Climate risks and global value chains

Rikard Forslid is Professor of Economics at Stockholm University and Mark Sanctuary

Extreme weather events will become more frequent as global temperatures rise. This is a challenge for companies that depend on complex international supply chains. There is an academic literature that analyses the impact of natural disaster shocks at the firm level (eg. Barrot and Sauvagnat 2016, Boem et al 2019, Carvalho et al 2021, Todo et al 2015, Zhu et al 2016, Kashiwagi et al 2021).

These studies focus on the Great East Japan Earthquake or on natural disasters in the US and find significant domestic effects as well as spillovers between Japan and the US. For example, Boehm et al (2019) find that the Great East Japan Earthquake caused the output of subsidiaries of Japanese firms in the US to fall roughly one-for-one with the decline in imports.

In a recent study (Forslid and Sanctuary 2022), we provide evidence of the impact of extreme weather events on two small countries located far from one another in the impact of the catastrophic 2011 Thai flood on Swedish importing firms. Both Sweden and Thailand are small countries located far from one another.

A priori, it would seem that Thai imports could be easily substituted by imports from countries closer to Sweden. Instead, the evidence points to very large effects. Production falls by an average of 8% among the affected Swedish firms, and the multipliers are very large, with a fall in production almost 30 times larger than the fall in imports.

The Thai flood of 2011 began in July of that year and inundated 9.1% of the total land area of the country, affecting close to 13 million people, with 728 deaths. Damages were estimated at $46.5 billion, dispersed across 69 provinces in every region of the country, and Bangkok and its vicinity were paralysed for two months (Poapongsakorn and Meethom 2013).

The flood hit the manufacturing sector especially hard. METI (2012) report, for instance, production losses of 84% in transport machinery, 77% in office equipment, and 73% in information and communication equipment. The time to recover differed between sectors, but also among individual firms depending on their location.

In the automotive industry Toyota required 42 days to partly resume operations, while Honda required 174 days. Thailand produced approximately 43% of the world’s hard disk drives in 2011, and recovery was somewhat slower than in the automobile sector. Many companies had facilities in Ayutthaya, where industrial parks were heavily inundated (Haraguchi and Lall 2015).

Overall, however, Thai industry recovered within months and had made important progress within six months. Production in March 2012 was 10% lower than that in March 2011, which may be compared to the maximal loss of 77% in November 2011 (METI 2012).

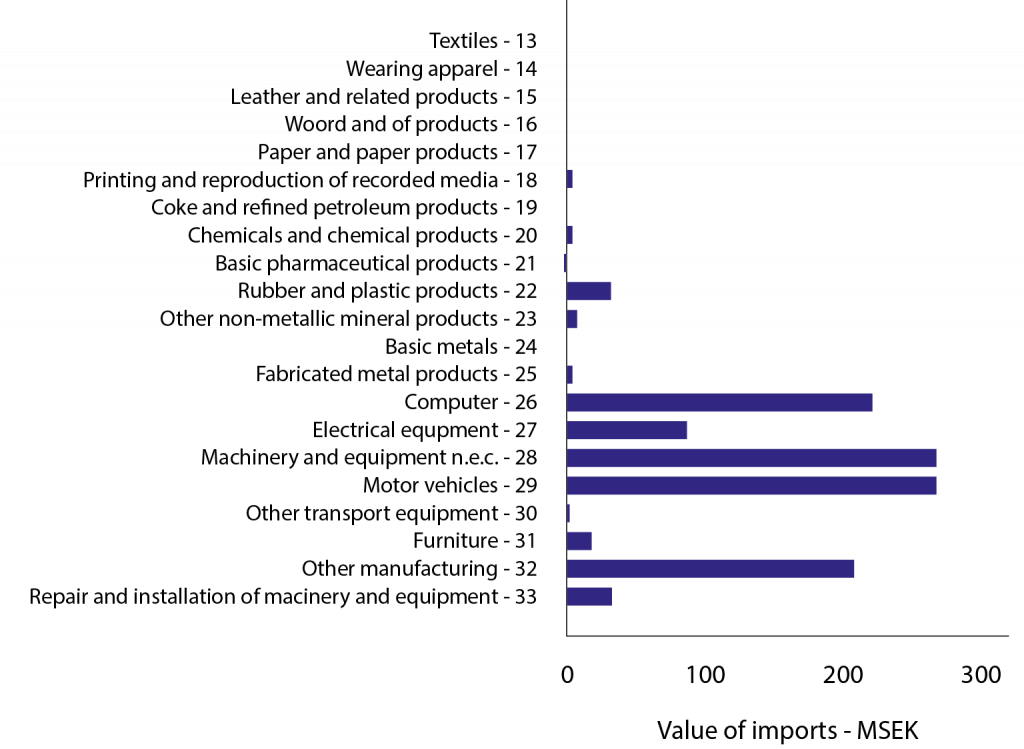

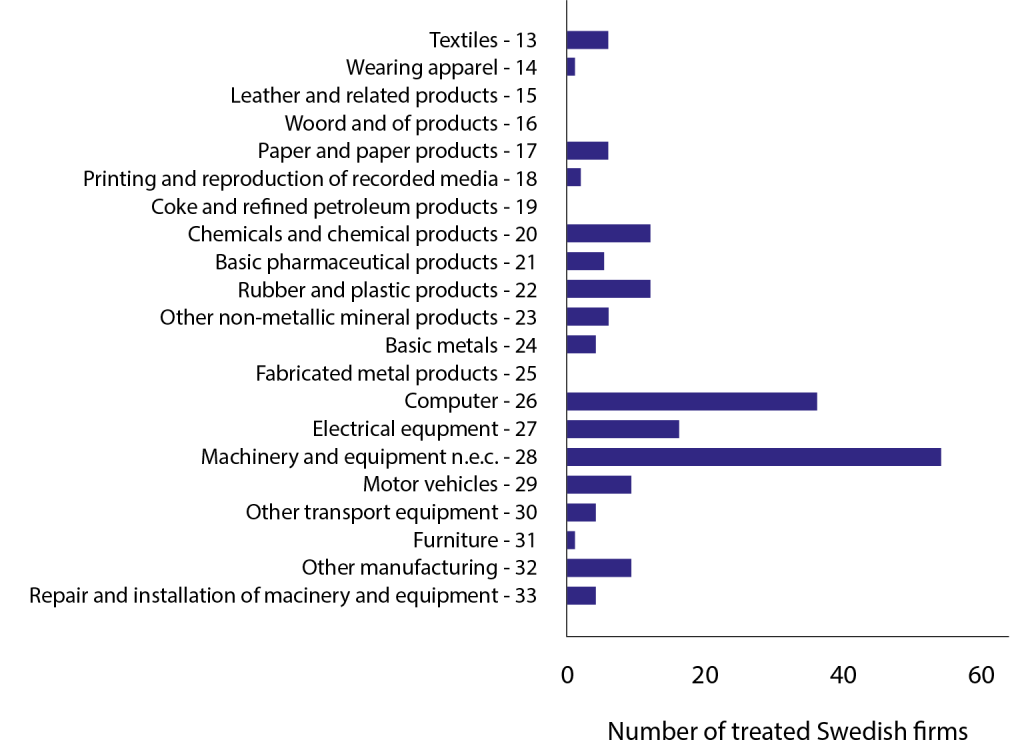

Swedish manufacturing imports from Thailand was concentrated in machinery and equipment (Sector 28) and computer and electronic products (sector 26) both in terms of value and number of importing business, shown in Figure 1.

The fact that Sweden is a small economy far away from Thailand seems to have aggravated the effects of the shock. Multipliers are much higher than in other studies on large countries

Figure 1. The pattern of Swedish imports from Thailand

Source: Statistics Sweden.

Estimating the impact of the flood on Swedish businesses requires careful study design. For our Thai flood study, we use firm-level data, including the products each business imports, and the countries from which these imports come from, over the period from 2006-2013.

Swedish businesses with an average of at least some (greater than zero) imports from Thailand in the two years prior to the flood (2009 and 2010) are assigned to the treated group, while all other Swedish firms that import during this period are assigned to the control group.

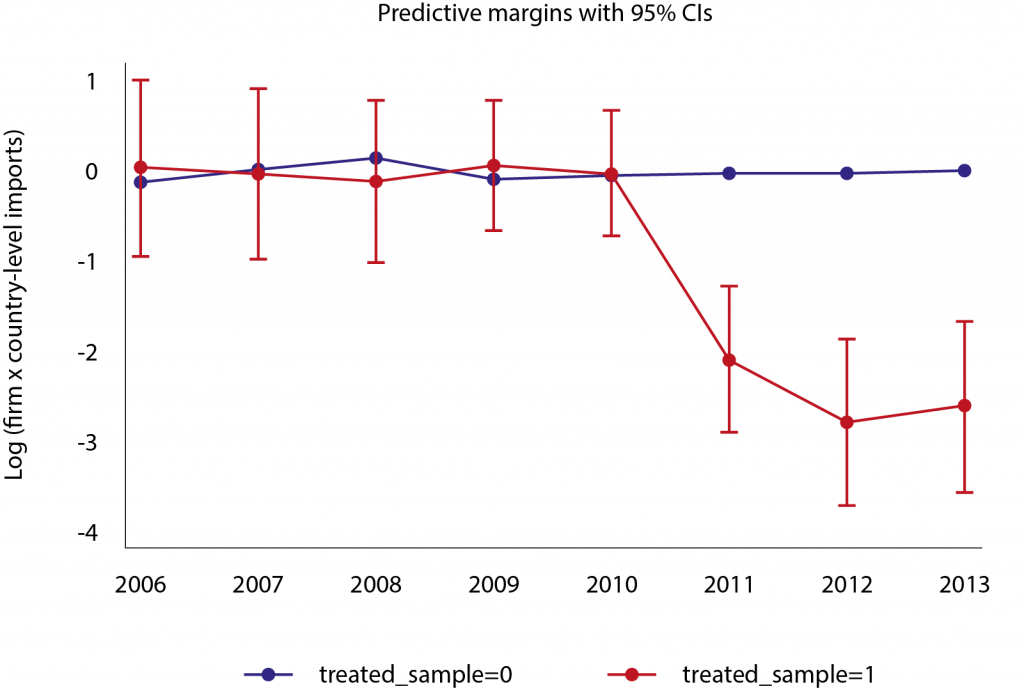

Figure 2 illustrates the divergence in imports between the treated and control groups of firms, the magnitude of the flood’s impact is clear. Thai imports by Swedish businesses fell by around 90%: Swedish imports from Thailand were around €100 million lower in 2012, the year following the flood.

Moreover, sales by exposed Swedish firms dropped 8% drop in 2012. This suggests the Thai flood caused a drop of about €3 billion in sales by Swedish business, a 30-fold amplification.

Figure 2. The impact of the 2011 Thai flood

Source: Forslid and Sanctuary (2022).

Interestingly, the adverse impacts to Swedish businesses persisted for two years through to 2013, even though Thai production had largely recovered within six months of the flood waters receding. This indicates that fixed costs in establishing links in supply networks may be substantial, and once severed, supplier-buyer relationships may be costly to re-establish (eg. Antras and Chor 2021).

Swedish importers predominantly switched to other Asian suppliers, and there is weak evidence of reshoring (where Swedish businesses sourced alternative inputs from EU countries). Larger businesses were better at handling the shock, facing a smaller drop in the value of imports from Thailand than smaller businesses.

Geographical diversification of suppliers is also important in determining how well Swedish businesses weathered the shock. Exposed businesses that import a product from more than one country are almost completely shielded from the disruptions caused by the flood; it was easier for these firms to substitute to similar inputs from non-Thai countries of origin.

In contrast, businesses that imported a product from Thailand only were unable to source alternative suppliers of the goods affected by the flood. There were also strong negative horizontal effects. Swedish businesses cancelled orders of goods that were complementary to the goods they were unable to obtain from Thailand – imports of other goods from other countries fell by around 80%.

Overall, these new insights suggest that firms were poorly prepared to manage the disruptions arising from the flood, even though some firms hedged their operations with multiple sources of critical inputs.

Moreover, imports from Thailand were slow to recover as Swedish businesses turned to other countries to meet their needs for critical inputs that Thailand had been unable to supply. The fact that Sweden is a small economy far away from Thailand seems to have aggravated the effects of the shock. Multipliers are much higher than in other studies on large countries.

Similarly, we find that small businesses are worse hit by the shock than large firms, possible due to weaker negotiating power. These microeconomic insights help clarify aggregate effects of foreign extreme weather events on the home economy.

While individual firms may suffer significant losses from events like the Thai flood (Xu and Monteiro 2022), and the aggregate effects were non-negligible, securing alternative sources for critical inputs can help support better economic resilience to extreme weather at home.

References

Antras, P and D Chor (2021), “Global value chains”, NBER Working Paper 28549.

Boehm, CE, A Flaaen and N Pandalai-Nayar (2019), “Input linkages and the transmission of shocks: Firm-level evidence from the 2011 Tohoku earthquake”, Review of Economics and Statistics 101(1): 60–75.

Carvalho, VM, M Nirei, YU Saito and A Tahbaz-Salehi (2021), “Supply chain disruptions: Evidence from the Great East Japan Earthquake”, The Quarterly Journal of Economics 136(2): 1255–1321.

Forslid, R and M Sanctuary (2022), “Climate Risks and Global Value Chains: The impact of the 2011 Thailand flood on Swedish firms”, CEPR Discussion Paper 17855.

Haraguchi, M and U Lall (2015), “Flood risks and impacts: A case study of thailand’s floods in 2011 and research questions for supply chain decision making”, International Journal of Disaster Risk Reduction 14: 256–272.

Kashiwagi, Y, Y Todo and P Matous (2021), “Propagation of economic shocks through global supply chains—evidence from Hurricane Sandy”, Review of International Economics 29(5): 1186–1220.

METI – Ministry of Economy Trade and Industry (2012), “White paper on international economy and trade 2012”.

Poapongsakorn, N and P Meethom (2013), “Impact of the 2011 floods, and flood management in Thailand, ERIA Discussion Paper 34:2013.

Todo, Y, K Nakajima and P Matous (2015), “How do supply chain networks affect the resilience of firms to natural disasters? Evidence from the Great East Japan Earthquake”, Journal of Regional Science 55(2): 209–229.

Xu, A and J-A Monteiro (2022), “International trade in the time of climate crisis”, VoxEU.org, 12 December.

Zhu, L, K Ito and E Tomiura (2016), “Global sourcing in the wake of disaster: Evidence from the Great East Japan Earthquake”, RIETI.

This article was originally published on VoxEU.org.