A virtuous circle

Agustín Carstens is General Manager of the Bank for International Settlements

I will use my time to share some lessons learned during my career as a policymaker, which has now spanned more than four decades. At various times, I have had a front row seat during episodes of economic and financial crisis. Early in my career at the Bank of Mexico, I witnessed the debt crisis that hit many Latin American countries in the early 1980s and the 1994 ‘Tequila crisis’ in Mexico.

The Great Financial Crisis (GFC), which exploded in 2008, coincided with my tenure first as Mexican Finance Minister, and then as Governor of the central bank. The COVID-19 pandemic and its aftermath took place while I was in my current role at the BIS.

The crises of the 1980s and 1990s were felt most keenly in emerging market economies. Some considered advanced economies immune from such events. But the more recent crises have hit advanced economies as hard as emerging markets, if not harder. Indeed, in many respects the GFC had its epicentre in the most mature and largest advanced economies.

Crises often prompted important changes in policy frameworks. In many emerging markets, the crises of the 1980s and 1990s led to the adoption of more flexible exchange rate regimes, greater central bank independence from governments, a heightened focus on low inflation as the main monetary policy objective, fiscal discipline and a remarkable improvement in banking sector supervision and regulation.

Some jurisdictions also saw major structural reforms, including the liberalisation of product and labour markets and privatisation of public enterprises. The GFC and the subsequent period of low inflation led to a broadening of central bank policy instruments, particularly in advanced economies, including the introduction of quantitative easing and forward guidance. Needless to say, the recent inflation surge has prompted further reassessments in many policy dimensions.

A key development that has taken place over the course of my career is that economies have become significantly more integrated. They trade more with each other. And, due to the emergence of global value chains, they trade more intensively. We felt this intensely in Mexico, particularly after the introduction of the North American Free Trade Agreement (NAFTA) in 1994.

Today, I see this international trade integration from the vantage point of a resident of Basel, which lies at the intersection of Switzerland, France and Germany. And it is very evident here in Frankfurt, at the heart of the manufacturing powerhouse of Europe.

More generally, the global economy has become extremely dynamic. Information flows are unfettered, and firms and consumers very sophisticated. Even more importantly, as compared with when I began my career, financial markets have become much larger, more integrated and more fast-paced.

A side effect of all this is that the scope to sustain fundamentally flawed policy frameworks has diminished. In particular, global financial markets’ immense size and speed discipline policymakers and, at times, force policies to be realigned.

To be sure, financial markets do not get everything right. They can miss important signals and remain calm in the face of rising vulnerabilities. This can be a serious problem. The years leading up to the GFC were a case in point. It is precisely in tranquil times that the seeds of future distress are often sowed.

But when financial markets smell weakness, they can move very quickly. To quote another highly influential German economist, the late Rudiger Dornbusch: “Financial crises take much, much longer to come than you think and then they happen much faster than you would have thought.”1 When that happens, policymakers need to react very quickly, often amidst great uncertainty and with their credibility dented. Unsustainable policies disappear swiftly.

What are the key lessons that I take from my experience?

The first is that crises are costly and best avoided, and while adopting sensible policy frameworks can make them less likely, some crises, sooner or later, will occur.

The second is that as economies and financial markets continue to evolve rapidly over time, policy settings and even frameworks that seem appropriate today will need to change, at times very quickly.

Thus, it is critical that policymakers have the nimbleness and flexibility to adapt both to crises and to evolving economic and financial circumstances – it is a perennial challenge to adjust and recalibrate policy.

This takes me to the core issue that I would like to focus on today: the value of trust in policymaking. It is much easier to make the necessary changes if the public trusts policymakers and their policies. But the importance of trust goes beyond enabling change. In my view, only when trust is present can public policies succeed.

Trust in public policies

What does ‘trust’ refer to? Essentially, it refers to society’s expectation that public authorities will act predictably in the pursuit of predefined objectives and that they will succeed in their task.

Why is trust so important? If the public trusts authorities’ actions, they will incorporate those actions in their own behaviour. This makes it more likely that the authorities will achieve their objectives. In addition, if the public has trust in public policies, they will be more willing to accept measures that impose short-term costs but deliver long-term benefits. In sum, trust underpins the effectiveness and legitimacy of policies.

Policymakers acquire trust by achieving their objectives over time. Hence the importance of setting clear policy goals, which provide a benchmark against which to evaluate policy actions and assess their success or failure. But setting targets alone is not enough. Policymakers must also pursue them decisively, particularly when the environment changes.

There is a positive feedback loop in the dynamics of trust. Effective and legitimate policies make it easier for the authorities to achieve their objectives. This, in turn, feeds back onto trust, producing a virtuous circle. However, this dynamic can also work in the other direction and, at times, very quickly.

In the extreme, if trust evaporates, the capacity to make effective public policies disappears. Preserving credibility is therefore a constant challenge, and it requires consistency in public policies over time. Institutional arrangements, like independent central banks, can be very valuable for this purpose.

To establish, enhance and preserve macro-financial stability, it is essential that the public retain trust in all of the key macro policy dimensions – monetary, financial and fiscal policies – individually and as a group. This requires coherence between them.

Let me elaborate. I will begin with the most fundamental aspect of central banking: the nature of money. The social convention of money, as we know it today, is based on the trust placed in it by the public. And as money is the basis for the entire financial system, the system’s stability depends also on trust.

Fiat money is an asset that has no intrinsic value. It’s worth derives from the social convention that underpins it, and from the institution that enables it to function: the central bank. Money only has value if the public believes that others will honour that value, today and in the future. This ensures that when a person wants to use it, they know that there will be finality in the payment.

Thus, the value of money clearly comes from trust. That is why the issuer of money is so powerful. This power carries with it great responsibility. Those who abuse their ability to issue currency deprive money of its value and forfeit the trust of the public. Germany knows this all too well.

The consequences of the state abusing the privilege of issuing money can be disastrous. These can range from high inflation and sharp exchange rate depreciations to the substitution of the national currency in favour of a foreign one. In the extreme, for example in hyperinflationary episodes, there could even be a return to barter. Such events typically go hand in hand with financial instability, sharply lower economic growth, widespread job losses and soaring inequality.

The consequences of losing trust in money were a key reason for the emergence of central bank autonomy. After all, autonomous central banks are nothing more than institutions within the state with a mandate to preserve the purchasing power of the national currency. Their autonomy is the social engineering that solidifies society’s trust in money.

Germany’s experience in the 20th century illustrates vividly why trust in money matters. The contrast between the hyperinflation of the 1920s and the monetary stability that followed the foundation of the Deutsche Bundesbank could not be starker. And it is fair to say that the success of the Bundesbank inspired the emergence of central bank independence worldwide.

In recent decades, many central banks have followed the Bundesbank’s lead and adopted monetary arrangements that allow them to anchor expectations and preserve money’s purchasing power. Inflation targeting regimes are the most common framework to ensure this. The Bank of Mexico and the European Central Bank apply their own versions. But what does inflation targeting consist of?

Central banks do not control inflation directly. But their policy tools can influence it. When a central bank adopts an inflation target, it commits to use its tools to achieve that target. If the public trusts the central bank, then the inflation target, rather than current inflation, becomes a key reference point for price and wage decisions.

This contributes to low and stable inflation. Inflationary episodes are usually short-lived, reflecting changes in relative prices. Inflation becomes self-equilibrating and ceases to have a material influence on the behaviour of households or businesses.

That is why the inflation outbreak that followed the COVID pandemic and the onset of the Ukraine war was so concerning. The trust central banks had gained over many years could have been lost if society had started to doubt their commitment to price stability. Some generations experienced for the first time the risk of the economy transitioning to a high-inflation regime.

Once that transition starts, it can become increasingly difficult to stop. Therefore, it was necessary and appropriate for central banks to tighten policy forcefully and decisively through higher interest rates to restore price stability. The tighter stance may need to be maintained for a long time, for only through resolve, perseverance and success can trust in money be preserved.

Building resilient and robust economies and financial systems is the best way to ensure that policies remain effective, so that they can be deployed when they are needed the most

Commercial bank money also needs to command trust. It is well known that the money issued by the central bank, known as primary money, is not the only money that circulates in a modern economy. Commercial bank money, in the form of bank deposits and credits, is what most households and businesses use for the bulk of their day-to-day transactions. It is thus fundamental to the monetary system. At the same time, for most people primary and commercial bank money are indistinguishable. That is by design.

Over time, institutional arrangements have evolved to extend society’s trust in primary money to commercial bank money in a two-tiered monetary system. The central bank lays the foundation, and on the first floor are commercial banks.

The key is that interbank payments ultimately settle on the central bank’s balance sheet, through the exchange of primary money between commercial banks. This guarantees the finality of payments and the singleness of commercial bank money.

The ultimate settlement of the banking system at the central bank is made possible by the central bank’s ability to create liquidity by lending to the banking system. At times of great instability, the central bank can also provide additional liquidity through its well-known function of lender of last resort. In doing so, it safeguards the public’s trust in the entire monetary system.

To put into perspective the enormous value of the framework I have just described which supports trust in primary and bank money, it is useful to consider recent failed attempts to issue private money through technologies that allow transactions based on decentralised ledgers.

These alleged forms of money function without central bank intervention, a lender of last resort or a reliable regulatory and supervisory framework. They have led to the proliferation of so-called cryptocurrencies, which cannot guarantee finality of payments nor a stable value, and so clearly lack the fundamental attributes of money.

These developments reinforce the point that what sustains fiat money over alternatives based on novel technologies is the institutional framework and the social convention that support it, which are precisely what makes it reliable for the public.

However, the mere existence of a two-tier monetary system is not enough to guarantee trust. The banking system must also remain solvent. Because banking crises have large social costs, the system should be extensively regulated and supervised.

A complement is deposit insurance, which exists to forestall potential bank runs. These layers of protection aim to safeguard the public’s savings and are manifested in trust in both primary and commercial bank money.

Banks’ resilience has increased markedly since the GFC. We reaped the benefits of the comprehensive regulatory and supervisory response to that crisis in the COVID pandemic, as banks were able to play a vital role in keeping economies afloat. Even when banking stress emerged in 2023, the post-GFC reforms and authorities’ rapid deployment of crisis management tools limited the fallout to only a handful of institutions.

Nonetheless, there is still work to do to bolster the banking sector’s resilience. Make no mistake, the core responsibility lies with banks themselves. There is no substitute for sound business models, adequate risk management and effective governance. But banking supervision needs to up its game to identify and remedy problems at banks proactively2. And we need timely, full and consistent implementation of banking reforms and regulations, including Basel III.

Recent decades have also seen rapid growth in the non-bank financial system. This sector comprises mainly activities involving securities, including debt instruments and broader forms of intermediation performed by insurance companies, private credit, investment service companies and hedge and pension funds, among others. In many countries, non-bank financial intermediation has for some time now accounted for over half of the financial system.

The need for greater supervision and regulation of the non-bank sector has become more pressing in the light of recent episodes of extreme instability. One reason is to prevent nefarious arbitrage between regulated and unregulated financial activities.

In addition, the sector’s interconnectedness with the traditional banking system and the tendency of non-bank intermediation to generate opaque and excessive leverage and substantial liquidity mismatches create systemic risks. Unforeseen events in this sector can trigger systemic financial crises.

In recent years, some central banks have had to act as ‘market-makers of last resort’ to defuse crises and preserve trust in the broader financial system. Because such actions may conflict with central banks’ measures to preserve price stability, greater regulation and supervision of the non-bank financial sector are indispensable.

Within the universe of debt instruments, public debt is of particular importance. If used appropriately, public debt allows governments to successfully function. But, from a macro-financial point of view, it is important that any public debt is, and is seen to be, sustainable. Investors must trust the government to meet its financial obligations, without resort to central bank financing.

Public debt plays a strategic role. It is considered the instrument with the lowest credit risk, making it essential for grounding the risk of asset portfolios, particularly those of banks. In addition, public debt serves as the main reference for valuing other forms of debt, for example corporate debt.

Hence, defaults on public debt compromise the stability of the whole financial system. They also threaten monetary stability since the central bank, even if it is formally autonomous, could find it necessary to finance debt service with primary issuance, leading to fiscal dominance of monetary policy. Under these circumstances, economies would cease to have a nominal anchor and would be cast adrift.

The result would be rising inflation and sharp exchange rate depreciations. We can thus appreciate the vulnerabilities that can be triggered if trust in public finances is lost.

In the light of these considerations, it is imperative for fiscal authorities to curb the relentless rise in public debt. The post-GFC low interest rate environment flattered fiscal accounts. Large deficits and high debt seemed sustainable, allowing fiscal authorities to avoid hard choices. But the days of ultra-low rates are over.

Fiscal authorities have a narrow window in which to get their house in order before the public’s trust in their commitments starts to fray. As I pointed out earlier, financial markets can remain calm in the face of large imbalances until suddenly, one day, they no longer are.

That is why fiscal consolidation in many economies needs to start now. Muddling through is not enough. In many countries, current policies imply steadily rising public debt in the coming decades. Demands for more public spending will only increase, not least due to population ageing, climate change and, in many jurisdictions, higher defence spending.

Fiscal authorities must provide a transparent and credible path to safeguard fiscal solvency, ideally supported by stronger fiscal frameworks. And they must follow through on their commitments.

Fiscal health is not only about avoiding crises. It also brings material benefits. The lower long-term interest rates and debt service burdens enjoyed by Germany, compared with some of its advanced economy counterparts, are a prime illustration. Greater trust in public finances also increases fiscal space. This allows fiscal authorities to maintain trust even in the face of adverse events that require expansionary policy responses as, once again, Germany’s recent experience has illustrated3.

It is clear from what I have discussed that trust in the various aspects of macroeconomic policy – monetary, financial stability and fiscal – is closely interrelated. Monetary instability imperils financial stability, erodes the willingness of investors to hold public debt and hammers public confidence. Financial crises have large fiscal costs. And loss of confidence in public finances compromises the stability of the whole financial system and can undermine price stability.

This could happen because of political pressure to keep interest rates low to maintain fiscal space. But it can also occur if central banks perceive that raising interest rates risks triggering a sovereign debt crisis. Either way, monetary and financial stability are seriously undermined.

Thus it is essential to preserve trust in all pillars of a country’s macro-financial frameworks, and for there to be consistency between them. In practice, this represents a great challenge due to the multiple authorities involved and the existence of unavoidable political motivations, especially with regard to fiscal policy. This is not an insurmountable problem, but it highlights the need for consistency and coordination of public policies.

In this context, I think it is unavoidable to mention the need for consistent policy frameworks in the euro area. While the institutional environment features a single monetary policy, there is no fiscal authority, and movement towards a fuller banking and capital union has been slow.

This hinders coherence and can make the euro area more vulnerable, as we witnessed during the sovereign debt crisis. The best institutional framework to deliver policy coherence is open for debate, but the value of coherence itself seems self-evident.

Let me add a final reflection on the credibility of fiscal and monetary policy today. Recent experiences should prompt a reassessment of the appropriate role of monetary and fiscal policy and greater realism about what they can deliver. Fostering unattainable expectations about policymakers’ ability to smooth out every economic pothole will ultimately lower trust in public policies.

For monetary policy, a prudent approach would be to avoid excessive ‘fine-tuning’. Central banks should not be called upon to stabilise inflation at very short horizons and within narrow ranges.

This is particularly important because, as recent events have shown, inflation will partly depend on factors that are not under central banks’ control.

For fiscal policy, prudence requires allocating scarce fiscal resources to measures that can raise future growth. In addition to the green transition, this includes improving healthcare systems, spending on education and improving infrastructure.

Above all, we must remember that structural reforms are the best tool to sustainably increase a country’s growth potential.

Towards a soft landing?

Let me start wrapping up by highlighting the recent positive developments in the fight against inflation. It seems that we are on route to a soft landing, thanks to the forceful, opportune and decisive monetary policy response.

Lower inflation, combined with surprisingly resilient activity and labour markets, suggests that we are on the right course. Financial markets seem to agree – the prices of shares and other risky asset classes have reached new highs in recent months.

In the light of the enormous strains placed on the global economy in recent years, a soft landing would be an impressive outcome. It would surely bolster trust in macroeconomic policymaking. So, where do we stand?

On the inflation front, the news is good. The monetary medicine is working. A year ago, inflation averaged 7% in advanced economies. Today it is 3%. In emerging market economies, excluding a few outliers, inflation averages 4%.

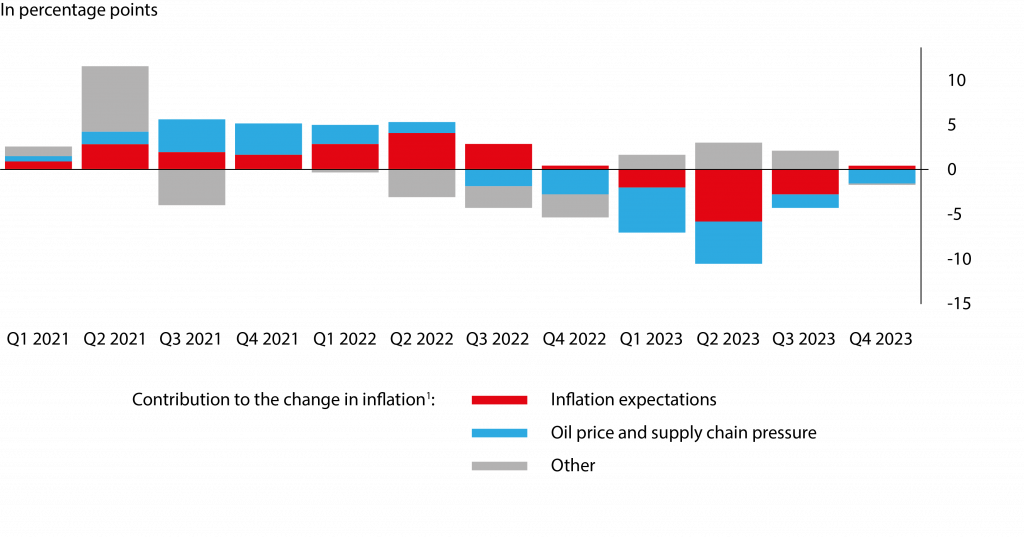

Admittedly, central banks cannot claim all of the credit. As the blue bars in Graph 1 show, lower commodity prices and the easing of pandemic-related supply disruptions also played a role. I am showing here estimates for the United States, although the story for the euro area would be similar.

Graph 1. Contributors to disinflation: decomposition

1 Contributions to the change in quarter-on-quarter inflation over past year based on a linear regression model using data for the United States.

Sources: Federal Reserve Bank of New York; Federal Reserve Bank of St Louis, FRED; Bloomberg; BIS.

Central bank actions were felt in other ways, however. Tighter monetary policy restrained demand. Just as importantly, central banks’ accumulated trust allowed them to bring inflation down without the need for a large recession.

This was a stark contrast to the end of the most recent global inflationary outbreak in the late 1970s, which occurred at a time when many central banks lacked credibility as inflation fighters. Central banks’ public commitment to restore price stability, and decisive actions in pursuit of this objective, prevented changes in ‘inflation psychology’ from taking hold and kept second-round effects at bay.

As the red bars in Graph 1 show, measures of inflation expectations, which rose concerningly at the start of the inflation outbreak, began to fall shortly after central banks started to raise rates.

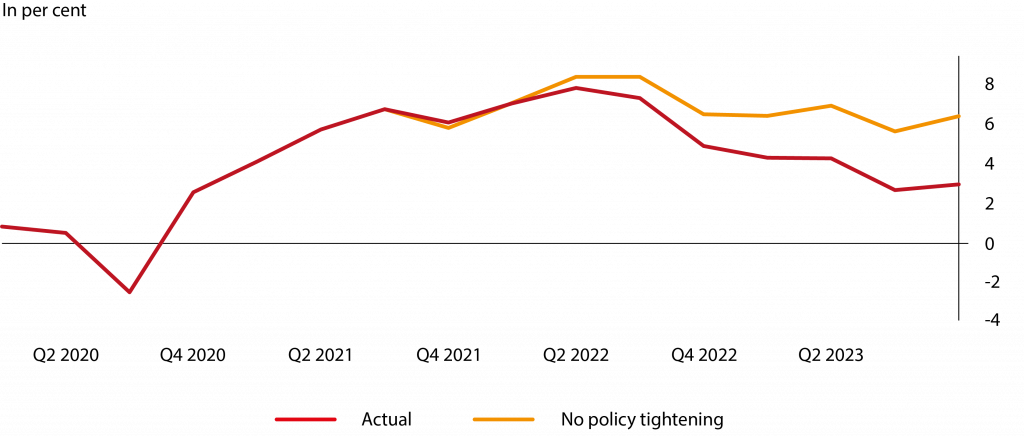

Simulations by some of my BIS colleagues, shown in Graph 2, illustrate that, if central banks had not tightened policy, inflation would have stayed high, even as the pandemic-related supply shocks faded4. Through their actions, central banks showed their firm commitment to achieving their mandates.

Graph 2. Inflation would have remained much higher without central bank actions

Based on simulations from a medium-scale macroeconomic model of the United States.

Sources: Federal Reserve Bank of St Louis, FRED; BIS.

Lower inflation has come at a remarkably small cost to the real economy. To be sure, global growth has slowed. Here in Europe, we narrowly avoided a recession last year. But labour market conditions remain firm and, at a global level, the growth slowdown is shallow. Against a backdrop of the largest and most synchronised monetary policy tightening in decades, this is an impressive achievement.

A strong recovery in aggregate supply was an important contributor. It helped support output while lowering inflation. Without the supply recovery, disinflation would have been harder. But we should not forget that, without tighter monetary policy, there would have been no disinflation.

A soft landing is not guaranteed, however. Central banks’ job is not done. While inflation is lower, it is still above central banks’ targets. And there will surely be more bumps in the road. The medium-run risks to inflation – such as deglobalisation, economic fragmentation, adverse demographic trends and the need to fight climate change – reinforce the need for central banks to stay the course. It is only in this way that the public’s trust in money can be preserved.

Conclusion

The events of the past decades presented policymakers with frequent and intense challenges. Facing extraordinary strains, policymakers strived to preserve the value of money, and keep their economies and the financial system functioning. These challenges showed the importance of the public’s trust in policymakers, which allowed for decisive action. And policies worked better when they were each part of a coherent whole.

As Goethe wrote in Faust: “Es irrt der Mensch, solang er strebt” – man errs as long as he strives. Policymakers did not get everything right. Nonetheless, their attempts to make good choices were noticed by society.

If the events of the 21st century so far are a guide, we should not expect plain sailing in the coming decades. Building resilience will require policymakers to apply an appropriate policy mix and communicate it effectively. Monetary policy will need to prioritise the inflation fight, until it is decisively won and price stability is restored.

Financial stability policy needs to ensure a resilient banking sector and address remaining regulatory gaps. Fiscal policy will need to rationalise expenditure while making room for vital investments in our future. But these policies are unlikely to be sufficient even if applied jointly.

Ultimately, to improve economic resilience and enhance sustainable growth, governments must rediscover the appetite for structural reforms that has been absent for far too long.

I would like to leave you with this last thought. Part of preserving trust is to know the limits of what policies can deliver. Expecting policymakers to deploy extraordinary macroeconomic policies to respond to every challenge is a sure way to erode the public trust.

Building resilient and robust economies and financial systems is the best way to ensure that policies remain effective, so that they can be deployed when they are needed the most.

Endnotes

1. R Dornbusch and S Fischer, “International financial crises”, CESifo Working Paper, no 926, 2003.

2. See A Carstens, “Investing in banking supervision”, speech at the European Banking Federation’s International Banking Summit, Brussels, 1 June 2023.

3. See J Nagel, “Fiscal policy challenges in a high inflation environment”, speech at the Forum Finanzpolitik und Steuerrecht, Baden-Baden, 10 November 2023.

4. See P Amatyakul, F De Fiore, M Lombardi, B Mojon and D Rees, “The contribution of monetary policy to disinflation”, BIS Bulletin, no 82, December 2023.

This article is based on a lecture by delivered at the Center for Financial Studies and the House of Finance at Goethe University, Frankfurt, 18 March 2024.