Climate risk stress tests underestimate financial sector losses

Henk Jan Reinders is an Economist at the World Bank and PhD researcher at the Rotterdam School of Management, Dirk Schoenmaker is Professor of Banking and Finance, and Mathijs Van Dijk is Professor of Finance, both at the Rotterdam School of Management at Erasmus University, Rotterdam

Central bank concerns about climate change are on the rise, and a plethora of new methods have been developed to assess the impact of climate-related shocks on the financial sector. This column reviews current climate risk stress test methods and identifies six types of climate shocks and four types of modelling approaches.

Given the complexity of the link between climate shocks and financial sector outcomes, the authors argue that current methods have several key limitations that may lead to significant underestimation of potential financial sector losses.

Climate change can potentially cause highly adverse shocks to the financial sector. Central banks and other policy institutions increasingly rely on a host of newly developed climate risk stress-testing (CRST) methods to assess these potential effects.

While traditional financial risk assessment methods typically assume that the future will be similar to the past, climate change is likely to lead to unprecedented and often detrimental changes in a broad set of regions and economic sectors over a long period of time. This implies a need for forward-looking risk assessments, based on those future outcomes that are potentially most detrimental.

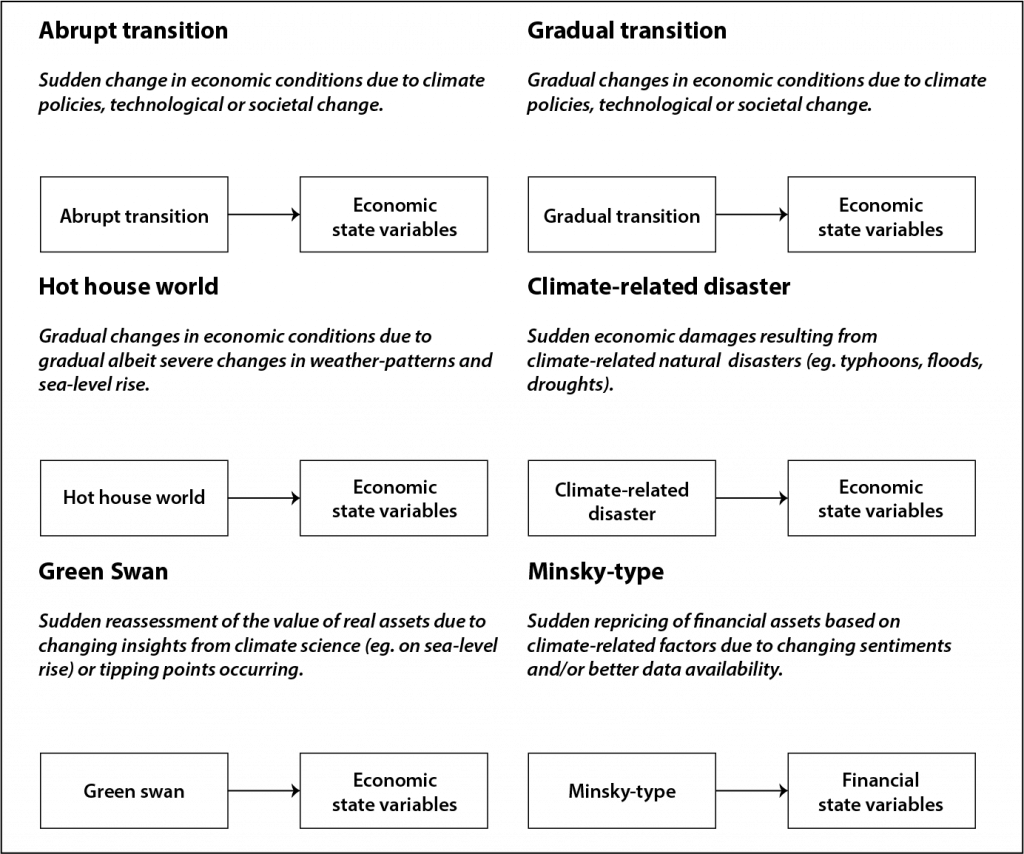

We identify six types of climate-related shocks that are relevant for climate risk assessments: abrupt transition, gradual transition, hot house world, climate-related disaster, ‘green swan’ events, and Minsky-type shocks. Figure 1 provides an overview.

We believe it is important that the next generation of CRST exercises assess the potentially most damaging scenarios and include feedback loops that can amplify shocks between climate, economic, and financial systems

Figure 1. Classification of climate shocks

Several of these shocks have been investigated in some detail in current CRST applications. These include orderly transitions, disorderly transitions, and gradual changes in economic conditions due to changes in weather patterns and sea-level rise. The latter is also referred to as a ‘hot house world’ scenario (NGFS 2022).

Disorderly transitions have primarily been investigated by looking at the sudden introduction of climate policies (eg. Battiston et al 2017) or policy uncertainty (Berg et al 2023). Furthermore, an emerging strand of literature investigates the occurrence of one or more climate-related natural disasters on financial institutions (Hallegatte et al 2022).

This type of shock is highly relevant from a financial stability perspective, as disasters may cause high losses for banks and manifest themselves in very short time horizons (Klomp 2014).

Other shocks have received much less attention. This is specifically the case for scenarios in which financial sector agents suddenly change their perception of current and future risks, which would be rapidly reflected in today’s market prices of financial instruments.

In the climate context, this could chiefly be for two reasons. First, a shock could emanate directly from our changing perception of the state of the global climate system. This could include the unexpected occurrence of climate tipping points or changing insights from climate science – for example, when research would find that sea-level rise occurs more quickly than previously thought.

Bolton et al (2020) label these tipping points and changing insights as a ‘green swan’ event. Second, a shock could emanate from the financial sector if it fails to continuously incorporate the latest climate science and financial sector agents suddenly do so at some point in time – for example, due to increased awareness, a large natural disaster event, or strongly improved climate risk data. We label the latter as a Minsky-type shock.

CRST modelling approaches

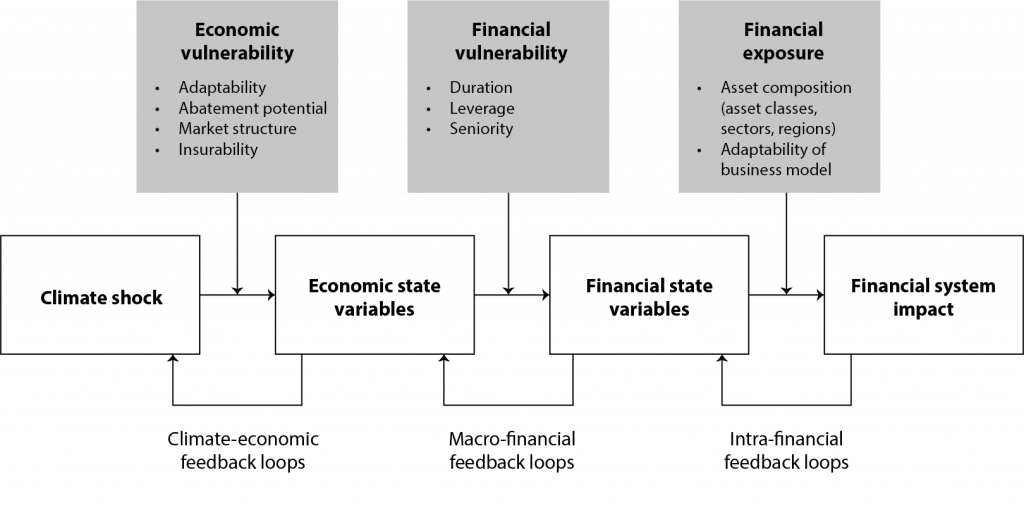

To assess the impact of climate shocks on the financial system, different modelling approaches are emerging. CRST must convert initial parameters (climate shocks) into key financial sector variables such as solvency and liquidity ratios.

The typical way that CRST methods do this is by employing macroeconomic models and translating shocks to key variables, such as GDP, into expected losses for the financial system. Additional modelling steps are often required to model the effect of severe climate shocks on the economy and financial system, as they do not have precedents in the past.

Furthermore, climate-related shocks often have specific sectoral and regional impacts, increasing the need for disaggregated (micro-based) modelling approaches. Our review of CRST methods (Reinders et al 2023) finds that, besides traditional macro-financial modelling, three new approaches are emerging:

1. The micro-financial approach focuses on firm or asset-level variables and uses valuation models and regression or structural models to estimate financial risk measures and losses.

2. The non-structural approach treats the economic effects of a shock as a black box and directly models the relationship between climate shock and financial outcomes, often using empirical methods.

3. The disaster risk approach links disaster risk models to financial sector outcomes, estimating the impact on variables such as economic damage and total factor productivity, which can be further linked to insurance liabilities or non-insurance financial variables.

Next to several relevant moderating effects, there are important feedback loops within the financial system (intra-financial), from the financial system to the economy (macro-financial) and from the economy to climate risk (climate-economic). These feedback loops are endogenous and may amplify the initial shock, as happened during the Global Financial Crisis of 2008-2009 (see Figure 2).

Figure 2. Moderating variables and feedback loops in the climate-financial relation

Policy recommendations

Given the complexity of the link between climate shocks and financial sector outcomes, we conclude that all CRST exercises to date have substantial drawbacks. CRST is a developing field with, so far, a wide variety of approaches to model the relation between climate shocks and financial sector outcomes. Common limitations include limited scopes (such as including only subsets of channels and asset classes) and incomplete modelling (such as excluding feedback effects).

Furthermore, our review points to an overreliance on macro models with low sectoral and spatial granularity and neglect of certain climate shock types. We conclude that these limitations may well lead to a significant underestimation of potential system-wide financial losses.

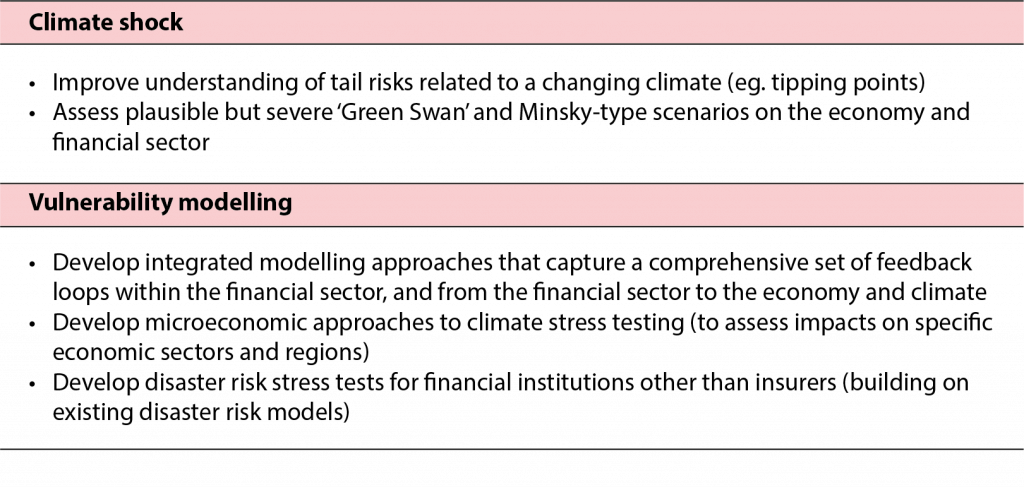

We offer suggestions for improving CRST approaches, summarized in Table 1. In particular, we believe it is important that the next generation of CRST exercises assess the potentially most damaging scenarios (such as ‘green swan’ events or rapid repricing of financial assets) and include feedback loops that can amplify shocks between climate, economic, and financial systems.

Table 1. Avenues for future research

References

Battiston, S, A Mandel, I Monasterolo, F Schütze and G Visentin (2017), “A climate stress-test of the financial system”, Nature Climate Change 7(4): 283–288.

Berg, T, E Carletti, S Claessens, J-P Krahnen, I Monasterolo and M Pagano (2023), “Climate regulation and financial risk: The challenge of policy uncertainty”, VoxEU.org, 10 May.

Bolton, P, M Després, L A Pereira da Silva, F Samama and R Svartzman (2020), The Green Swan, Bank for International Settlements, Basel.

Hallegatte, S, F Lipinsky, P Morales, H Oura, N Ranger, MGJ Regelink and HJ Reinders (2022), “Bank Stress Testing of Physical Risks under Climate Change Macro Scenarios: Typhoon Risks to the Philippines”, IMF Working Paper WP/22/163.

Klomp, J (2014), “Financial fragility and natural disasters: An empirical analysis”, Journal of Financial Stability 13: 180-192.

NGFS (2022), NGFS Climate Scenarios for central banks and supervisors. Network for Greening the Financial System, Paris.

Reinders, HJ, D Schoenmaker and MA van Dijk (2023), “Climate Risk Stress Testing: A Conceptual Review”, CEPR Discussion Paper DP17921.

This article was originally published on VoxEU.org.