How to finance the EU’s decarbonisation plan

Ugnė Keliauskaitė is a Research Assistant, Ben McWilliams is an Affiliate Fellow, Giovanni Sgaravatti is a Research Analyst, and Simone Tagliapietra is a Senior Fellow, all at Bruegel

Executive summary

By 2030, the European Union must reduce emissions from the heating and cooling of buildings – responsible for 13 percent of EU emissions – by the equivalent of the annual emissions of Slovakia. This requires a near tripling of the current decarbonisation rate. But the time gap between high upfront costs and long-term payback from renovation works deter consumers from investing in energy renovation.

To address these challenges, the EU has introduced a policy toolkit that includes strengthened price signals against fossil-fuel heating through emissions trading and setting energy-consumption reduction targets in the Energy Performance Building Directive (EPBD).

EU countries must take the EPBD targets seriously and implement policies to accelerate building retrofits and the adoption of clean heating. If they don’t, there is a risk that EU climate targets will not be met, and the costs for households of subjecting domestic heating to emissions trading could be almost twice the higher costs seen during the 2022 energy crisis.

We estimate that achieving the EPBD’s energy savings targets requires filling an investment gap of about €150 billion per year up to 2030. This is a daunting but feasible goal. By leveraging energy savings from electrification and retrofitting to reduce renovation costs, the investment gap could be more than halved. Additionally, effective use of EU funds and emissions trading revenues will further shrink the gap.

A mix of grants, preferential loans and obligations is needed, as no single policy will speed up energy renovations. Prioritising grants for the worst-performing buildings, often occupied by vulnerable consumers, will yield climate benefits and benefits in terms of improved air quality, health, productivity, energy security and lower future government outlays to alleviate energy poverty.

Traditional public subsidies have not successfully engaged the banking sector, which now must help to foster private-public financing mechanisms. Countries also need to adjust relative energy prices for heating through taxation and subsidies and expand one-stop-shops to streamline the renovation process for consumers.

1 Introduction

The heating and cooling of buildings using fossil fuels is responsible for 13 percent of European Union emissions (EEA, 2023a). Electricity use in buildings accounts for another 14 percent. While new buildings are designed increasingly to be nearly-zero or zero emission, three-quarters of the existing EU building stock is energy inefficient (European Parliament, 2024). Building renovations can cut heating bills by up to 85 percent (Abdoos et al 2024).

The EU energy performance of buildings directive (EPBD, EU/2024/1275), updated in 2024, sets targets for such energy savings for 2030 and 2033. However, we estimate that meeting the 2030 target requires a €149 billion annual investment gap to be bridged, and emissions reductions from building heating and cooling would have to triple.

Another EU rule – an emissions trading system (ETS) for the fossil fuels consumed by buildings and road transport – also has the potential to significantly impact household choices related to heating. The system (known as ETS2 because it will initially be separate from the main EU ETS) will change the energy price paid by households depending on the carbon price within the system and the energy mix used for heating.

The introduction of ETS2 in 2027 is expected, alongside the EPBD, to stimulate necessary investments in buildings by aligning price signals to reflect the environmental and economic impact of emissions. However, ETS2 could also worsen energy poverty unless public financing schemes are set up.

This policy brief discusses the challenges of meeting EPBD targets and introducing ETS2 smoothly, analyses the barriers holding up home renovation investments and assesses the impact of ETS2 on households. It also explores potential public financing tools, discusses trade-offs in designing public financing schemes and sets out policy recommendations.

2 Europe’s buildings-related emissions are not falling fast enough

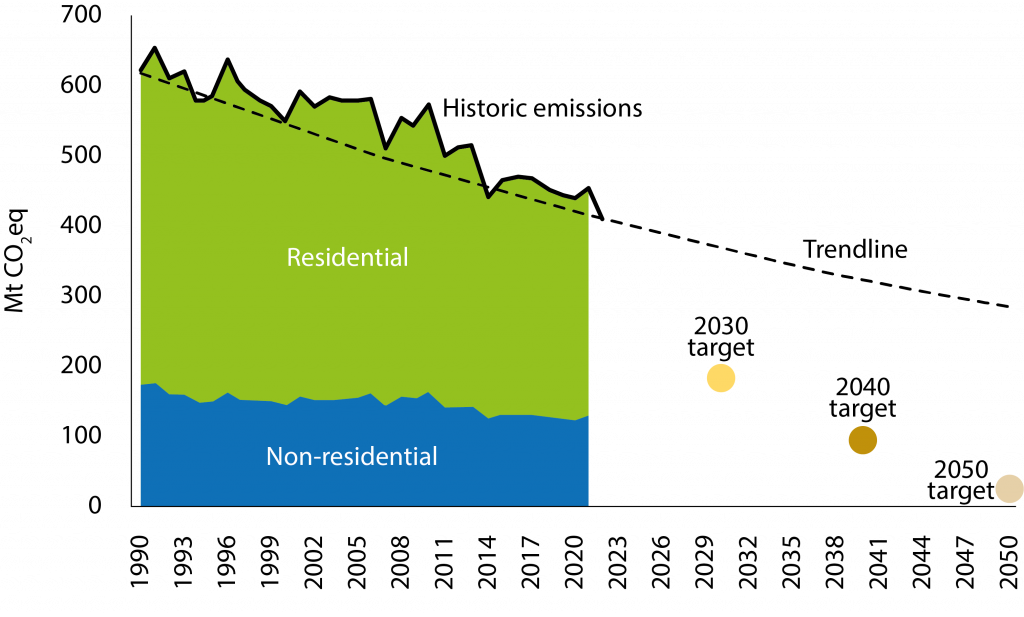

From 2005 to 2022, emissions from the EU’s building stock fell by 29 percent1. To meet the 2030 climate target, buildings emissions need to be reduced by 55 percent compared to 20222, meaning that annual reductions must almost triple (Figure 1).

2.1 Energy renovations

Accelerating emission reductions requires both deploying clean-energy solutions and energy retrofits to improve the thermal insulation of buildings. Clean-energy solutions involve the deployment of heat pumps and the greening and expansion of district-heating networks, which are centralised systems that distribute heating and hot water to buildings.

We define energy renovations as interventions that result in thermal insulation improvements and/or switching to cleaner fuels in heating and cooling systems (see the online annex for the complete list). From 2016 to 2020, 1 percent of EU buildings were renovated annually, with the rate for non-residential buildings at only 0.6 percent (Bredahl et al 2024)3. Deep renovations – resulting in energy savings of 60 percent or more (European Commission, 2019) – were done for only 0.2 percent of residential and 0.3 percent of the non-residential building stock.

Figure 1. Fossil-fuel use in heating and cooling in residential and non-residential sectors, emissions reductions, 1990-2022, Mt/CO2eq

Note: Emissions from agriculture, forestry and fishing related buildings are excluded.

Source: Bruegel based on EEA and UNFCCC.

A 2020 European Commission strategy, known as the Renovation Wave, aimed to double energy renovation rates, promote deep energy renovations and renovate 35 million building units by 2030. More energy efficient buildings will be important to integrate additional electricity demand smoothly into power grids.

Without efficiency improvements, meeting current heating demand in the EU through electricity would increase electricity demand in winter months by at least a third4, with even greater electricity generation capacity required for unfavourable cloudy and non-windy weeks.

There is unfortunately no good data on rates of energy renovation in the EU. Literature and institutional documents typically refer to the 1 percent rate estimated from 2012-2016 data (European Commission, 2019). There is also no standardised definition of the renovation rate.

Some datasets and studies have helped provide a clearer picture but use the same data as a basis for their analyses5. It is therefore not possible to assess thoroughly the latest trends in building energy efficiency, nor to gauge the impacts of the COVID-19 pandemic and the subsequent economic-recovery measures or the energy crisis.

The literature does converge, however, on the existence of an energy-efficiency gap, and in calling for more energy renovations to meet climate targets (Eichhammer et al 2023; Gerarden et al 2017; Bertoldi et al 2021a).

Figure 2. Percentage change per country in fossil-fuel emissions from building heating and cooling, 2005-2021

Note: The 2030 milestone of -68 percent compared to 2005 corresponds to the -60 percent compared to the 2015 level set in the PRIMES model’s MIX scenario, the leading model employed by the European Commission for energy policy assessment. The size of the circle in the figure represents that country’s share of total EU emissions associated with buildings, ranging from 0.02 percent (Malta) to 26 percent (Germany).

Source: Bruegel based on UNFCCC and EU Buildings Stock Observatory.

Figure 2 shows progress by country in reducing emissions associated with buildings. Most countries have cut emissions from buildings, but Malta, Lithuania, Romania and Luxembourg have seen increases. A critical bloc of Germany, Italy, Poland, the Netherlands and Belgium accounts for 60 percent of the EU’s buildings emissions. Teir building stocks have relatively high carbon intensities. On current trajectories, they are making insufficient progress towards 2030 targets.

2.2 Progress on deploying clean-energy solutions

In 2022 and 2023, six million heat pumps were installed across Europe (EU, Norway and the UK), bringing the total estimated stock to 23 million (McWilliams et al 2024)6. Modelling from the European Commission sets a target for 2030 of 60 million heat-pump installations (European Commission, 2024), replacing part of the 68 million gas and 18 million oil boilers currently installed in EU residential buildings (Carlsson et al 2023). In fact, fossil fuels and firewood still dominate the heating and cooling fuel mix of EU households (Figure 3).

Figure 3. Final energy consumption of heating and cooling in households by fuel type, 2021

Note: Firewood stoves convert 16 percent to 18 percent of firewood potential energy to heat, coal about 70 percent, gas and diesel about 90 percent; heat pumps can achieve efficiency as high as 400 percent. Therefore, heat pump adoption will displace energy consumption from fossil-fuel heating at a rate faster than 1:1. For Sweden heat-pumps are categorised under electricity.

Source: Bruegel based on Eurostat.

Slightly more than five million heat-pump installations annually are thus needed for the EU to meet its 2030 target. After a rapid increase in 2022, the rate of growth of heat-pumps sales slowed in each quarter of 20237, implying that the deployment of heat pumps must quickly reverse course and accelerate8.

District heating today accounts for 12 percent of final energy use for space and water heating, with 27 percent coming from biomass, biofuels and renewable waste (European Commission, 2021c). District heating is mostly present in Scandinavian and Baltic countries, meeting 50 percent of Swedish heating demand, while being almost non-existent in Belgium, Ireland and Spain (European Commission, 2021c).

District heating is generally obtained from cogeneration – the production by power plants of thermal energy alongside electricity – but can also come from waste heat from energy-intensive factories and lower-temperature sources including water-treatment plants, metro stations and data centres. District heating could meet more than half of EU heating demand and would imply a total energy system cost reduction of 17 percent to 20 percent (Jiménez-Navarro et al 2019), because of use of excess heat that would otherwise be wasted.

Maximising decarbonised district heating in dense urban areas can cut costs and provide flexibility to electricity networks (Brugger et al 2023). Tere are no specific EU targets on district heating, yet it has vast potential.

Accelerating energy renovations could lift seven million Europeans out of energy poverty each year, progressively reducing the need for public support to help vulnerable households with energy bills

3 The lack of an attractive investment case

Decisions to deploy clean energy solutions or insulate buildings are made by companies and households, but the rate of deployment has been undermined by weak economic incentives. Most EU governments have not implemented policies to change this situation.

Weak investment has five main reasons. First, energy renovations require high upfront costs and offer returns over the long term, making them less appealing to households and small and medium-sized companies, which discount future income more heavily than governments or large companies9.

Second, unlike electricity, fossil-fuel prices for heating do not reflect the cost of their carbon emissions, and EU energy taxation favours fossil fuels, an issue only partly addressed by ETS2.

Third, many households, especially poorer households, and small businesses lack access to funds for renovations and face borrowing difficulties.

Fourth, a third of EU residents live in rented accommodation, where tenants pay energy bills but landlords are responsible for renovations, creating split incentives.

Lastly, information barriers, construction-related inconvenience and administrative complexities add non-monetary costs to renovation projects.

3.1 The long wait for economic returns

For energy renovations, discount rates – the rate at which future cash flows are valued today – are generally assessed between 7 percent and 36 percent (Andersen et al 2020)10. Low-income households are typically more uncertain about the future, leading them to discount future savings more than high-income households (Samwick, 1997).

This lack of a viable investment case because of high discount rates is a major barrier to energy renovations. Table 1 outlines a modelling exercise estimating the net present value of deep renovations for a German household living in an apartment or a single-family house relying on either gas, oil or coal heating (in brackets), for four scenarios with different energy prices.

The net present value is computed by subtracting the costs of a deep renovation11 from the discounted value of the resulting future energy savings for 30 years. Cells in green show that the present value of the investment is positive for all fuel types; cells in grey show that the present value is positive only for some fuels; and cells in red show that the present value is negative for all fuels.

Given retail energy prices at the time of writing and a carbon price of €60 per tonne12 (scenario 1), there is no economic case for such an investment for households currently relying on gas and oil boilers, notwithstanding public support13. The investment case becomes positive for all technologies only when relative prices change, especially in scenarios 2 and 4, in which the electricity price halves.

Without government support and with a discount rate above 5 percent, the net present value of deep renovations remains negative, except for coal-heated apartments in the high carbon price scenario.

Table 1. Net-present value of deep renovation including fuel switching for a German household by fuel type (numbers in brackets: gas, oil, coal) and under different price assumptions

Note: The model shows the 30-year net present value of a deep energy renovation for a German household living in either a 70m² apartment or a 130m² house. The renovation costs assumed are €19,000 for the apartment and €45,000 for the house. The energy price assumed for gas, heating oil and coal is €0.11/KWh. Energy efficiency is assumed at 70 percent for the coal stove, 90 percent for the gas and diesel boilers and 300 percent for heat pumps. See the online annex for emission factors. To avoid double counting of benefits, the increase in property value is excluded from our net present value computations, as the literature shows that higher housing values after energy renovations largely correspond to the expected future energy cost savings.

Source: Bruegel.

3.2 Electricity is relatively overpriced

While heat pumps are on average three times more energy efficient than gas boilers14 (Carlsson et al 2023), consumers in Europe can still face higher running costs when switching to clean technology. This influences the payback period for a heat pump. At 300 percent efficiency, the electricity-to-gas price ratio for pay-back should be around three to one, while a two to one ratio would incentivise the switch in virtually all cases.

This is partly because energy taxes are applied disproportionally on electricity compared to heating oil, natural gas, coal and biomass. Additionally, network and other tariffs are often added to the electricity bills of households and smaller companies to maintain lower prices for energy-intensive companies (Sgaravatti, 2024).

Levies intended to support renewables deployment are also typically charged on electricity bills rather than natural gas bills. Pure energy costs for electricity are currently higher than gas, but this is likely to decrease with greater renewable deployment and the introduction of ETS2.

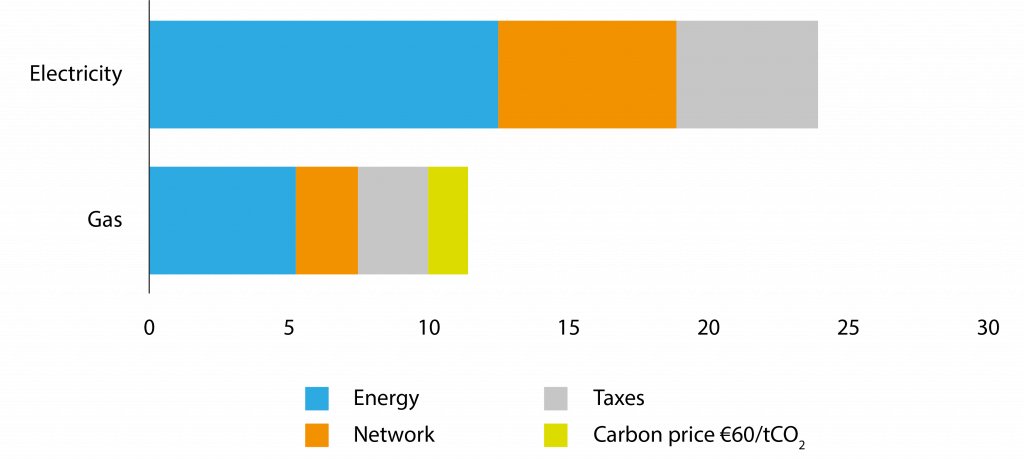

On average, in the EU, electricity excise duties exceed gas taxes more than twofold (Figure 4). Progress in the use of renewables for heating buildings has been stagnant, largely relying on biomass. The current taxation framework does not align with EU climate and energy objectives (Renewable Energy Directive, (EU) 2023/2413) and fails to incentivise investments in clean technology.

Figure 4. Composition of electricity and gas prices for households in the EU, eurocents/KWh, May 2024

Note: Because of the greater efficiency of electrical appliances, particularly heat pumps, significantly less electricity is needed than gas to deliver the same energy services.

Source: Bruegel based on Eurostat and Household Energy Price Index by VaasaETT.

3.3 Lack of upfront capital and borrowing constraints

Renovating a property to improve its energy performance can require an investment comparable to a household’s annual income. A 2023 German survey found that 41 percent of homeowners cited financial constraints as the main barrier to energy upgrades, rising to 68 percent among low-income households compared to 29 percent of high-income households (Romer and Salzgeber, 2023).

Low-income households struggle to borrow for renovation because of negative creditworthiness assessments by banks. Their risk profiles significantly influence loan approval and interest rates (Biere-Arenas et al 2021).

3.4 Split incentives

Landlords make energy-renovation decisions, while tenants consume and pay for the energy. Even when controlling for income and other characteristics, renters are significantly less likely to make energy-efficiency investments, while owner-occupied dwellings are much more likely to have energy-enhancing properties, such as ceiling insulation (Gerarden et al 2017).

Additionally, owners and tenants of apartments often cannot undertake significant energy-efficiency investments without the agreement of other apartment owners in the same building.

3.5 Administrative burden and disaggregated demand

Finding renovation technicians, evaluating the financial and non-financial benefits of renovation, obtaining a bank loan, applying for public support, navigating legal requirements and obtaining permits, awarding and overseeing multiple contractors, and finalising the work with guarantees are recurring and time-intensive steps in deep renovations (Biere-Arenas et al 2021).

These processes demand considerable time and expertise and might deter home and business owners. Moreover, the inability to aggregate multiple projects leads to high transaction costs for small single contracts and prevents the exploitation of economies of scale (Biere-Arenas et al 2021).

Box 1. Hits and misses in energy-efficient renovation support schemes

Italy’s ‘Superbonus’ scheme offers a 110 percent tax credit as an incentive for energy-efficient renovation. So far, the public costs have far exceeded expectations – it was estimated to cost €35 billion over 15 years but has cost €120 billion (6 percent of Italian GDP) in less than four years, raising Italy’s debt and contributing to a breach of EU fiscal rules15.

– Because the tax credit covered renovation costs fully, households had no incentive to negotiate prices, leading to significant cost spikes.

– Only 4 percent of Italian buildings (about 500,000 buildings) have undergone renovations under the scheme (Arcano et al 2024).

– The programme has favoured wealthier households (Ciminelli and Schwellnus, 2024) but has been narrowed to focus on low-income families, with an expected reduction in uptake (UpB, 2023). The programme is set to end in 2026.

Germany approved a bill to phase out new fossil fuel domestic boilers by 2024 but faced backlash because of long waiting times for replacement subsidies and a cut in subsidies in early 2023, making even the cheapest heat pumps more expensive than gas boilers (Dempster and Huckstep, 2024). Lack of skilled fitters and insufficient electricity supply for heat pumps also caused problems16. The scheme actually led to the share of fossil gas and oil heating systems rising, and the boiler ban deadline was pushed to 2028, making it likely that Germany will miss its 2030 climate targets17.

France’s éco-Prêt à Taux Zéro (éco-PTZ) programme ran from 2009 to 2023, offering interest-free loans for energy-efficiency upgrades of primary residences built before 1990. In 2015, the government’s €40 million investment mobilised €480 million in private investment18. This approach showed the potential for cutting emissions by using limited public money to leverage private finance.

– Zero-interest renovation loans boosted renovation rates in the programme’s first two years (Dastgerdi et al 2022).

– Take-up was higher among high-income households, who are more likely to own property and be willing to take on debt. Low-income households saw less significant efficiency gains from renovations.

4 Europe’s new carbon price is a revolutionary step

In May 2023, EU countries agreed to introduce a second emissions trading scheme (ETS2). This will put a price on emissions from direct fuel combustion, including gas and oil boilers in private homes, and fuel combustion in road transport19.

Taking effect in 2027, ETS2 will require upstream fossil-fuel suppliers to surrender carbon certificates equivalent to the emissions generated by consumers of their fuels. These suppliers are expected to pass through the cost of certificates in the form of higher fuel prices.

Carbon pricing could impact energy bills significantly, making it more attractive to renovate buildings by adjusting relative prices. The extent of this impact will depend on the prevailing market price for carbon permits, which is influenced by supply and demand dynamics.

The European Commission has suggested that from 2027 to 2030, efforts will be made to keep the ETS2 price below €45 per tonne of CO220 (in 2020 prices, or €60 in 2027 prices)21. Although the market will determine prices, a reserve will be established to manage price volatility by releasing more carbon allowances if prices rise too quickly or too high.

The reserve will hold 600 million allowances, or 18 percent of the ETS2 emissions cap between 2027 and 2030. European Commission (2021) estimates suggest the price could range between €48 and €80 if the EU plan to cut emissions by 55 percent by 2030 compared to 1990 is fully implemented.

However, if countries do not act to decarbonise ETS2 sectors more quickly, prices could skyrocket to between €200 and €300 (Fotiou et al 2024; Müller and Nesselhauf, 2023), indicating that the allowance endowment of the reserve may be insufficient to contain prices.

Such high carbon prices would have a similar impact to the 2022 energy crisis. Our calculations suggest that an ETS2 price of €200 would increase the energy bills of the average EU household with a gas boiler by more than they rose during the 2022 energy crisis (Figure 5), calling into question the viability of the whole mechanism.

During the energy crisis, governments earmarked €540 billion in energy subsidies for final consumers (Sgaravatti et al 2023), suggesting that the revenues obtained from high ETS2 prices would also be returned to households as compensation.

Figure 5. Yearly financial impact (additional heating cost in €) on the average EU household with a gas boiler

Note: the figure does not include support to households that might be provided by governments through the use of ETS2 revenues in case of high ETS2 prices.

Source: Bruegel.

The introduction of ETS2 will help in decarbonising buildings. However, it could lead to very high carbon prices, undermining its social and political acceptability and jeopardising both building decarbonisation policies and the European Green Deal more generally.

Implementing the decarbonisation and energy efficiency in buildings legislation is fundamental because it will directly tackle high energy prices. EU laws on emissions reductions in non-ETS sectors, renewable energy and energy efficiency, alongside the EPBD, set targets and standards that incentivise energy efficiency, increase the use of renewable energy and provide technical support for renovation.

Collectively, these policies should lower energy bills, stabilise costs and improve living conditions, particularly benefiting households struggling with high energy prices.

5 Missing money: the need for more investment

5.1 The investment gap

We estimated that, from 2024 to 2030, meeting the EPBD targets will requires annual investments of €297 billion (for details see the online annex)22. Reaching this target requires doubling renovation rates from the current 1 percent. The overall (public and private) investment gap would therefore be €149 billion per year.

Two European instruments fill some of this gap. First, the Recovery and Resilience Facility, the EU’s post-COVID-19 economic recovery fund, is estimated to provide €12 billion annually until 2027. Second, if half of the ETS2 revenues are reinvested in energy renovations23, an additional €30 billion could be made available from 2027.

This leaves an annual investment gap of €134 billion up to 2027, and €119 billion thereafter, or approximately 0.7 percent of EU GDP. A substantially larger sum is currently spent on building renovations – though not necessarily aimed at cutting emissions (for example, extensions).

In most countries with available data, the required additional energy-efficiency investments are substantially less than overall renovation expenditures. For instance, overall building renovations in Germany in 2023 amounted to €145 billion, compared to a €42 billion investment gap for energy renovations (see table A.6).

Figure 6 shows the required investments by country to meet EPBD targets. Germany requires the most additional investment in absolute terms at just over €40 billion annually.

In relative terms, Portugal has the largest investments gap at 1.6 percent of GDP. Figure 6 also shows that the EPBD targets place the greatest renovation burden on non-residential buildings.

Figure 6. Additional annual investment needs for energy renovations, € billions and % of GDP

Note: See the online annex for a detailed explanation.

Source: Bruegel.

5.2 EU financing

The Recovery and Resilience Facility has increased funding for energy-efficient improvements, providing €73 billion for 2021-2027 (Baccianti, 2023, in which figures are in current prices). This is the first European policy instrument with such a significant volume of funding dedicated to buildings energy efficiency and renovation. However, the overall impact of this funding on energy renovations remains unclear.

The EU budget, the European Regional Development Fund, the Cohesion Fund, and the Just Transition Fund contribute to these efforts (Ivanova et al 2023). Funding for building renovations and energy-efficiency projects was slightly increased in the most recent EU budget for 2021-2027, totalling around €17 billion (Baccianti, 2023). This amount is not included in our calculation of the investment gap as it does not represent a significant change from previous periods.

5.3 New funding: ETS and ETS2 revenues and the Social Climate Fund

Carbon prices have increased significantly in recent years and revenues from auctioning carbon allowances rose from €5 billion in 2017 to €30 billion in 2022 (EEA, 2023b).

Over the past decade, EU countries reported allocating 76 percent of these revenues to climate, renewable energy and energy-efficiency initiatives. Tis increased stream of public revenues and its claimed allocation to energy efficiency raises hopes for increased funding for energy renovations in the future.

However, reporting and accountability on the use of these revenues are considered poor, with several counties categorising compensation for high carbon prices given to industrial firms as climate action (WWF, 2022; Branner et al 2022). Reporting and accountability shortcomings make it difficult to gauge the role that ETS revenues could play in fostering energy renovations.

Auctioning of ETS2 allowances will also generate substantial revenues, ranging from €50 billion annually at a carbon price of €45 to €217 billion annually at a carbon price of €200. A maximum of €65 billion of these revenues from 2026-2032 will fund the Social Climate Fund24, which is intended to support vulnerable households, micro-enterprises and transport users who face higher costs.

This fund will not receive additional top-ups if carbon prices exceed target levels. To access the SCF, by June 2025 EU countries must develop social climate plans that outline how they will use these funds to support vulnerable communities. Countries must contribute at least another 25 percent of the costs of their social climate plans, increasing SCF resources to at least €87 billion (Cludius et al 2023).

The remaining ETS2 revenues will be managed by national governments. Assuming an ETS2 carbon price of €60, overall revenues managed at the national level will be €275 billion, about two-thirds of the total expected revenues of €362 billion (Figure 7). Governments must use this revenue for deployment of low-emission solutions in transport and heating, or to mitigate social impacts.

This creates a trade-off between compensating consumers and encouraging low-carbon investment, and between support measures for decarbonisation of heating and cooling or transport. Efficient use of this nationally-managed funding will be crucial for social acceptance of ETS2 and achieving climate targets.

If just half of the ETS2 revenues are used for energy renovations (or €30 billion/year), the investment gap could be reduced to €119 billion annually after 2026. If every €1 of government subsidy was able to leverage €3 in private finance, the gap could be reduced to just €29 billion annually.

5.4 Progressive distribution by country

The ETS2 carbon price will be a single price across the EU, despite wide differences in income levels in EU countries. To address this, the Social Climate Fund will redistribute about a third of ETS2 revenues from high-income to low-income countries, based on factors including gross national income per capita, shares of the population at risk of poverty living in rural areas and the percentage of households at risk of poverty with arrears on their utility bills.

Figure 7. Per country expected revenues from ETS2, € billions, 2026-2032, carbon price of €60

Source: Bruegel based on Regulation 2023/955 and EEA.

6 Policy options, trade-offs and recommendations

Annual investments in renovating European buildings need to increase by around € 149 billion or 1 percent of EU GDP. The challenge for policymakers is to ensure that the additional annual €149 billion investment in building renovation happens, that it happens in a way that society deems fair and that it does not threaten fiscal stability.

This is particularly challenging when governments currently face borrowing costs at their highest level since 2008. The EU’s fiscal rules framework also restricts the ability of countries with high debt (above 60 percent of GDP) to invest (Darvas et al 2024).

Traditionally, for supporting building renovation, European countries have relied on grants and tax incentives, soft loans and regulations (EIB, 2020; Bertoldi et al 2021). Four-fifths of 2021-2027 EU budget funding for energy efficiency and renovations comes in the form of grants (Ivanova et al 2023).

In the previous EU funding cycle (2014-2020) the European Scientific Advisory Board for Climate Change found that the cost-effectiveness of EU spending on energy efficiency in buildings was low because of inadequate targeting of investments through grants that crowded out private investment that would probably have happened anyway (Bredahl et al 2024).

The magnitude of the challenge means a wide range of policies should be employed to cut buildings-related emissions. A portfolio of measures will help mitigate the impact of policy trade-offs. For example, with zero-interest green loans, a trade-off exists between maximising cost-effectiveness and ensuring distributional fairness, because such loans are primarily taken up by richer households.

Maximising cost-effectiveness often involves targeting policies at wealthier households, which are more able to invest, while ensuring fairness would require focusing on poorer households25.

Another trade-off is simplicity versus complexity. Simple policies, such as bans on fossil-fuel boilers, are easy to understand and communicate but may fail to allocate resources efficiently and can create backlash. Policymakers must address such issues, especially when using ETS2 revenues, which should be allocated effectively and equitably.

Frontload investment support for the vulnerable to limit future compensation spending

For low-income countries, the Social Climate Fund (SCF) will likely suffice to both fully compensate vulnerable households26 for the carbon price and support investment in fuel-switching (Braungardt et al 2022).

However, if countries do not decarbonise at the pace they have committed to, and the carbon price is not contained, the capped SCF funding will not be enough to cover increased costs for vulnerable households in major countries including Germany, France and Italy (Braungardt et al 2022).

A fine balance must be struck between compensation measures and encouraging investment in decarbonisation solutions. If progress in energy renovations does not gain pace, the ETS2 price shock might be similar to that experienced during the energy crisis, during which €540 billion were earmarked to compensate consumers (Sgaravatti et al 2023).

This is equivalent to providing 35 million households with €15,000 each or covering more than half of our overall estimated investment gap for energy renovations up to 2030.

Governments should frontload investment support for vulnerable consumers to encourage energy renovations and reduce the need for compensation after ETS2 takes effect. Accelerating energy renovations in advance will help contain the ETS2 carbon price. Compensation measures must preserve the price-incentive to renovate. Typically, this involves using lump-sum transfers, rather than reducing consumer fossil-fuel prices.

Reduced energy demand also reduces the EU’s dependency on energy imports and improves resilience against economic shocks, which is critical given that 40 percent of the energy used for heating homes comes from natural gas (European Parliament, 2024), making the residential sector Europe’s biggest gas consumer.

The social benefits of targeted intervention

Untargeted and poorly designed policies can be fiscally unsustainable, lead to renovation works that would have happened anyway and provide little return on investment to the state. Financial support needs to be targeted by income level and building type.

The worst-performing buildings are prime candidates for grants and tax incentives because of their high energy and emissions-saving potential, offering a bigger return on investment compared to more energy-efficient buildings (European Commission, 2021). Renovating these buildings could significantly reduce the ETS2 carbon price. We estimated that deeply renovating 10 percent of the worst-performing buildings would cut total buildings-related emissions by 20 percent and lower ETS2 emissions by 8 percent27.

Targeting support at the least energy-efficient buildings addresses fairness considerations and is politically justifiable. Low-income households typically occupy these buildings and renovating them could reduce heating bills – which in Germany are up to 30 percent of the earnings of low-income households (Behr et al 2024).

Targeting these buildings would help alleviate energy poverty, which currently affects 50 million Europeans and leads to public health costs of €167 billion annually – from heating with smoky fuels, for example (Ahrendt et al 2016). Accelerating energy renovations could lift seven million Europeans out of energy poverty each year (ITRE, 2017), progressively reducing the need for public support to help vulnerable households with energy bills.

The EPBD’s broad definition of residential worst-performing buildings (43 percent of the building stock) allows for tailored policies suited for different local needs. For example, central and eastern European countries have large shares of multi-apartment blocks built from the 1960s to the 1980s.

While these buildings are energy-inefficient, in terms of energy per square meter, they perform better than energy-inefficient single-family houses because they have proportionally fewer outer walls and smaller unit sizes (Gerőházi et al 2023).

However, renovating communist-era panel buildings could be a more cost-efficient strategy than single-family houses because of their high population density and the potential for standardised, scalable renovation projects.

An important issue for the worst-performing and multi-apartment buildings is the impact on rental prices. Half of EU households below 60 percent of the median income are tenants, compared to only 30 percent overall. Landlords may put up rents after energy renovations, forcing vulnerable households to move and reducing the positive social impacts of energy renovations.

Therefore, controls on rental prices need to be attached to access to generous state subsidies. Similarly, to create incentives for energy renovation, the costs of the ETS2 carbon price might be shared between tenants and landlords. The higher the emissions per square meter, the greater the share of the costs that should be borne by landlords.

Change relative fuel prices and reduce price uncertainty

Only a third of the retail electricity price paid by households and small enterprises reflects actual electricity production costs. The rest is taxes, network costs and subsidies for renewables or nuclear plants.

As electrification is crucial to meet climate targets and can be considered an important societal goal, electricity taxes and subsidies could be shifted to the general tax burden, similar to education and public health funding.

Uncertainty around future fossil fuel and electricity prices also complicates the optimisation problem for investors. Governments have extensive experience designing tools to hedge against price volatility for renewable energy providers, such as contracts for difference.

Similar schemes could be implemented for deep energy renovations, involving energy utilities or new competitors as aggregators. Governments or public development banks could hedge future energy price risks by guaranteeing fixed payments to households based on defined electricity, fossil fuel and carbon prices (McWilliams and Zachmann, 2021). If fossil fuel or carbon prices are lower than expected (reducing the savings for investing households), governments would provide an annual payment. If not, nothing would happen.

Little progress has been made in phasing out fossil-fuel subsidies in the EU. The current policy framework, including the more than two-decades-old Energy Taxation Directive (2003/96/EC) and EU state aid regulations, permits subsidies for fossil gas and oil.

Between 2015 and 2021, fossil-fuel subsidies remained stable at around €50 billion per year, but in 2022, they more than doubled to €120 billion as governments shielded consumers from the energy crisis. Only eight EU countries28 have set dates for phasing out subsidies for fossil-fuel heating in buildings, or have restrictions on installing new fossil fuel-based heating systems.

Fossil-fuel subsidies distort competition, hinder the energy transition and can lead to long-term emission lock-ins. As energy commodity prices have fallen, governments should shift subsidies from fossil fuels to clean technologies and electricity.

It is critical to phase out these subsidies before 2027 when ETS2 takes effect, impacting final consumers and making the phase-out politically challenging.

Leverage future energy savings

The benefits of energy renovation investments are accrued over decades through lower energy bills and increased property values. We calculate that meeting the EPBD targets would imply annual savings of €81 billion by 2030 (Table 2). In other words, more than half of the investment gap can be met through direct economic returns.

Table 2. Annual investment gap to achieve the 2030 targets and potential energy savings, € billions per year

Note: See the online annex for a detailed explanation.

Source: Bruegel based Eurostat.

Households and small enterprises heavily discount the future and are typically risk averse. They face a disincentive to invest because of the heavy dependence of the returns on renovation investment on uncertain future energy and carbon prices. Governments can create certainty around future pay-offs and possibly bring them forward in time29.

Pay-as-you-save (or on-bill finance) schemes involve repaying energy-efficiency investments through the utility bill. Households could repay renovation expenses over time, limiting or removing completely the need for upfront capital (Bertoldi et al 2021a).

Another idea is energy-performance contracts, via which companies guarantee clients (households or firms) a certain level of energy savings. Payments are linked to actual energy savings achieved, and the company compensates the client for any shortfall (Bertoldi et al 2021a).

These contracts often involve a mix of funding sources, including revolving funds from the energy service company, the client, local and national subsidies and third parties. These types of contracts have already been used across Europe for large industrial sites, public administration buildings, large multifamily apartment buildings and social housing (Bertoldi et al 2021a).

Public funding to scale up energy-performance contracts can reduce the need for upfront capital, reduce borrowing costs and link renovations to actual energy-efficiency gains.

Policies such as these can alleviate consumer concerns about future energy savings and provide visibility around the expected cash flow from renovations, offering more investment certainty. Pay-as-you-save financing and energy performance contracts have emerged in recent years in Europe but so far have been too limited in scope and available funding.

Governments need to involve banks, utilities and local authorities in tackling this financing challenge, as only public-private partnerships can deliver the desired results.

Provide access to cheap money: the role of banks

EU governments should shoulder most of the energy-renovation costs for vulnerable consumers. However, to meet the EPBD targets, most consumers will have to pay for their own energy renovations.

Energy-performance obligations will therefore be essential, while governments can offer subsidised mortgages, collaborating with banks to create attractive, long-lasting financial products accessible to a wide range of beneficiaries. These loans must cater to various risk profiles and offer low interest rates.

Banks will only participate in such schemes if they provide guarantees and are financially appealing. The market value of properties themselves could be one main source of collateral. EU residential buildings, of which 71 percent are occupant-owned and most (58 percent) have no outstanding mortgage, are worth around €20 trillion (Sweatman and Yrivarren, 2023).

For high-risk profiles, governments or public development banks need to provide additional guarantees, ensuring the state will cover non-performing loans. This is vital for those with existing mortgages and the elderly, who may struggle to secure long-term loans.

The second pillar of an effective financial product would be a zero-interest rate. Repaying the debt-servicing costs of an investment is generally cheaper than directly covering the investment principal. Countries could design mechanisms that socialise the debt-servicing costs generally paid by clients.

Assuming interest rates fall in the coming years, covering only the financing costs of the €1,041 billion investment gap through the years could require €14 billion annually between 2024 and 2040, or 23 percent of the investment principal30.

The French zero-interest loan programme (Box 1), which mobilised ten times the initial public investment, demonstrated the effectiveness of such schemes in incentivising middle-income uptake while reducing public financial strain.

Public development banks, such as KfW in Germany, can provide preferential loans and act as intermediaries between governments and retail banks. KfW already offers households preferential interest rates, flexible repayment terms and up to 40 percent debt relief based on energy-efficiency gains. Investment in construction and energy renovations has surpassed KfW’s commitments threefold (Macfarlane and Mazzucato, 2023).

This scheme has proved to be budget-positive, as value-added tax revenues have exceeded the government’s allocation for the KfW programme (Macfarlane and Mazzucato, 2023). Both schemes were rolled out on a multiannual basis, which was also beneficial to increase awareness among citizens and provide positive feedback effects.

At the EU level, the European Investment Bank’s ELENA facility launched in 2009 provides technical assistance for buildings energy-efficiency investments. However, with less than €300 million awarded, mobilising an estimated €9.5 billion over 15 years, the impact has been limited31.

Other policy options are energy-efficiency obligations and mortgage portfolio standards. These are more stringent types of regulation that force the market to move towards improved energy performance. Energy-efficiency obligations target utility companies, forcing them to promote energy efficiency savings to their consumers.

Mortgage portfolio standards require lenders and financial funds to gradually increase the energy performance of their real-estate portfolios (Bertoldi et al 2021). The EPBD rightly encourages greater use of mortgage portfolio standards at national level.

One-stop shops to simplify energy renovations and collect data

One-stop shops (OSS) are private or public entities that act as points of reference for companies and citizens willing to make energy-efficiency investments. OSS serve as intermediaries between final customers and the entire supply chain for energy renovations, providing administrative, financial and legal support, while monitoring renovation progress and delivery.

OSS can also help pool projects, creating an investment case for contractors that would be lacking for projects in isolation32 (Bertoldi et al 2021b). This function of matching demand and supply can be particularly useful to create public-private partnerships.

OSS can also help fill data gaps by collecting information on prices, types of renovations and efficiency gains post-renovation. For example, OSS could help expand the adoption and improve the quality of energy-performance certificates (EPCs), the main tool at EU level to certify a building’s energy efficiency rating, grading building from A (best performing) to G (worst performing).

While useful, EPCs have been criticised for inaccuracy, often because of self-reporting and unreliable energy audits (European Commission, 2021). EPCs often provide ratings based on the physical assets of buildings or real energy consumption but fail to give an actual representation of energy performance in kilowatt hours per square metre (Jenkins et al, 2017). As a result, EPCs sometimes fail to inform households about the energy efficiency of their homes, leading many to mistakenly believe renovations are unnecessary (Römer and Salzgeber, 2023).

More broadly, the lack of useful data on buildings is alarming and should be addressed as a priority33. Detailed information on heating systems across local communities can help local authorities make informed decisions on which heating systems to promote and whether district heating is a viable option.

7 Conclusions

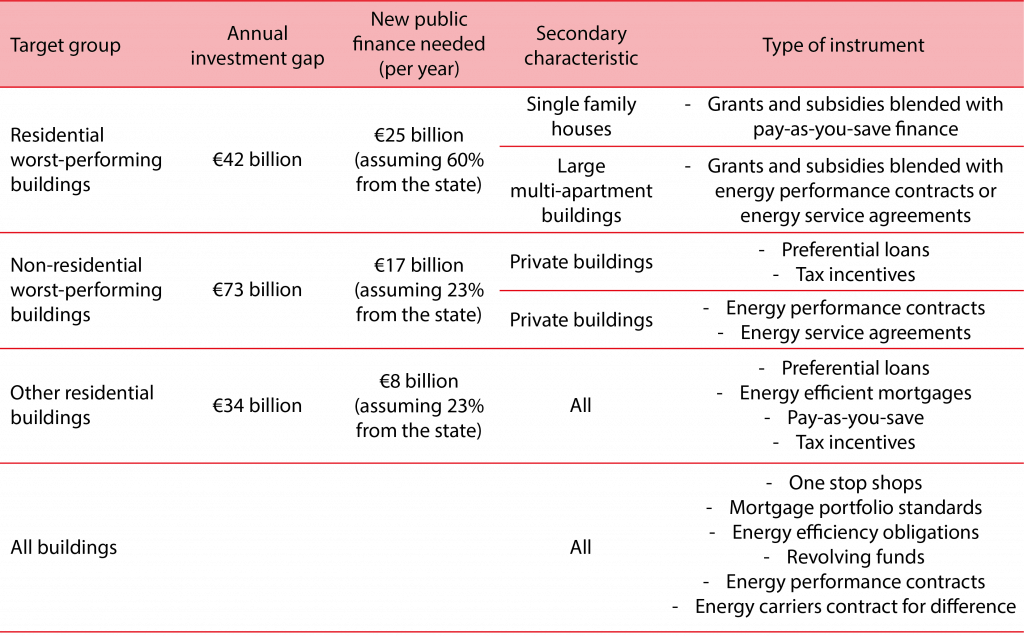

Bridging the investment gap in buildings energy renovations in the EU to meet the 2030 EPBD target requires national governments to roll-out cost-effective policy tools, shielding vulnerable consumers from the high upfront costs, leveraging future energy savings, lowering administrative burdens, correcting relative energy prices and crowding-in private capital.

Even for the worst-performing buildings, for which governments will need to allocate the biggest share of public support (estimated at 60 percent), leveraging future energy savings can close the remaining investment gap. This can be done by blending subsidies with pay-as-you-save or energy-performance contracts.

For other private buildings, preferential loans, tax incentives and energy-efficient mortgages can be used. Doing this would lower the new public finance needed to €50 billion per year (Table 3). Finally, deploying one-stop-shops, mortgage portfolio standards, energy efficiency obligations, revolving funds and contracts for difference have the potential to greatly speed up energy renovations.

Table 3. estimated investment gap and suggested relevant instruments by type of building

Source: Bruegel.

However, even if public funds and ETS2 revenues – estimated at €30 billion/year for energy renovations – are deployed most efficiently, a gap of €20 billion per year persists. EU institutions should therefore leave enough margin for fiscal manoeuvre for EU countries to make the required investments.

Endnotes

1. Or 10 metric tonnes of carbon dioxide (MtCO2) equivalent annually. Tis estimate includes emissions from residential, commercial and institutional buildings and excludes agricultural, forestry and fishing-related buildings.

2. This is to be consistent with reductions of emissions from buildings by 2030 of 60 percent compared to a 2015 baseline (European Commission, 2020). Note that buildings emissions reductions will need to exceed the overall EU target for sectors not covered by emissions trading to compensate for the limited expected progress in agriculture (-37 percent compared to 2015) and in transport (-16 percent compared to 2015).

3. In the same period, total renovation rates in the EU, including non-energy efficiency enhancing renovation, were about 12 percent per year (10 percent for non-residential buildings).

4. In 2022, household final energy demand (excluding commercial and public buildings) totalled 2,806 terawatt hours, of which fossil fuels accounted for 1,238 TWh and primary solid biofuels for 400 TWh. If both fossil-fuel and firewood heating were replaced by heat pumps, this would result in approximately 400 TWh of additional electricity demand (accounting for the thermal efficiency of different fuels), or 36 percent of the total load electricity generated in the EU in winter 2022-2023 (1,100 TWh).

5. The EU Building Stock Observatory dataset and studies such as Calipel et al (2024).

6. See European Heat Pump Association press release of 27 February 2024, ‘Market data’.

7. Ibid.

8. A major obstacle for policymakers is the lack of data. Heat-pump installation statistics come from the European Heat Pump Association, which does not cover all EU countries. Clear data on the number of boilers installed is hard to come by and not available over time. We cite one-of estimates from Carlsson et al (2023).

9. One immediate economic benefit of a major renovation is the increase in the property value, generally worth between 5 percent a 10 percent of the original value and reflecting the expected energy savings (Mahlstein et al 2022).

10. Until 2014, the European Commission used a fixed discount rate of 17.5 percent for all technology choices made by a representative household (Faure et al 2016). This was the lowered to 12 percent to 14.75 percent in 2016 and then to the current 10 percent. A discount rate of 10 percent means that €1,000 received 20 years from now is worth only €150 today. Interest groups consider the 10 percent discount rate still too high and recommend a rate between 3 percent and 6 percent (ECEEE, 2018).

11. Involving both thermal insulation and fuel switching.

12. The carbon price on heating in Germany at time of writing is lower and is expected to rise to €55 by 2025. It will be replaced by the ETS2 as of 2027.

13. Tis ignores the impact of other barriers by assuming zero borrowing constraints, no split incentives between renters and tenants and perfect information on the impact of renovation, and it does not account for the administrative non-monetary burden.

14. Heat pump energy efficiency changes depending on the buildings insulation level, the heating system design and the type of climate.

15. Crispian Balmer and Giuseppe Fonte, ‘Explainer: Why Italy’s Superbonus blew a hole in state accounts’, Reuters, 9 April 2024.

16. Guy Chazan, ‘Outraged and furious’: Germans rebel against gas boiler ban’, Financial Times, 26 May 2023.

17. Laura Pitel, ‘Germany passes watered-down ‘boiler ban’ law after months of infighting’, Financial Times, 8 September 2024.

18. See BPIE, ‘Attracting investment in building renovation’, September 2017.

19. Emissions linked to electricity use in buildings and heat supply via district heating are already covered by the first EU ETS.

20. See European Commission website.

21. The price of €60 was calculated by indexing the 2020 price of €45 to inflation, assuming inflation of 3 percent in 2024 and 2 percent thereafter.

22. Estimating the investment gap is challenging due to fragmented, outdated and poor-quality data. Our estimate aligns with the European Commission’s one of €152 billion per year in the EBPD impact assessment (European Commission, 2021) and I4CE’s €112 billion per year (Bizien, 2024), though it is more conservative than the BPIE’s estimate of €200 billion per year for the EU Renovation Wave (Dravecký et al 2021). Our estimate excludes costs for upgrading electricity infrastructure for peak winter demand and potential cost savings from expanding district heating in urban centres.

23. This is likely to be an overly generous assumption, as EU countries will use ETS2 revenues to compensate households and smaller companies for the price increase. However, ETS revenues are also rising and can be dedicated to energy renovations, giving us confidence that our estimate is not too generous.

24. See European Parliament press release of 20 April 2024, ‘Social Climate Fund’.

25. An example is the introduction of feed-in tariffs for solar photovoltaic panels by European governments, such as the UK, in the early 2010s. Feed-in tariffs were designed to guarantee a fixed payment to households in the future for the energy generated by an upfront investment. Policies were successful at crowding-in private investment immediately. However, a focus on future benefits rather than upfront subsidies excluded all those who could not afford the immediate installation costs (of about €20,000).

26. Defined as households at risk of poverty and social exclusion.

27. Equivalent to 81 MtCO2 and 554 TWh of energy savings; see the online annex.

28. Austria, Belgium, Denmark, Finland, Germany, Ireland, Netherlands, Slovenia.

29. For example, the cash flows generated by energy savings and the increased value of renovated homes can be used as collateral for loans (Bertoldi et al 2021a).

30. This is assuming the cost of borrowing for households for house purchase as the default interest rate, which in March 2024 was 3.8 percent for the euro area. The interest rate is expected to drop to 3 percent in 2025, and then fall to the European Central Bank target of 2 percent.

31. See the ELENA webpage.

32. For example, unlocking the use of energy performance contracts, generally deployed for large dwellings, also for single-family houses.

33. This might be delivered as part of a wider European Energy Agency initiative. See Simone Tagliapietra, Georg Zachmann, Anna Creti, Ottmar Edenhofer, Natalia Fabra, Jean-Michel Glachant … László Szabó, ‘Green transition: create a European energy agency’, First Glance, 26 April 2023, Bruegel.

References

Abdoos M, A Alireza, A Shahee and R Zahedi (2024) ‘Reducing the energy consumption of buildings by implementing insulation scenarios and using renewable energies’, Energy Informatics 7(18).

Ahrendt D, H Dubois, V Ezratty, T Fox, JM Jungblut, A Pittini … J Vandamme (2016) Inadequate housing in Europe: Costs and consequences, Eurofound.

Alpino, M, L Citino and F Zeni (2023) ‘Costs and benefits of the green transition envisaged in the Italian NRRP. An evaluation using the social cost of carbon’, Occasional Papers 720, Bank of Italy.

Andersen, KS, R McKenna, S Petrovic and C Wiese (2020) ‘Exploring the role of households’ hurdle rates and demand elasticities in meeting Danish energy-savings target’, Energy Policy, 146: 111785.

Arcano, R, A Capacci and G Galli (2024) ‘Post mortem per il Superbonus: extra defcit, extra debito e rallentamento in atto nel settore delle costruzioni’, Osservatorio CPI, 21 March, Università Cattolica del Sacro Cuore.

Baccianti, C (2023) EU Climate Funding Tracker, Agora Energiewende, 20 June.

Behr VSM, M Kücük, M Longmuir and K Neuhof (2024) ‘Sanierung sehr inefzienter Gebäude sichert hohe Heizkostenrisiken ab’, DIW Wochenbericht 19/2024, DIW Berlin.

Bertoldi, P, B Boza-Kiss, M Economidou, V Palermo and V Todeschi (2021a) ‘How to finance energy renovation of residential buildings: Review of current and emerging financing instruments in the EU’, WIREs Energy and Environment 10(1).

Bertoldi P, B Boza-Kiss, N Della Valle and M Economidou (2021b) One-Stop Shops for Residential Building Energy Renovation in the EU: Analysis & Policy Recommendations, JRC Science for Policy Report, European Commission.

Biere-Arenas, R, C Marmolejo-Duarte, S Spairani-Berrio and Y Spairani-Berrio (2021) ‘One-Stop-Shops for Energy Renovation of Dwellings in Europe—Approach to the Factors That Determine Success and Future Lines of Action’, Sustainability, 13(22): 12729.

Bizien A, C Calipel and T Pellerin-Carlin (2024) European Climate Investment Deficit Report: An Investment Pathway for Europe’s Future, Institute for Climate Economics.

Branner H, I Haase, A Reyneri and EK Velten (2022) The Use of Auctioning Revenues from the EU ETS for Climate Action, Ecologic Institute.

Braungardt S, V Bürger, J Rosenow and B Tezak (2023) ‘Banning boilers: An analysis of existing regulations to phase out fossil fuel heating in the EU,’ Renewable and Sustainable Energy Reviews, 183: 113442.

Braungardt, S, K Hünecke, Z Philipps, D Ritter and K Schumacher (2022) The Social Climate Fund – Opportunities and Challenges for the Buildings Sector, Oko-Institute.

Bredahl Jacobsen J, C Cartalis, S Dessai, L Diaz Anadon, O Edenhofer, V Eory … M Van Aalst (2024) Towards EU climate neutrality: Progress, policy gaps and opportunities, European Scientific Advisory Board on Climate Change.

Brugger, H, E Popovski and M Ragwitz (2023) ‘Decarbonization of district heating and deep retrofit of buildings as competing or synergetic strategies for the implementation of the efficiency first principle’, Smart Energy 10: 100096.

Carlsson, J, A Gasparella, D Koolen, S Letout, JC Roca Reina, A Toleikyte … J Volt (2023) The Heat Pump Wave: Opportunities and Challenges, JRC Science for Policy Report, European Commission.

Ciminelli, G and C Schwellnus (2024) ‘Achieving the energy and climate transition’, in OECD Economic Surveys: Italy 2024, Organisation for Economic Co-operation and Development.

Cludius J, A Eden, I Holovko, K Schumacher, N Unger and N Victoria (2023) Putting the ETS 2 and Social Climate Fund to Work: Impacts, Considerations, and Opportunities for European Member States, Adelphi, Oko Institut, Center for the Study of Democracy, WiseEuropa.

Darvas, Z, L Welslau and J Zettelmeyer (2024) ‘Incorporating the impact of social investments and reforms in the EU’s new fiscal framework’, Working Paper 07/2024, Bruegel.

Dastgerdi M, I Eryzhenskiy, LG Giraudet and M Segú (2022) Zero-Interest Green Loans and Home Energy Retrofits: Evidence from France, Centre international de recherche sur l’environnement et le développement.

Dempster H, S Huckstep (2024) Meeting Skill Needs for the Global Green Transition, Center for Global Development.

Dravecký, L, M Fabbri, X Fernández Álvarez, I Jankovic … H Sibileau (2021) Deep Renovation: Shifting from Exception to Standard Practice in EU Policy, Buildings Performance Institute Europe.

ECEEE (2018) Discount rates crucial in energy modelling, European Council for an Energy Efficient Economy.

EEA (2023a) ‘Greenhouse gas emissions from energy use in buildings in Europe’, 24 October, European Environment Agency.

EEA (2023b) ‘Fossil Fuel Subsidies’, 17 November, European Environment Agency.

EIB (2020) The Potential for Investment in Energy Efficiency through Financial Instruments in the European Union, European Investment Bank.

Eichhammer, W, T Mandel, L Kranzl, A Müller, E Popovski and F Sensfuß (2023) ‘Investigating pathways to a net-zero emissions building sector in the European Union: what role for the energy efficiency first principle?’ Energy Efficiency 16(22).

ENEA (2024) Super Ecobonus 110%, Agenzia nazionale per le nuove tecnologie, l’energia e lo sviluppo economico sostenibile and Ministero dell’ambiente e della sicurezza energetica.

European Commission (2019) Comprehensive study of building energy renovation activities and the uptake of nearly zero-energy buildings in the EU: final report, Directorate-General for Energy, Ipsos and Navigant.

European Commission (2020a) ‘A Renovation Wave for Europe – Greening Our Buildings, Creating Jobs, Improving Lives’, SWD (2020) 550 final.

European Commission (2020b) ‘Impact Assessment, Stepping up Europe’s 2030 Climate Ambition, Investing in a Climate-Neutral Future for the Beneft of Our People’, SWD (2020) 176 final.

European Commission (2021) ‘Impact Assessment Report Accompanying the Proposal for a Directive of the European Parliament and of the Council on the Energy Performance of Buildings (Recast)’, SWD (2021) 453 final.

European Commission (2021b) Lessons Learned to Inform Integrated Approaches for the Renovation and Modernisation of the Built Environment – Final Report, Directorate General for Energy.

European Commission (2021c) Overview of District Heating and Cooling Markets and Regulatory Frameworks under the Revised Renewable Energy Directive – Annexes 6 and 7 – Final version, Directorate General for Energy.

European Commission (2023b) ‘2023 Report on Energy Subsidies in the EU’, COM (2023) 651 final European Commission (2024) ‘Securing our future’, SWD (2024), 63 final.

Faure C, X Gassmann, T Meissner and J Schleich (2016) ‘Making the implicit explicit: A look inside the implicit discount rate’, Energy Policy, 97: 321–331.

Fotiou T, K Govorukha, Günther, C, M Pahle and S Osorio (2024) ‘Carbon prices on the rise? Shedding light on the emerging EU ETS2’, mimeo.

Gerarden, TD, RG Newell and RN Stavins (2017) ‘Assessing the Energy-Efciency Gap’, Journal of Economic Literature 55(4): 1486–1525.

Gerőházi, É, E Somogyi and H Szemző (2023) Community Tailored Actions for Energy Poverty Mitigation (Deliverable 1.3), ComAct Project, Metropolitan Research.

ITRE (2017) Energy Poverty, Study for the ITRE Committee, European Parliament.

Ivanova V, M Jones, A Joyce, A Psatha and C Simpson (2023) 2021-2027 Cohesion Policy Support for Energy Efficiency and Building Renovation, E3G and Renovate Europe.

Jenkins, D, A Peacock and S Simpson (2017) ‘Investigating the consistency and quality of EPC ratings and assessments’, Energy 138: 480–89.

Jiménez-Navarro JP, K Kavvadias and G Tomassen (2019) Decarbonising the EU Heating Sector, JRC Technical Reports, European Commission.

Macfarlane, L and M Mazzucato (2023) ‘Mission-Oriented Development Banks: The Case of KfW and BNDES’, Working Paper 2023/13, UCL Institute for Innovation and Public Purpose.

Mahlstein, K, C McDaniel, S Schropp and M Tsigas (2022) ‘Estimating the economic effects of sanctions on Russia: An Allied trade embargo’, The World Economy, 45(11): 3344–83.

McWilliams, B, S Tagliapietra and C Trasi (2024) ‘European clean tech tracker’, Bruegel dataset, first published 28 March 2021.

McWilliams, B and G Zachmann (2021) ‘Commercialisation contracts: European support for low-carbon technology deployment’, Policy Contribution 15/2021, Bruegel.

Müller, S and L Nesselhauf (2023) Der CO2-Preis Für Gebäude Und Verkehr, Agora Energiewende.

Römer, D and J Salzgeber (2023) KfW Energy Transition Barometer 2023 Energy Transition Caught between Need for Action and Financial Possibilities, KfW.

Samwick, A (1997) ‘Discount Rate Heterogeneity and Social Security Reform’, Working Paper 6219, National Bureau of Economic Research.

Sgaravatti, G (2024) ‘Electricity tariffs dashboard’, Bruegel dataset, 16 May.

Sgaravatti, G, S Tagliapietra, C Trasi and G Zachmann (2023) ‘National Fiscal Policy Responses to the Energy Crisis’, Bruegel dataset, first published 4 November 2021.

Sweatman, P and M Yrivarren (2023) Engaging Retail Lenders in Home Renovation 2024, Climate Strategy.

UpB (2023) ‘Audizione della Presidente dell’Ufcio parlamentare di bilancio nell’ambito delle audizioni preliminari all’esame del Doc. LVII, n. 1 (Documento di economia e fnanza per il 2023)’, Ufcio Parlamentare di Bilancio.

WWF (2022) Where Did All the Money Go? How EU Member States Spent Their ETS Revenues – And Why Tighter Rules Are Needed, WWF European Policy Office.

The authors thank Atanasiu Bogdan, Rebecca Christie, Johanna Cludius, Sarah O’Brien, Clara Calipel, Stephen Gardner, Roaland Gladushenko, Conall Heusaff, Bertin Martens, Marion Santini, Louise Sunderland, Georg Zachmann for providing comments to an earlier version of this paper. They are also grateful to the participants in a February 2024 workshop held at Bruegel to discuss this issue. Financial support from the European Climate Foundation is gratefully acknowledged. This article is based on Bruegel Policy Brief Issue no12/24 | July 2024.