A way out via the Strait of Hormuz

Simon Johnson is the Ronald A Kurtz Professor of Entrepreneurship and Head of the Global Economics and Management Group, Sloan School of Management; Co-Director, Stone Center on Inequality and the Future of Work at Massachusetts Institute of Technology (MIT); Amir Kermani is Assistant Professor, Haas School of Business, at the University of California, Berkeley

The US–Iran relationship appears to be at its lowest point in decades. Following the intense strikes launched on 28 February 2026, the assassination of Supreme Leader Ali Khamenei and a number of other leaders, Iran’s effective closure of the Strait of Hormuz, and President Trump’s subsequent naval blockade, the two countries seem locked in an intractable confrontation. Yet beneath the escalation lies a paradox: the very instruments that have deepened the crisis may also contain the seeds of its resolution.

The nuclear issue, time inconsistency, and political debt overhang

For over two decades, proposed solutions to the Iranian nuclear question have centred on a simple exchange: Iran limits or gives up its nuclear programme in return for sanctions relief. The core challenge is a classic time-inconsistency problem.

Once Iran incurs irreversible costs, there is enormous temptation for the US to reimpose sanctions and push for further concessions. History bears this out. Despite Iran’s compliance with the 2015 nuclear deal, the US withdrew in May 2018, reimposed tough sanctions, and no further agreement emerged.

The cumulative cost of sanctions has been enormous. Laudati and Pesaran (2023) estimate that sanctions reduced Iran’s annual growth by about 2 percentage points over 1989 to 2019, implying the economy could have been roughly 50% larger. Farzanegan and Habibi (2025) find that sanctions reduced the size of Iran’s middle class by 30%.

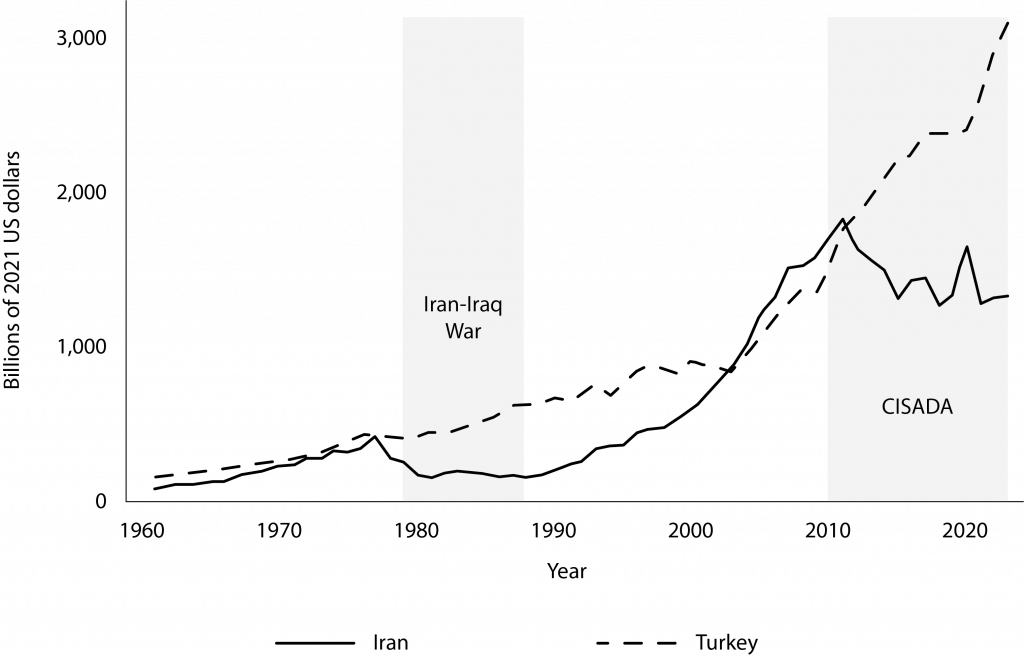

A comparison with Turkey is illustrative. The two countries had similar GDP and GDP per capita before 1979. By the end of the Iran-Iraq War in 1988, Iran’s economy was only one-third the size of Turkey’s, but this gap was nearly closed by 2001. The two economies then grew largely in tandem until 2010, when the enforcement of comprehensive financial sanctions caused their trajectories to diverge sharply. Today, Iran’s economy is less than half the size of Turkey’s.

Figure 1. Real GDP (output-side, PPP-adjusted) for Iran and Turkey, 1960–2022

Given this asymmetry, where sanctions impose devastating costs on Iran but are nearly costless for the US, it is very difficult for any US administration to resist the temptation of reimposing sanctions once Iran has made irreversible concessions on the nuclear issue.

There is a second problem related to the nuclear issue. Both countries have invested heavily, materially and rhetorically, in the nuclear dispute, and both now need to show a meaningful victory to their domestic audiences.

This creates what we call ‘political debt overhang’ (Johnson and Kermani 2026): accumulated political commitments that constrain leaders’ choices, because changing course would carry significant political costs, from appearing to concede to alienating core supporters, even when the new policy is substantively better than available alternatives.

On the Iranian side, decades of sanctions have closed off major economic opportunities. Restoring growth above 5% would require annual investment exceeding $50 billion in infrastructure and the oil and gas sector. A deal offering only limited sanctions relief simply cannot justify giving up the nuclear programme.

On the US side, the dynamic is strikingly similar. The 2015 deal placed meaningful limits on Iran’s enrichment capabilities. Any successor agreement must be seen as an improvement. But the threshold has risen considerably. The recent wars have imposed significant casualties and economic costs on both sides, making it even harder to accept terms that do not clearly surpass what was previously on offer.

The most recent 40-day war has demonstrated that Iran has a new source of leverage: closing the Strait of Hormuz to commercial shipping

A new bargaining chip may change the game

The most recent 40-day war has demonstrated that Iran has a new source of leverage: closing the Strait of Hormuz to commercial shipping. While Iran cannot unilaterally benefit from this leverage, given the US counter-blockade, it can use the threat of future closures to impose meaningful costs on US allies in the region, on global oil prices, and on the American and world economy. Unlike sanctions or military strikes, where costs fall disproportionately on Iran, disruptions to the Strait hurt both sides in a more proportional manner.

Therefore, a new agreement can link resolution of the nuclear issue, meaningful sanctions relief, and unrestricted flow of ships through the Strait together. If these elements are tied together, so that continued lifting of sanctions (ie. not reimposing sanctions once they are lifted) depends on the normal flow of traffic through the Strait and vice versa, then both sides face higher costs if they break the agreement. The key difference between agreeing to keep the Strait open and agreeing to shut down the nuclear programme is that the former does not suffer from a time-inconsistency problem.

Political debt overhang: why a small deal won’t work

Even if a new deal overcomes the time-inconsistency problem, it also needs to address political debt overhang so that the new agreement is presentable as a clear victory to domestic audiences on both sides.

From Iran’s perspective, the central weakness of the 2015 deal was not only its vulnerability to reversal but also the limited economic gains it delivered. Sanctions relief proved partial and fragile, and the agreement did not generate the level of investment or trade integration needed to create durable constituencies in favour of its continuation.

From the US perspective, the deal was viewed as too narrowly scoped. The absence of clear channels through which US and allied firms could benefit reduced domestic support, while concerns over the expiration of key provisions reinforced the perception that it provided limited long-term leverage.

A revised framework can address these deficiencies by embedding stronger, more visible economic linkages into the agreement itself. Rather than treating sanctions relief as a passive outcome, it can be structured as an active mechanism tied to specific large-scale investments, particularly in civilian infrastructure and the energy sector.

This helps Iran’s middle class the most and can also create stakeholders with a direct interest in the agreement’s survival. Iran’s frozen assets, instead of being released as unrestricted liquidity, could also be channelled into financing these projects.

A role for China

Given the depth of mistrust between Iran and the US, reaching a comprehensive agreement through direct negotiations alone will be difficult. China is uniquely positioned to play a decisive role in brokering a deal. As Iran’s single largest oil customer, Beijing enjoys substantial trust in Tehran and meaningful economic leverage.

China also has strong incentives to act: importing roughly 10 million barrels of oil per day, a $40 increase in oil prices costs China approximately $150 billion annually, with total impacts likely exceeding $200 billion when higher LNG, fertiliser, and other input costs are included.

China is also well positioned to supply the capital goods needed for Iran’s investment in renewable energy and civilian infrastructure. The planned Trump-Xi summit in mid-May 2026 provides a natural moment to advance elements of a deal.

The narrow path forward

We do not underestimate the obstacles. Both sides have incentives to project strength and signal they can outlast the other. Without a comprehensive agreement, the Strait is unlikely to remain stably open.

But the structural logic points toward an eventual deal. The costs of continued confrontation are real and mounting. The new symmetry of leverage provides, for the first time, a credible mechanism to enforce compliance over time.

And the scale of potential economic gains creates the basis for a package large enough to overcome political debt overhang on both sides. The question is whether leadership in Washington, Tehran, and Beijing will recognise this window before it closes.

References

Farzanegan, MR and N Habibi (2025), “The effect of international sanctions on the size of the middle class in Iran”, European Journal of Political Economy 90: 102749.

Johnson, S and A Kermani (2026), “Is a lasting US–Iran deal now possible? Overcoming time inconsistency and political debt overhang”, CEPR Policy Insight No. 150.

Laudati, D and MH Pesaran (2023), “Identifying the effects of sanctions on the Iranian economy using newspaper coverage”, Journal of Applied Econometrics 38(3): 271–294.

This article was originally published on VoxEU.org.