).

If policymakers deem the risks of an immediate disruption to imports sufficiently high, the EU might explore more formal stockpiling arrangements to ensure supply-chain reliability. For example, it could require major importers to maintain a stockpile equivalent to three months (or more) of current import levels.

Frequent turnover of the stockpile should ensure that only the latest technology of panel is maintained. As global supply is diversified, this requirement can gradually be replaced by a requirement to demonstrate import resilience in case of disruption to a main supplier.

Stockpiling is a tried-and-tested approach, in line with current IEA recommendations for oil imports, which are substantially more important for economic security. Countries must maintain oil reserves equivalent to a minimum of 90 days’ worth of net oil imports24.

A solar stockpile is a relatively cheap tool for addressing import concern risks. A rough estimate is that the costs of storing 20 GW solar panels would be from €400 million to €550 million annually25. That is around 10 percent of the total value of the panels at current prices (around €4 billion).

By comparison, to provide these same 20 GW of supply, estimates based on US Inflation Reduction Act subsidy rates suggest a cost of around €2 billion annually in subsidies offered for the first years of a plant’s operation26.

While the EU might offer substantially lower subsidies than the US, they will still far exceed the costs of storing panels. From a short-term resilience perspective, stockpiling is cheaper.

4.2 Accelerating solar deployment

Accelerating the deployment of solar panels should be a much higher economic-security priority for Europe than developing its own manufacturing capabilities. This is because reliance on imported fossil fuels poses a greater threat to Europe’s economic security than reliance on imported solar panels.

Solar deployment is accelerating, with 56 GW installed in 2023 (SolarPower Europe, 2023), exceeding the annual installation of 54 GW needed to meet EU energy targets27. A combination of steadily decreasing solar costs and increased policy attention is driving this growth.

The European Commission has described the deployment of solar energy as the ‘kingpin’ of efforts to end dependency on Russian fossil fuels. Governments are encouraged to create ‘go-to areas’ where permitting is accelerated for renewable projects to hasten deployment (European Commission, 2022).

With no shortage of supply, policy efforts should be most concerned with guaranteeing and possibly exceeding current targets. This requires a continued focus on permitting and grid connection. Developers are ready to build, but they need permission from agencies and they need destinations for all the generated power.

In the coming years, this challenge will intensify as optimal locations become utilised. Grids will also face increasing pressure from large volumes of electricity generation aligned with periods of sunlight.

4.3 Gradual import diversification

The NZIA benchmark of meeting, or getting close to, a certain proportion of deployment needs with domestic manufacturing disregards the costs of promoting self-sufficiency compared to the use of cheaper imports (Tagliapietra et al 2023a).

Regrettably, no impact assessment has been performed to evaluate whether disrupting imports of solar panels would harm or improve overall EU energy and economic security. Economic resilience is hampered more by a high concentration of imports rather than high overall import volumes (Welslau and Zachmann, 2023).

It will be difficult to immediately diversify imports given Chinese dominance; however, in the second half of this decade it will likely become easier as heavily subsidised supply will come online in the US.

The EU might also act by supporting those countries with a comparative advantage (eg. potential for cheap electricity), but which need to develop their manufacturing capacities (BloombergNEF, 2021). The EU’s Global Gateway initiative to support green and digital infrastructure development in partner countries28 could serves as a strategic tool in this respect.

With investment commitments of up to €300 billion by 2027, this initiative is geared towards establishing sustainable and resilient supply chains across various sectors, including ensuring access to critical raw materials essential for solar PV technologies.

Its main regional focus is on Africa, where the EU has already pledged a significant investment of €150 billion with the Africa-Europe Investment Package.

5 Innovation, rather than European content, should justify manufacturing subsidies

5.1 Risks of intervention justified by domestic content

The notion of economic resilience as a justification for solar PV manufacturing subsidies is questionable, but clearly drives current European public discourse on the issue.

For example, the NZIA foresees resilience criteria in public procurement, meaning that governments can explicitly penalise bids from outside of Europe by providing additional subsidies to bids that prove European content.

This would bring with it two risks. First, given that European producers are currently highly uncompetitive compared to their Chinese counterparts, any policy that limits the ability of foreign competition will increase solar panel prices. The effect is likely to be slower solar PV deployment and slower decarbonisation.

Second, such a policy risks creating an industry that is completely dependent on subsidies. There is no guarantee that European solar manufacturing will be competitive with foreign competition once subsidies expire.

This is especially the case with the current generation of solar panels, on which Chinese companies benefit from huge economies of scale. Instead, Europe must focus on innovation and developing the next generation of solar PV if it is to stand any chance of growing some market share.

5.2 Support innovation in manufacturing

The manufacture of solar cells is a fast-moving sector, in which innovation drives substantial change and there is still plenty of space for further innovation. Companies that lead and commercialise such innovation may be able to carve out market shares in future solar products.

The best chance for Europe to develop some solar leadership is to support innovation and the commercialisation of emerging solar technologies, including new semiconducting technologies such as perovskite (Box 2).

Box 2. Innovation in solar cells

A solar cell contains a semiconductor material that transforms light energy into electrical energy. Innovations focus on how to enhance the efficiency of this transformation, and on reducing the cost and energy requirements of solar panel manufacture. Around 95 percent of today’s solar panels use cells with a silicon-based semiconductor material. Typical innovations include adding layers of material to the cell to improve the absorption and conversion of light energy.

For instance, a major ongoing industry shift is toward TOPCon cells, in which an additional insulating layer enhances electrical conductivity. An advantage of TOPCon cells is that they essentially rely on the current manufacturing supply chain.

Silicon-based solar cells installed on houses are based on single-junction architecture, with one layer of semiconducting material. For applications involving space travel, multi-junction cells are used instead: these have multiple layers of semiconducting material, improving efficiency but at a much higher cost. A major challenge for the manufacturing process is to reduce these costs to make them commercially viable for use on Earth.

A perhaps more radical innovation is the use of new semiconductor material, such as perovskite. A range of layers including plastics, metals and glass can be coated with this crystal-based material. A current industry focus is to combine a layer of perovskite material with a silicon-based cell (known as a tandem cell). This has the potential to substantially improve efficiencies as its production requires much less energy than crystalline silicon PV cells. The technology is not yet commercialised, but Oxford PV aims to bring its manufacturing plant in Berlin soon online. Alternative cell designs include ‘thin film’ such as cadmium telluride. These cells are made by depositing thin layers of semiconductor material onto a base layer. First Solar runs an integrated thin-film facility in the US serving about 15 percent of the overall domestic solar market.

The EU has an established tool for supporting early-stage innovation: the Innovation Fund. This fund receives its revenues from the EU emissions trading system, and its size is expressed in terms of permits.

Therefore, the recent rise in the price of permits from close to €20 per tonne of emissions to above €60 per tonne (reaching above €100 in early 2023) resulted in a substantial expansion of spending capacity. Part of this surge can be channelled toward new solar technologies.

Several facilities currently under construction have received funding from the Innovation Fund. Projects are evaluated against five criteria: 1) effectiveness of reducing greenhouse-gas emissions, 2) degree of innovation, 3) project maturity, 4) replicability, and 5) cost efficiency.

Funding involves a competitive process against other clean technologies with the idea of ensuring that European public money is targeted to the most promising projects. The approach contrasts with that taken under the US Inflation Reduction Act, which allows all projects meeting broader criteria apply for tax credits. The EU approach maximises the chance that supported projects contribute to sustainable economic growth.

Other EU-level instruments also support early-stage innovation in clean technologies. The Horizon Europe research programme spearheads the EU’s commitment to innovation with a €95.5 billion budget, emphasising climate and sustainability.

It includes the European Research Council (ERC) and the European Innovation Council (EIC) to nurture early-stage innovation. The ERC will allocate over €16 billion from 2021-2027 to pioneering research projects, while the EIC, with a €10.1 billion fund, offers startups and smaller companies financial backing through grants and equity, focusing on clean energy and smart technologies.

The European Institute of Innovation and Technology (EIT), supported by a €2.9 billion Horizon Europe budget, cultivates cross-sector partnerships for global challenges, with a significant portion dedicated to green industrial policy.

Reinforcing the EU’s innovation ecosystem, the European Investment Bank (EIB) supports investments in clean energy, efficiency and renewables. In 2022, the EIB allocated €17.5 billion to transport and industrial sectors, with €3.3 billion targeting clean technology projects and €10.4 billion for energy projects, including €4.4 billion for renewable energy.

Finally, InvestEU, an EU initiative to stimulate private investment in innovation and the green transition29, has a €26.1 billion EU budget guarantee to stimulate private investment in strategic areas, including sustainable infrastructure and innovation (Tagliapietra et al 2023b).

European subsidies are less successful at growing new technologies from demonstration to commercial status (McWilliams and Zachmann, 2021). This is a problem as the cost of financing is higher for emerging technologies and often is not provided by the market.

Public support for the commercial growth of technologies that offer a radical advantage over the current generation of solar panels is more likely to lead to the development of economically sustainable industries in Europe.

Radically new technologies might enable a new start for a competitive, self-sustaining EU eco-system of cell manufacturing. Developing and bringing to scale next-generation panels could contribute to the goal of accelerating decarbonisation, within the EU, but, importantly, also beyond.

The deployment of much utility-scale solar PV across Europe is driven by government auctions or subsidies30. To stimulate innovation, governments might increase available subsidies if developers can demonstrate certain characteristics of the manufactured panels.

To further promote innovation, governments could offer enhanced subsidies or higher bid limits for developers that show their solar panels excel in, for example, peak efficiency, low-light performance, recyclability and energy input requirements.

Maximum bid prices or even separate auctions could be designed for developers who can prove the use of an innovative panel design. Similar criteria should drive any support offered by the EIB.

5.3 Support innovation in recycling

In the EU, solar recycling is a legal requirement under the Waste Electrical and Electronic Equipment Directive31. The directive sets minimum waste collection and recovery targets for different product categories. Solar panels are in a category of electronic waste with a target set at 85 percent for recovery and 80 percent for reuse and recycling.

Producers of solar PV panels are responsible for the disposal and recycling of the modules they sell in the EU. A scheme financed by panel manufacturers and importers funds the collection of end-of-life panels, with pilot recycling lines in certain countries.

Effective recycling reduces reliance on imported materials. The EU can play a role in scaling up this industry by expanding funding and support mechanisms. Initiatives such as those under Horizon Europe32 and EIT RawMaterials Innovation Hub Central & West33 are paving the way.

Box 3. Recycling of end-of-life solar panels

The most widespread solar-panel recycling technology recovers only the aluminium frame, copper-containing junction box and sometimes the front glass panel. The central technical hurdle is the high-purity separation of encapsulated materials, which is vital for the economic viability of the recycling process (Granata et al 2022).

The value of recovered materials varies, with silver, copper, silicon and tin being the most lucrative, particularly silver, which, despite its lower concentration, is valued 500 to 800 times more than tin and copper, making it a prime target for recycling. Silver content and processing volumes are key to the profitability of PV recycling: for panels with high silver concentration (0.2 percent), recycling is economically viable without fees at volumes above 18,000 tonnes per year; below this threshold, fees are necessary to cover up to 46 percent of costs (Granata et al 2022). Panels with only 0.05 percent silver require fees for profitability, unless processed volumes exceed 43,000 tonnes annually. Optimal returns on investment are tied to both the timing of investment and silver-market prices, with the best outcomes predicted for early investments at higher silver prices and substantial processing volumes.

Emerging recycling technologies aim to refine the separation process and enhance the recovery of glass, silicon and metals. These technologies can be generally divided into physical, thermal and chemical methods (Pereira et al 2023). Among these, the Advanced Photolife Process stands out, claiming over 80 percent material recovery through a combination of physical, thermal and chemical methods (Granata et al 2022).

6 Conclusions

The approach under the NZIA of setting an indicative benchmark of about 40 percent for home production of different technologies raises significant concerns, which solar panels make plain. Supporting solar manufacturing purely for the sake of being European does not present clear advantages in terms of accelerated decarbonisation or increased economic growth.

Nor is the political focus on increasing economic resilience in this sector a valid justification for committing substantial public resources. Instead, more efficient strategies should be employed.

Measures including accelerating solar deployment, stockpiling to ensure a buffer in a worst-case scenario and diversifying import sources offer more pragmatic approaches to mitigate threats to European economic security arising from solar PV imports.

Manufacturing subsidies for the solar industry should prize innovation only. This criterion would ensure that funding would be directed toward technologies that offer genuine economic and climate benefits.

Finally, while a general over-reliance on imports from one country can be considered dangerous, the case of solar panels emphasises that an obsession with addressing this risk at individual product level is myopic. For the existing generation of mass-manufactured, energy-intensive solar panels, Europe will struggle to reclaim Chinese market share, and the case for trying is not well justified.

Europe can strengthen its economic resilience relative to China with an industrial policy that intervenes in sectors with greater potential to contribute to sustainable economic growth and alleviate decarbonisation bottlenecks.

Examples include the manufacture of wind turbines or exploiting Europe’s labour force and brand recognition for electric vehicles. Such an approach better leverages existing strengths and can contribute more effectively to the global push for clean energy.

Endnotes

1. The EU currently has 110 GW coal-fired capacity, 180 GW natural gas fired capacity, and 105 GW nuclear capacity. Average hourly demand in 2022 was 320 GW.

2. See SolarPower Europe press release of 12 December 2023, ‘New report: EU solar reaches record heights of 56 GW in 2023 but warns of clouds on the horizon’.

3. See Eurostat press release of 8 November 2023, ‘International trade in products related to green energy’.

4. Agreement on the NZIA on 6 February 2024 requires ratification by the European Parliament and Council of the EU. See Council of the EU press release of 6 February 2024, ‘Net-Zero Industry Act: Council and Parliament strike a deal to boost EU’s green industry’.

5. Ivan Penn and Ana Swanson, ‘Solar Company Says Audit Finds Forced Labor in Malaysian Factory’, The New York Times, 15 August 2023.

6. Sandra Enkhardt, ‘European solar manufacturers demand EU support’, PV Magazine, 12 September 2023.

7. We discuss here the silicon manufacturing route, which is by far the most common today. Innovation in the sector may also see development of new supply chain routes, which we discuss in section 5.

8. Usha CV Haley and George T Haley, ‘How Chinese Subsidies Changed the World’, Harvard Business Review, 25 April 2013.

9. See European Commission memo of 4 June 2013, ‘EU imposes provisional anti-dumping duties on Chinese solar panels’.

10. See European Commission press release of 2 December 2013, ‘EU imposes definitive measures on Chinese solar panels, confirms undertaking with Chinese solar panel exporters’.

11. Jorge Valero, ‘Commission scraps tariffs on Chinese solar panels’, Euractiv, 31 August 2018.

12. See answer given by the European Commission to a European Parliament question on ‘End of anti-dumping measures on imports of solar panels from China’, 27 October 2018.

13. Levelised cost of energy (LCOE) refers to a calculation of the average cost per unit of electricity generated by a particular energy source, such as solar PV, over its operational lifetime. It takes into account all the costs associated with the energy system – initial investment, operations, maintenance, the cost of fuel and the system’s expected lifetime. The LCOE enables comparison of different energy technologies on a consistent basis. In this context, ‘LCOE for solar PV’ refers to the cost of generating electricity using solar PV technology.

14. See US Department of Commerce press release of 18 August 2023, ‘Department of Commerce Issues Final Determination of Circumvention Inquiries of Solar Cells and Modules from China’.

15. Marco de Jonge Baas, ‘Noorse waferfabrikant Norwegian Crystals failliet’, Solar Magazine, 29 August 2023.

16. Valerie Thompson, ‘Norsun announces temporary wafer production halt, layoffs’, PV Magazine, 8 September 2023.

17. Kate Abnett, ‘Europe’s solar panel manufacturers ask EU for emergency support’, Reuters, 30 January 2024.

18. Henning Jauernig, Benedikt Müller-Arnold, Stefan Schultz und Gerald Traufetter, ‘Der deutsche Solarboom hängt an Chinas Tropf – kann das gut gehen?’ Der Spiegel, 27 October 2023.

19. Trade measures would “would injure the EU solar sector to the detriment of the EU’s own green energy transition at a critical moment in time”. See SolarPower Europe statement of 29 November 2023.

20. See Rystad Energy press release of 20 July 2023, ‘Europe hoarding Chinese solar panels as imports outpace installations; €7 billion sitting in warehouses’.

21. This is exactly what the EU is currently investigating Chinese electric vehicles for. An anti-dumping investigation is seeking to determine whether the Chinese state provides excessive support for automobile exports, leading to unfair competition with EU products. See European Commission press release of 4 October 2023, ‘Commission launches investigation on subsidised electric cars from China’.

22. The suspension of the EU-China Comprehensive Agreement on Investment (CAI) serves as a pertinent example of how concerns over forced labour can impact trade flows between the two countries. The CAI negotiations, which started in 2014 and concluded in December 2020, faced significant challenges because of concerns over forced labour, particularly in Xinjiang. Following EU sanctions against Chinese officials for human-rights violations, China imposed retaliatory sanctions on EU entities and officials. In May 2021, the European Parliament voted to suspend the ratification of the CAI, as long as China’s sanctions remain in place.

23. Much uncertainty surrounds this number. S&P Global reported industry estimates at 45 GW in August 2023; see Camilla Naschert, ‘Glut of inexpensive solar panels in Europe boosts project economics’, S&P Global, 21 August 2023. Rystad Energy made multiple estimates in 2023, ranging between 40 GW and 80 GW.

24. See IEA website: https://www.iea.org/reports/oil-security-policy.

25. 20 GW is an upper-bound estimate for three months EU deployment. The authors assume a typical solar panel of 1.5 square metres and 300 W capacity. They assume that the cost of storage is €50 per square metre, insurance costs are 1 percent of the value of stored panels, and overhead costs at 20 percent of storage and insurance cost. Finally, it is assumed that solar panels can be stacked 15 rows high in a warehouse. For estimates of the storage cost in Europe, see https://ecommercenews.eu/warehouse-storage/ and https://www.statista.com/statistics/527840/warehouse-primary-rent-cost-logistics-market-france-europe/.

26. With a subsidy rate of €0.10 per watt.

27. The EU Solar Strategy cites required 45 GW capacity, but this is given in AC terms. Assuming a conversion factor of 1.2 to account for the DC conversion, this figure translates to approximately 54 GW in DC terms.

28. See European Commission Global Gateway webpage.

29. See https://investeu.europa.eu/index_en.

30. See IEA, https://www.iea.org/data-and-statistics/charts/europe-solar-and-wind-forecast-by-policy-and-procurement-type-2023-2024.

31. See the European Commission Waste from Electrical and Electronic Equipment (WEEE) webpage.

32. See European Commission CORDIS webpage.

33. See EIT RawMaterials webpage.

References

Andres, P (2022) ‘Was the Trade War Justified? Solar PV Innovation in Europe and the Impact of the “China Shock”’, Working Paper 404, Centre for Climate Change Economics and Policy.

Basore, P and D Feldman (2022) Solar Photovoltaics: Supply Chain Deep Dive Assessment, Technical Report, US Department of Energy Office of Scientific and Technical Information.

Bettoli, A, T Nauclér, T Nyheim, A Schlosser and C Staudt (2022) Rebuilding Europe’s Solar Supply Chain, McKinsey.

Bloom, N, P Romer, SJ Terry, and J Van Reenen (2021) ‘Trapped Factors and China’s Impact on Global Growth’, The Economic Journal 131(633): 156–91.

BloombergNEF (2021) ‘Producing Battery Materials in the DRC Could Lower Supply-Chain Emissions and Add Value to the Country’s Cobalt’, 24 November.

Buckley, T and X Dong (2023) Solar Pivot: A Massive Global Solar Boom Is Disrupting Energy Markets and Speeding the Transition, Climate Energy Finance.

Cao, J, and F Groba (2013) ‘Chinese Renewable Energy Technology Exports: The Role of Policy, Innovation and Markets’, Discussion Papers 1263, DIW Berlin.

Carvalho, M, A Dechezleprêtre, and M Glachant (2017) ‘Understanding the Dynamics of Global Value Chains for Solar Photovoltaic Technologies’, World Intellectual Property Organization (WIPO) Economic Research Working Paper Series 40.

Crawford, A and L Murphy (2023) Over-Exposed: Uyghur Region Exposure Assessment for Solar Industry Sourcing, Sheffield Hallam University Helena Kennedy Centre for International Justice.

ESMC (2023) ‘How to address the unsustainably low PV module prices to ensure a renaissance of the PV industry in Europe’, Position Paper, European Solar Manufacturing Council.

ETIP PV (2023) PV Manufacturing in Europe: Understanding the Value Chain for a Successful Industrial Policy, ETIP PV Industry Working Group White Paper, European Technology and Innovation Platform for Photovoltaics. European Commission (2022a) ‘EU Solar Energy Strategy’, COM(2022) 221 final.

European Commission (2022b) ‘Proposal for a Regulation on prohibiting products made with forced labour on the Union market’, COM(2022) 453 final.

European Commission (2023a) ‘European Wind Power Action Plan’, COM(2023) 669 final.

European Commission (2023b) ‘Proposal for a Regulation establishing a framework for ensuring a secure and sustainable supply of critical raw materials’, COM(2023) 160 final.

Granata, G, P Altimari, F Pagnanelli and J De Greef (2022) ‘Recycling of solar photovoltaic panels: Techno-economic assessment in waste management perspective’, Journal of Cleaner Production 363: 132384.

Grau, T, M Huo and K Neuhoff (2012) ‘Survey of photovoltaic industry and policy in Germany and China’, Energy Policy 51: 20–37.

IEA (2022) Special Report on Solar PV Global Supply Chains, International Energy Agency.

IEA (2023a) The State of Clean Technology Manufacturing, International Energy Agency.

IEA (2023b) Energy Technology Perspectives 2023, International Energy Agency.

IEA (2024) Renewables 2023, International Energy Agency.

McWilliams, B and G Zachmann (2021) ‘Commercialisation contracts: European support for low-carbon technology deployment’, Policy Contribution 15/2021, Bruegel.

McWilliam, B, G Sgaravatti, S Tagliapietra and G Zachmann (2024) ‘Europe’s under-the-radar industrial policy: intervention in electricity pricing’, Policy Brief 01/2024, Bruegel.

Meckling, J (2021) ‘Making Industrial Policy Work for Decarbonization’, Global Environmental Politics, 21(4): 134–47.

OHCHR (2022) Assessment of Human Rights Concerns in the Xinjiang Uyghur Autonomous Region, People’s Republic of China, Country Reports, Office of the High Commissioner for Human Rights.

Pereira, MB, G Botelho Meireles de Souza, DC Romano Espinosa, LV Pavão, CG Alonso, VF Cabral and L Cardozo-Filho (2023) ‘Simultaneous recycling of waste solar panels and treatment of persistent organic compounds via supercritical water technology’, Environmental Pollution 335: 122331.

SolarPower Europe (2023) EU Market Outlook For Solar Power 2023 – 2027.

Tagliapietra, S, R Veugelers and J Zettelmeyer (2023a) ‘Rebooting the European Union’s Net Zero Industry Act’, Policy Brief 15/2023, Bruegel.

Tagliapietra, S, R Veugelers and C Trasi (2023b) ‘Europe’s green industrial policy’, in S Tagliapietra and R Veugelers (eds) Sparking Europe’s New Industrial Revolution. A Policy for Net Zero, Growth and Resilience, Blueprint 33, Bruegel.

The White House (2021) ‘Executive Order on America’s Supply Chains’, 24 February.

Welslau, L and G Zachmann (2023) ‘Is Europe Failing on Import Diversification?’ Bruegel Blog, 20 February.

Woodhouse, M, D Feldman, V Ramasamy, B Smith, T Silverman, T Barnes … R Margolis (2021) Research and Development Priorities to Advance Solar Photovoltaic Lifecycle Costs and Performance, Technical Report, U.S. Department of Energy Office of Scientific and Technical Information.

Zhang, Y, P Xie, Y Huang, C Liao and D Zhao (2021) ‘Evolution of Solar Photovoltaic Policies and Industry in China’, IOP Conference Series: Earth and Environmental Science 651(2): 022050.

This article is based on Bruegel Policy Brief 02/2024 | February 2024.