Lessons from the Germany shock: consequences of uncoordinated policies

Harald Fadinger is Professor of Economics at the University of Mannheim, Philipp Herkenhoff is a Postdoctoral Researcher at the Johannes Gutenberg University of Mainz, and Jan Schymik is an Economist at the University of Mannheim

As the world emerges from the COVID crisis, it is witnessing a resurgence of industrial policy in affluent countries, including the Inflation Reduction Act and the CHIPS Act in the US. These developments are putting pressure on EU members to also engage in industrial policy measures. This column evaluates the impact of Germany’s early-2000s labour market reforms on the broader euro area. The findings underscore the importance of coordinated EU-wide policies.

Industrial policy is experiencing an unprecedented comeback in affluent countries (Juhasz et al 2023). The US Inflation Reduction Act (IRA) bill alone consists of an estimated $780 billion subsidy package to clean-tech production and investment, largely through tax credits, while the subsidies under the CHIPS Act amount to $50 billion.

Using simulations based on a structural model of international trade, Attinasi et al (2023a, 2023b) indicate that the effect of the IRA on the EU is sizable, lowering EU output by between 0.5% and 3%, with varied sectoral impacts.

The EU also provides a substantial level of green subsidies already today. While the level of these subsidies is roughly similar in size to those granted by the US, the EU lacks a flagship green subsidy scheme; most green subsidies are given as part of a multitude of initiatives at the national or EU level (Kleimann et al 2023).

Moreover, the planned policy responses of EU member countries to the IRA are also highly heterogeneous. While some countries, such as Germany, have individually drafted large subsidy schemes, poorer EU countries or economies with less fiscal space have hardly responded to the IRA.

The German government has proposed an 80% electricity price subsidy for heavy industry (Industriestrompreis), which carries a €30 billion price tag. It has also drafted subsidy plans for clean production in heavy industry worth around €20 billion and €20 billion of subsidies have already been earmarked for chip production plants, of which €10 billion alone will go to Intel.

This disparity can threaten the EU’s internal competitiveness. Producers in the EU are not only competing with Chinese and US producers, but there is also harsh competition for the location of industrial activity between EU economies themselves. Consequently, uncoordinated industrial policy within the EU will likely also have negative consequences due to negative internal spillovers.

Industrial policy should be done mostly at the EU level instead of at national level to prevent fragmentations of the European Single Market

Lessons from the past: the transformation of the German economy from the ‘sick man’ of Europe

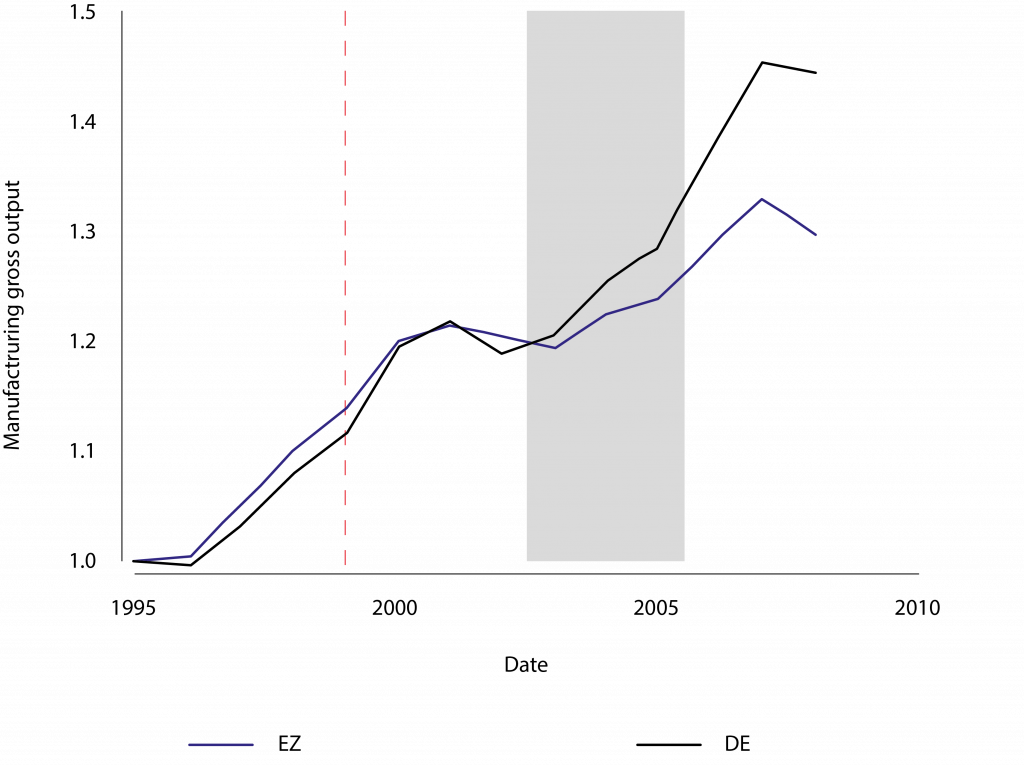

To quantitatively assess the potential impact of such unilateral policies within the EU, we reflect on the EU’s recent history. In a recent paper (Fadinger et al 2023), we evaluate the impact of Germany’s early-2000s labour market reforms on the broader euro area. In the aftermath of these reforms, German manufacturing surged while manufacturing in the rest of the euro area experienced a significant contraction.

In the 1990s, German firms increasingly embraced wage flexibility and distancing from collective wage agreements. Additionally, a series of major labour market and social insurance reforms were implemented from 2003 to 2005 (the Hartz reforms and others).

These reforms incentivised labour force participation, for example via an increase in the pension age and stricter eligibility requirements for access to disability benefits, while curbing the generosity of unemployment insurance.

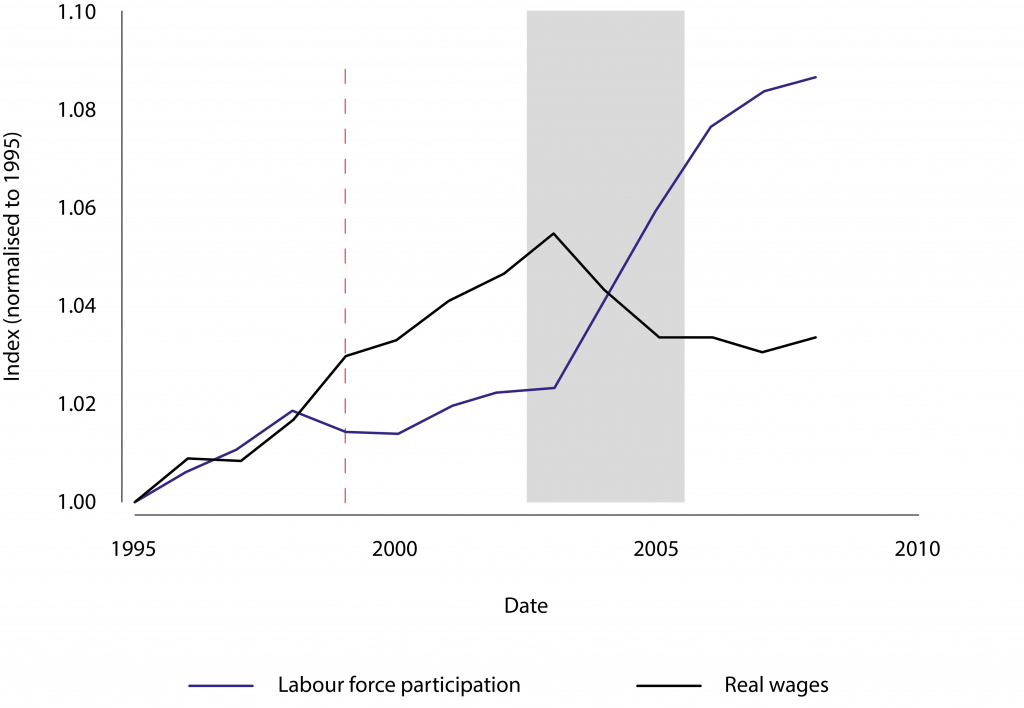

Following the implementation of the reforms, labour force participation increased strongly in Germany while nominal wages stagnated. These developments were reflected in a real depreciation of German goods relative to those of other euro area economies, implying a large gain in German manufacturing competitiveness within the euro area.

Figure 1. Labour force participation and real labour costs in Germany

Notes: The figure plots indices of labour-force participation and real labour costs in Germany. Index values are relative to the base year 1995. Labour-force participation is based on OECD data for working ages 20-64 years and real wages are deflated labour compensation per employment, using EU KLEMS data.

Figure 2. Manufacturing output in the euro area

Notes: The figure plots indices of real gross output in manufacturing in Germany and the rest of the EZ. Index values are relative to the base year 1995, using EU KLEMS data.

Drawing from approaches by Autor et al (2013) and Acemoglu et al (2016), we examine the impact of intensified trade competition from Germany on euro area employment and wages. Sectors more exposed to German competition faced significant employment declines, especially after the introduction of the euro, with nominal wages remaining largely unresponsive.

On average, increased German competition led to an estimated 6% dip in manufacturing employment in the rest of the euro area.

We then quantify the consequences of this German shock in general equilibrium, using a quantitative New Keynesian multisector model of international trade that builds on the work of Rodríguez-Clare et al (2020).

It features multiple sectors and an input-output structure akin to Caliendo and Parro (2015) and additionally incorporates downward nominal wage rigidities (DNWRs) à la Schmitt-Grohé and Uribe (2016). These rigidities lead to sluggish downward adjustment of wages over time, resulting in temporary involuntary unemployment.

We extend that model in three aspects that are relevant to our research question. First, we allow for time variation in the utility value of staying out of the labour force, since German structural reforms increased incentives to actively participate in the labour market.

Second, we introduce unemployment benefits to account for variation in unemployment insurance replacement rates.

Finally, we introduce a savings decision and international trade in bonds to generate an endogenous adjustment of countries’ current accounts, as the same period was marked by a growing German current account surplus.

With the help of our structural model, we can back out the nature of the Germany shock caused by the reforms. First, we estimate nominal wage rigidities for euro area economies and find significantly smaller DNWRs for Germany compared to all other euro area countries.

Second, we back out shocks to the utility from not participating in the labour market based on variation in labour force participation and expected real wages. Following the reforms, German workers experienced a 25% reduction in the utility value of staying out of the labour force, while the rest of the euro area experienced no such shock.

Third, we directly feed in data on replacement rates to assess the role of less generous unemployment insurance. Time series of replacement rates show a strong reduction in the replacement rate for Germany starting with the Hartz reforms in 2003.

We also assess the role of the German savings glut through the lens of our model. Around the introduction of the euro, German investors put a greater weight on current consumption compared to consumption in future periods, which led to increases in international saving over time.

Together with investors’ desire to smooth the temporary positive income shock caused by increased labour supply, this contributed to the large increase in the German current account surplus.

Lastly, we find that productivity and trade costs in Germany evolved similarly to those of other euro area economies, and thus cannot explain the German export boom.

Our model suggests that the German competitiveness shock, combined with the fixed-exchange regime, essentially reallocated unemployment from Germany to other euro area members. Economies with a similar industrial structure were most exposed the German competitiveness shock, as these economies experienced a greater contraction of their export demand.

In the euro area’s fixed-exchange regime, immediate wage adjustments were stifled, causing short-term involuntary unemployment that only subsequently died out over time.

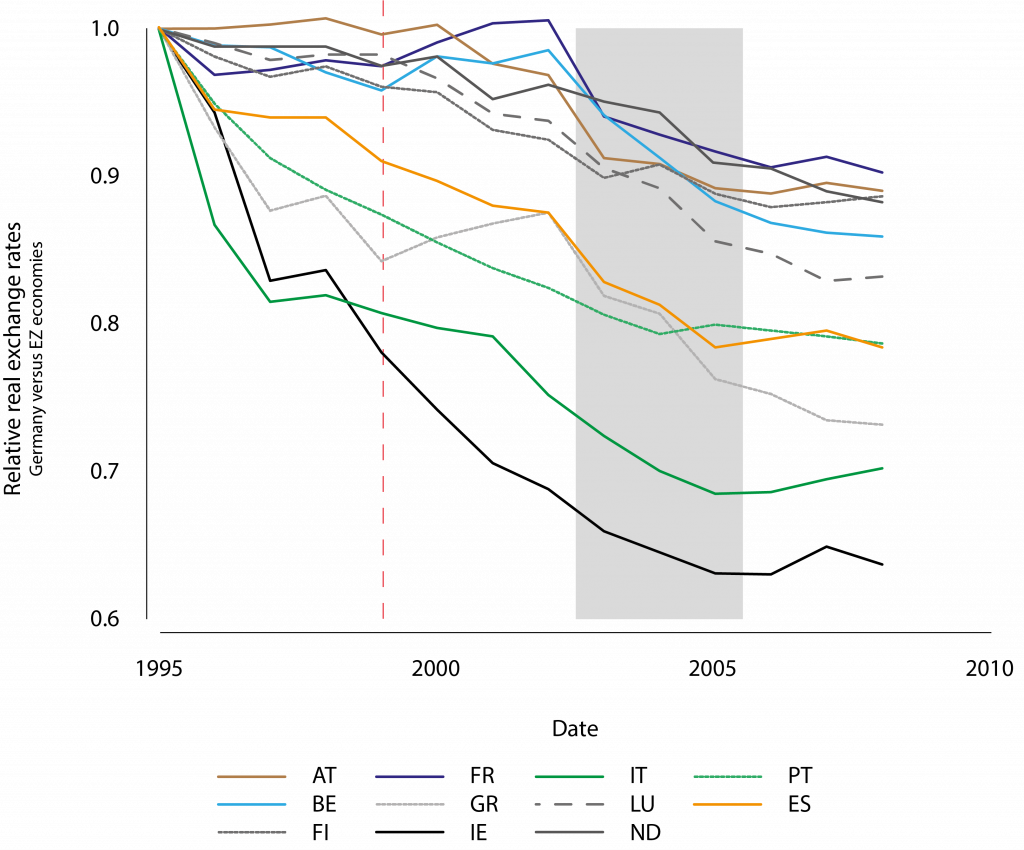

Figure 3. Real exchange rate fluctuations in the euro area

Notes: The figure plots indices of real exchange rates for EZ economies relative to the German real exchange rate. Relative real exchange rates are defined as the German expenditure-based price level of GDP in purchasing power parities relative to the price level of respective EZ economy using data from the Penn World Tables 8.0. Decreases in the relative real exchange rate imply a relative loss in trade competitiveness of the respective EZ economy.

Using our structural model, we can evaluate alternative policies to deal with the unilateral German competitiveness shock. In the absence of nominal wage rigidities, wages may have declined to clear labour markets and thus prevented involuntary unemployment.

Alternatively, we consider the impact of coordinated labour market reforms. Structural divergences between euro area member states can contribute to nominal and real divergences and prevent euro area convergence (Eriksgård Melander et al 2019). We study a counterfactual where all euro area member economies conduct reforms identical to those implemented by Germany.

This counterfactual results in lower unemployment and a large increase in labour force participation, employment, and output across euro area economies, highlighting the importance of coordinated labour market policies within the currency area.

Furthermore, we find that a higher average inflation might have offset the adverse effects of the German shock for the rest of the euro area.

Key take-aways from the Germany shock for today

How can we relate these findings to the current drive for large, but largely uncoordinated, industrial policy initiatives in the EU? While these policies will likely mitigate the impact of the IRA on EU manufacturing production, as currently designed, they will also likely cause significant reallocation of economic activity and negative distortionary effects within the EU.

Countries with large fiscal capacity, in particular Germany, will likely benefit at the expense of their poorer neighbours. This could lead to significant tensions within the EU, and the euro area in particular.

To avoid such effects, industrial policy should be done mostly at the EU level (if at all) instead of at national level to prevent fragmentations of the European Single Market.

References

Acemoglu, D, D Autor, D Dorn, G Hanson, and B Price (2016), “Import Competition and the Great US Employment Sag of the 2000s”, Journal of Labor Economics 34(S1): 141–198.

Attinasi, M-G, L Boeckelmann and B Meunier (2023b), “Friend-shoring global value chains: a model-based analysis”, ECB Economic Bulletin.

Attinasi, M-G, L Boeckelmann and B Meunier (2023a), “Unfriendly friends: Trade and relocation effects of the US Inflation Reduction Act”, VoxEU.org, 3 Jul.

Autor, D, D Dorn, and G Hanson (2013), “The China Syndrome: Local Labor Market Effects of Import Competition in the United States”, American Economic Review 103(6): 2121–2168.

Caliendo, L and F Parro (2015), “Estimates of the Trade and Welfare Effects of NAFTA”, Review of Economic Studies 82(1): 1–44.

Eriksgård Melander, A, M Hallet, and D Costello (2019), “Germany and France: The case for structural convergence in the euro area”, VoxEU.org, 22 November.

Fadinger, H, P Herkenhoff, and J Schymik (2023), “Quantifying the Germany Shock: Structural Labor-Market Reforms and Spillovers in a Currency Union”, CEPR Discussion Paper No. 18225.

Juhász, R, NJ Lane, D Rodrik (2023), “The New Economics of Industrial Policy”, NBER Working Paper 31538.

Kleimann, D, N Poitiers, A Sapir, S Tagliapietra, N Véron, R Veugelers, and J Zettelmeyer (2023), “How Europe should answer the US Inflation Reduction Act”, Bruegel Policy Contribution 04/23.

Rodríguez-Clare, A, M Ulate, and J Vásquez (2020), “New-Keynesian Trade: Understanding the Employment and Welfare Effects of Trade Shocks”, NBER Working Paper 27905.

Schmitt-Grohé, S and M Uribe (2016), “Downward Nominal Wage Rigidity, Currency Pegs, and Involuntary Unemployment”, Journal of Political Economy 124(5): 1466–1514.

This article was originally published on VoxEU.org.