Decisions ahead and takeaways for the EU

Alicia García-Herrero is a Senior Fellow at Bruegel

Taiwan’s economy has transformed since 2016 under the leadership of the Democratic Progressive Party (DPP). In particular, the Taiwanese economy has diversified away from mainland China, while reliance on semiconductors is now even more acute than eight years ago.

In elections in January, the DPP won the presidency for a third term but lost overall control of Taiwan’s parliament, the Legislative Yuan. In contrast to the previous two terms, the DPP therefore needs to agree policy, including economic policy, with other parties. this could signal a softer approach in relation to the continuation of diversification away from the mainland.

Ongoing diversification

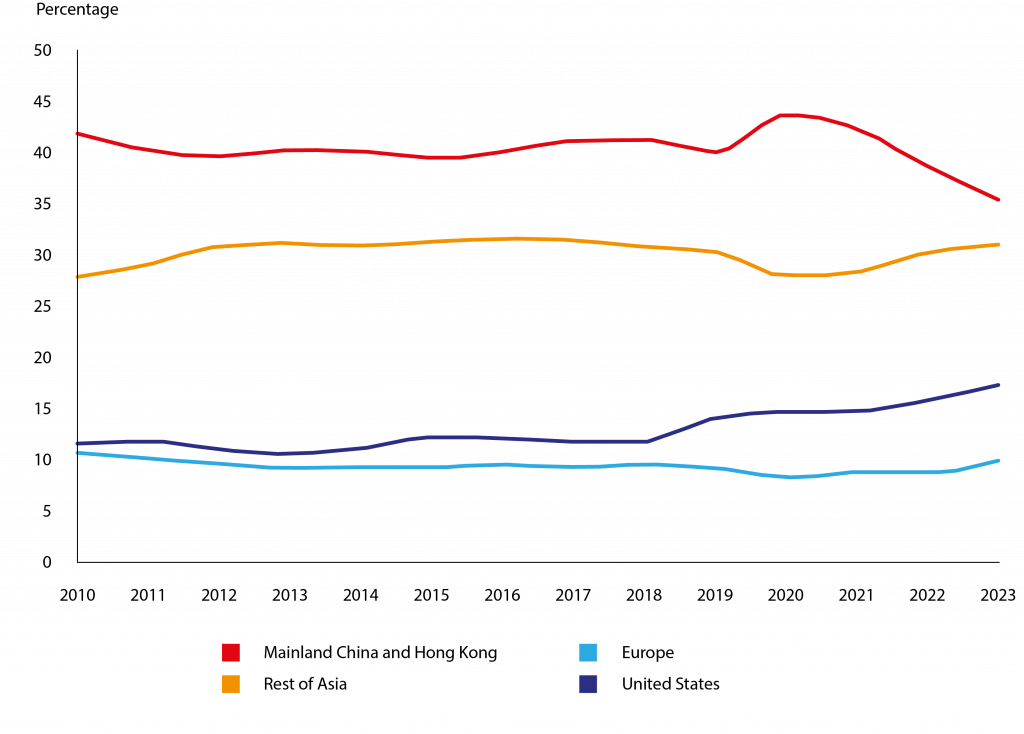

Mainland China remains Taiwan’s biggest export and investment destination, despite the share of Taiwan’s exports that go to China reducing from 40 percent on average between 2016 and 2019 to 35 percent in 2023 (Figure 1).

This has happened even though Taiwan signed a free trade agreement with mainland China in 2010 – the Economic Cooperation Framework Agreement (ECFA) – which at the time led to an increase in Taiwanese exports to the mainland. The COVID-19 pandemic in 2020 also triggered a sharp increase as the rest of the world entered a deep recession, but the trend has not lasted.

Since 2021, the share of Taiwanese exports going to the mainland has dropped significantly, influenced by US export controls on high-end semiconductors, with a clear knock-on effect on Taiwanese exporters.

Figure 1. Taiwan’s exports – destinations by % of value

Source: Bruegel based on Taiwan Ministry of Finance, CEIC.

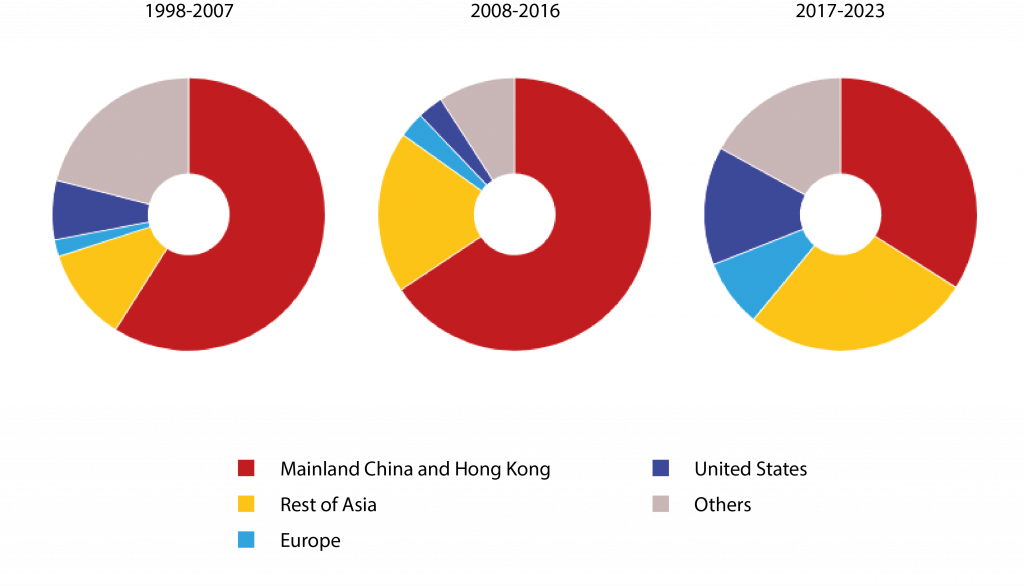

Taiwanese FDI into mainland China has also shrunk rapidly, from 65 percent of total Taiwanese FDI on average from 2008-2016 to 34 percent on average from 2017-2023 (Figure 2). The difference between these periods is that in the former, Taiwan was governed by the Kuomintang (KMT, Chinese Nationalist Party), which favours closer relations with the mainland, while in the latter period the DPP was in charge.

There are both geopolitical and economic reasons for mainland China’s falling share of Taiwanese FDI. First, the ECFA trade and investment agreement, reached under the first term of KMT President Ma Ying-jeou, was not extended when a new round of negotiations started in 2012, to include technological cooperation, finance and people-to-people exchanges.

A broader economic agreement between Taiwan and the mainland, mostly focusing on services – the Cross-Strait Service Trade Agreement (CSSTA) – fell victim to lack of consensus among Taiwan’s main political parties, increased tensions in the Taiwan Straits and student protests in Taiwan (the so-called Sunflower movement) in 20141.

Second, with the DPP victory in 2016, the new Southbound Policy2 was launched, offering incentives for Taiwanese companies investing in 18 Asian countries, including ASEAN3, India and other South Asian and Australasian nations.

In addition, rising labour costs in mainland China, the ongoing trade war between the US and China, an increased regulatory burden in the mainland and political tensions between the two sides of the Taiwan Strait also pushed Taiwanese businesses to look elsewhere to invest.

Working with business associations and chambers should be a key driving force to improve business relations between Taiwan and the EU, especially considering that the EU is the largest foreign direct investor in Taiwan

Figure 2. Taiwanese outward direct investment, destinations by % of value

Source: Bruegel based on Taiwan Ministry of Economic Affairs, CEIC.

The new political reality and geographical diversifiation

While the election winning DPP wants to see further diversification away from the mainland, the more pro-China party, the KMT, wants reinforced economic relations with China4. Because of the now-hung parliament, the DPP will need to take some of the KMT’s wishes into account it wants pass new rules, including those related to geographical diversification.

Beyond the two parties’ preferences, two other important issues also need to be factored in. First, geographical diversification requires open markets but Taiwan is increasingly unable to open any market through trade or investment deals.

Taiwan has spent the last eight years negotiating bilateral deals with its closest allies, Japan and the US, but the DPP administration has not even been able to complete these. Incoming President Lai has said that Taiwan should continue to push to be part of the Comprehensive and Progressive Agreement for Trans-Pacific Partnership (CPTPP), to which it applied in September 2021, but the reality is that Taiwan’s application has little hope of success.

China officially applied to be a member of the CPTTP only a couple of days before Taiwan. Since then, the United Kingdom has become a member of CPTTP, but the negotiation processes with Taiwan and mainland China have not started. Australian’s prime minister, Anthony Albanese, has expressed severe doubts about Taiwan’s ability to become member of CPTTP because of lack of international recognition of it as a nation-state5.

Second, while the DPP is likely to continue to offer more fiscal incentives to promote diversification in Southeast Asia and India (under the Southbound Policy), the fastest-growing destination for both exports and foreign direct investment from Taiwan is the United States, followed by Japan.

This can be explained by the ongoing artificial intelligence revolution, which needs semiconductors, and the decisions of some key Taiwanese chip companies (especially TSCM) to open factories overseas for chip production, with the US and Japan as the most important destinations.

In other words, the DPP’s push for geographical diversification might not be the main reason why diversification has happened; rather, it has been driven by market forces and business opportunities. This also means that the KMT push to maintain – if not deepen – economic ties with mainland China might not succeed unless China’s currently underwhelming economic performance turns around.

Implications for the European Union

So far, the EU has benefitted little from Taiwan’s trade and investment diversification, at least when compared to the US and the rest of Asia. The EU’s export share into Taiwan has remained practically stagnant (while the US has doubled its share), notwithstanding a large increase in exports from the Netherlands for a single item – ASML’s lithography machines for chip production.

The EU lacks a trade or investment deal with Taiwan, but so do some of Taiwan’s other trading partners, including the US. Considering that the EU is the largest foreign direct investor in Taiwan, the question arises of whether the EU should do more to foster more bilateral economic relations.

The gains could be substantial, especially from inbound FDI as Taiwanese investment focuses on high-end manufacturing. There has been some movement. A €5 billion investment in France by a Taiwanese company (ProLogium) was announced in May 2023 to build a battery factory6. TSMC announced in August 2023 a €4.5 billion investment in a semiconductor factory in Germany7.

But for the EU to catch up with Japan and the US as a recipient of outbound FDI from Taiwan, the result of Taiwan’s elections could be an obstacle. This is because the DPP will have less control of the economic agenda because it does not control the Legislative Yuan.

The close-to-impossible negotiation of a trade and investment deal between the EU and Taiwan – as shown by Taiwan’s difficulties in relation to Japan, the US and the CPTTP – does not point to any improvement in the institutional framework for economic relations to improve.

The question, then, is what can the EU offer to attract high-end foreign direct investment from Taiwan? Subsidies to attract semiconductor factories cannot be the only answer, given the very large amounts needed and the pressure such subsidies put on EU member states’ already stretched finances (Legarda and Vasselier, 2023).

Working with business associations and chambers should be a key driving force to improve business relations between Taiwan and the EU, especially considering that the EU is the largest foreign direct investor in Taiwan, while Taiwanese companies have been absent from the EU single market until recently.

Overall, the US and the rest of Asia have been the main winners from Taiwan’s rapid diversification of its economy away from mainland China. The EU, which is lagging, should work to enhance its economic exchanges with Taiwan. Hopefully the January 2024 election results will facilitate this. Most importantly, the EU should aim to attract more high-tech FDI from Taiwan.

Unfortunately, a better institutional framework through a trade/investment deal seems highly unlikely, for geopolitical reasons. This puts all the burden on chambers of commerce and other forums to improve business relations.

Endnotes

1. The Sunflower Movement was a student-led protest that occupied Taiwan’s Legislative Yuan to put pressure on the KMT government against signing a second cooperation deal with mainland China. See Ho (2018).

2. See the New Southbound Policy portal at https://nspp.mofa.gov.tw/nsppe/.

3. Brunei, Cambodia, Indonesia, Laos, Malaysia, Myanmar, Philippines, Singapore, Thailand and Vietnam.

4. Alicia García-Herrero, ‘Taiwan’s future economic direction hinges on the election outcome’, First glance, 12 January 2024, Bruegel.

5. Claudia Long and Stephen Dziedzic, ‘Albanese says Australia is unlikely to support Taiwan’.

6. France24, ‘Taiwanese battery maker Prologium to invest €5 billion in French factory’, 12 May 2023.

7. DW, ‘Taiwan’s TSMC to build semiconductor factory in Germany’, 8 August 2023.

References

Ho, M-S (2018) ‘The Activist Legacy of Taiwan’s Sunflower Movement’, Carnegie Endowment for International Peace, 2 August.

Legarda, H and A Vasselier (2023) ‘Navigating Taiwan relations in 2024: Practical considerations for European policy makers’, China Horizons, 21 December.

This article was originally published on Bruegel.