Relationship stickiness in international trade

Julien Martin is a Full Professor at the Université du Québec à Montréal (ESG-UQAM), Canada, Isabelle Mejean is a Professor at Sciences Po Paris, and Mathieu Parenti is Assistant Professor of Economics at ECARES, Université Libre De Bruxelles

Global supply chains have become a significant concern for policymakers worldwide, especially in light of the supply chain pressures arising from the COVID-19 pandemic and escalating geopolitical tensions (Baldwin et al 2023). The vulnerability of supply chains to disruptions related to trade, such as tariff wars, natural disasters, pandemics, wars, or other unforeseen events, is closely tied to the dynamics of firm-to-firm trade relationships within the supply chain.

Specifically, a firm’s vulnerability tends to be more pronounced when it is entrenched in trade relationships (Antras and Chor 2013). Locked-in effects limit a firm’s capacity to adapt to shocks by switching suppliers, which is a crucial aspect of shock mitigation in conventional trade models. The degree of such stickiness thus determines the cost of shocks, which influences the opportunity to adopt de-risking strategies (Baldwin and Freeman 2022).

Several factors contribute to locked-in situations, including the challenges of identifying alternative suppliers, the existence of long-term contracts, and investments specific to the relationship (Antras and Helpman 2004). In a recent paper (Martin et al 2023), we consolidate these elements under the term ‘relationship stickiness’. While this concept is essential for describing the nature of trade ties, the existing trade toolkit lacks a well-defined measure of relationship stickiness.

A new measure of trade relationship stickiness

The question then arises: how can we measure and quantify relationship stickiness? Our hypothesis is that relationship stickiness predominantly varies across different product categories.

For instance, we anticipate minimal stickiness for commodities traded on spot markets but expect higher stickiness for products requiring extensive customisation for each client, such as car doors. Based on this premise, we develop a measure of product stickiness at the 6-digit Harmonized System (HS) level, which can be merged with widely available trade datasets.

We begin with a simple intuition: in sticky product categories, firms cannot easily switch from one supplier to another. Therefore, the duration of trade relationships becomes a valuable indicator of stickiness. Of course, relationships may last longer for reasons that are orthogonal to product-market characteristics, eg. because of a good match between the firm and its supplier.

We incorporate these considerations into a theoretical framework, enabling us to map the duration of firm-to-firm relationships to an indicator of relationship stickiness. Subsequently, we leverage detailed firm-to-firm data on French bilateral trade to estimate relationship stickiness.

We end up with a measure of stickiness for 5,000 HS6 product categories. A natural question is whether our measure correlates with established characteristics of product markets commonly used in the trade literature. The short answer is affirmative, but none of these measures, even when combined, explains a significant fraction of the estimated dispersion. More specifically:

Product-level characteristics used in the literature, such as product differentiation, upstreamness, and product complexity, all correlate with our measure in the expected way. However, they jointly explain around 10% of the dispersion in stickiness. This implies that our measure captures dimensions of heterogeneity that are not encompassed by other variables.

Our measure also correlates with proxies for search frictions and market thickness as well as measures of technological specificity. Market and technological determinants respectively explain about 12% and 14% of the dispersion in relationship stickiness.

Stickiness explains 10% of the dispersion in the share of intra-firm trade in the US across industries. Note that causality operates bidirectionally here: firms might opt for integration with the producers of their most sticky inputs, yet vertical integration also generates mechanical stickiness in firm-to-firm relationships.

Stickiness is anticipated to influence the resilience of international trade ties, the adjustments of trade flows, and the scope and design of de-risking strategies

Stickiness with gravity

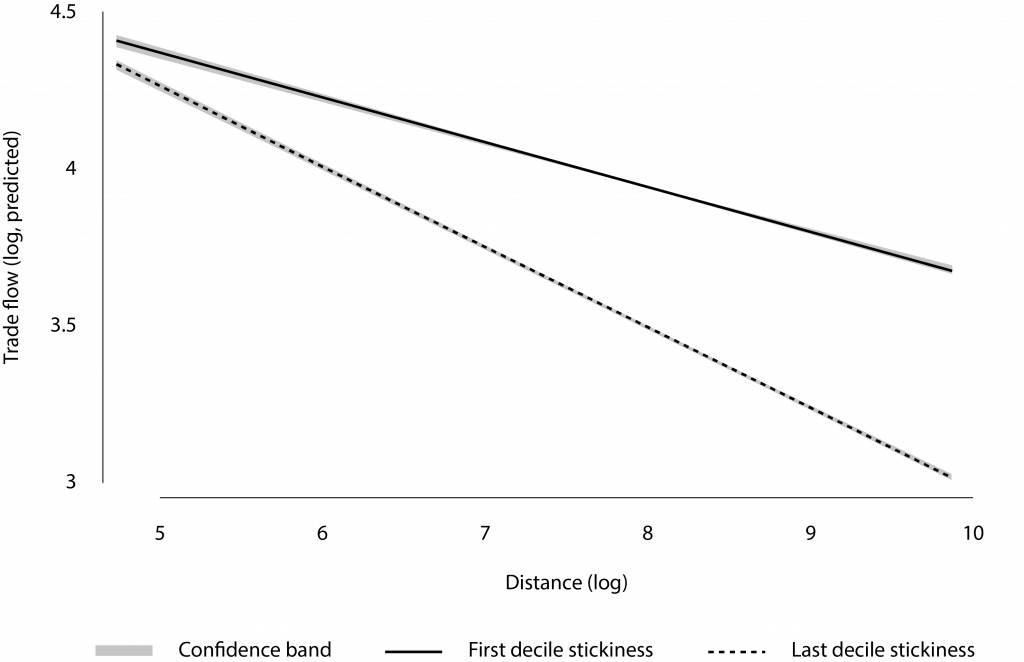

A nice feature of the measure is that it can be easily merged with widely used trade datasets, to revisit standard empirical facts. We analyse the interplay between distance and relationship stickiness in a gravity equation estimated on product-level multilateral data. Our estimates confirm the adverse effect of distance on the magnitude of trade.

Figure 1 further shows that the distance elasticity is magnified in stickier product markets. A possible interpretation is that the impact of distance is in part a consequence of trade involving monitoring costs, which are i) larger in stickier markets, and ii) increasing in distance (Head and Ries 2008).

Figure 1. Predicted impact of distance on trade flows for products in the top decile vs. bottom decile of the distribution of our index

Note: Prediction based on Martin et al (2023); Column 4 Table OA.8.

Stickiness and the heterogenous impact of uncertainty shocks

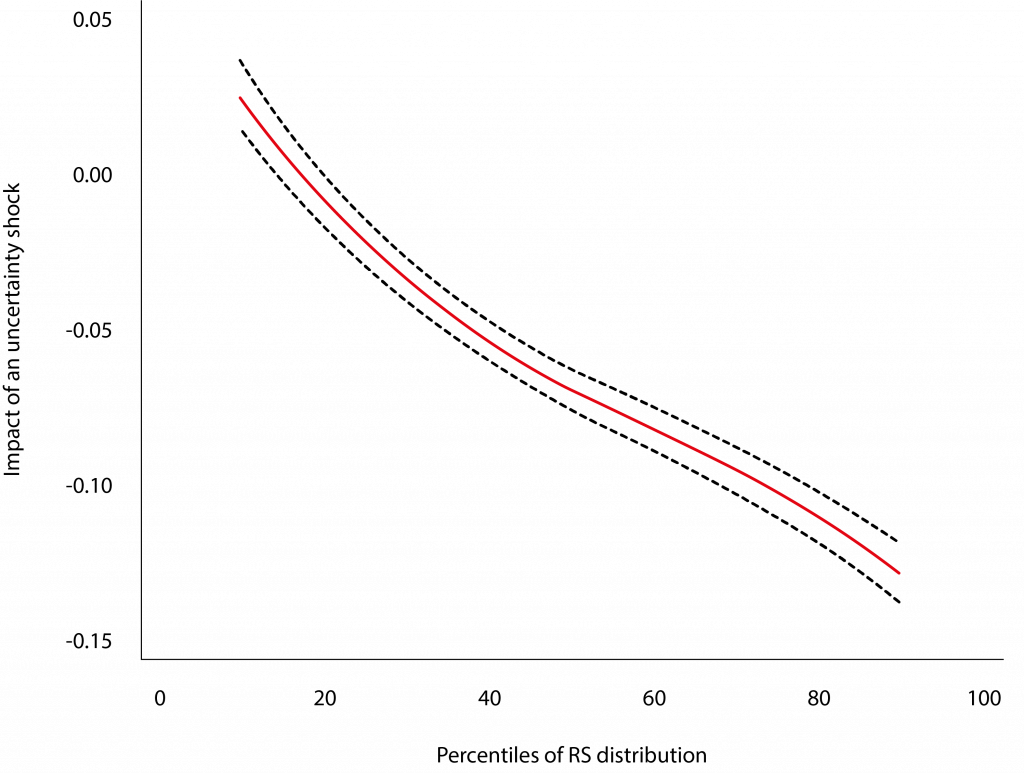

In our paper, we then explore how relationship stickiness shapes the adjustment of trade flows to macroeconomic shocks. Our focus is on uncertainty shocks, and we estimate the extensive margin response of French exports to an increase in uncertainty in the destination country.

Figure 2. Impact of an uncertainty shock on new relationships along the distribution of stickiness

Note: Percentage-point impact of an uncertainty shock on the number of new relationships.

Source: Martin et al (2023).

The results of this analysis are summarised in Figure 2. The figure shows that high uncertainty episodes are associated with a significant reduction in the number of new firm-to-firm relationships, aligning with the intuitive notion that uncertainty discourages firms from engaging in new economic activities.

Importantly, the extensive margin response is stronger in sticky product categories compared to less sticky ones: in high-uncertainty episodes the number of new firm-to-firm relationships drops by 1.5% for products in the bottom quartile of the distribution of relationship stickiness versus 10% for products in the top quartile.

The paper further analyses firms’ disruption of relationships and the intensive and extensive adjustment along the distribution of stickiness. All our findings consistently support the notion that trade adjustments are intricately shaped by the degree of relationship stickiness in product markets.

Stickiness during the COVID crisis

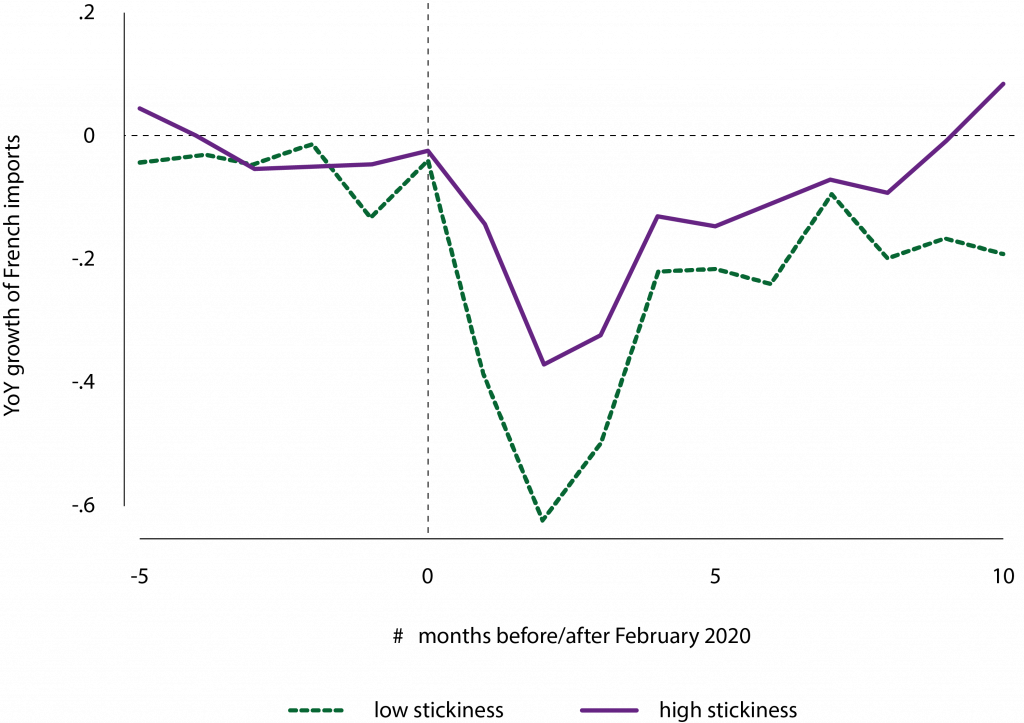

While in Martin et al (2023) we focus on uncertainty episodes, delving into the microeconomic underpinning of other crisis episodes can enhance our understanding of dynamic trade patterns. Figure 3 thus digs into the trade collapse around the COVID crisis.

Figure 3. Year-on-year growth of French imports

Note: Sticky products are products in the top quartile of the distribution of our index. The least sticky products are in the bottom quartile.

Source: Martin et al (2023).

The figure contrasts the evolution of French imports between high-stickiness and low-stickiness products at the end of 2019 and in 2020. It appears that product markets with a higher degree of stickiness experienced a milder impact from the trade collapse in March and April 2020.

This observation is largely attributed to the fact that the trade downturn was more pronounced in less sticky product markets. Further analysis reveals that the bulk of this has been driven by the extensive margin, ie. a drop in the number of bilateral import flows within a firm.

Whereas such descriptive evidence is by no means indicative of the specific mechanism behind this pattern, it illustrates how our index can be used to shed light on unexplored facets of trade flows.

Using relationship stickiness to refine the measures of trade dependencies

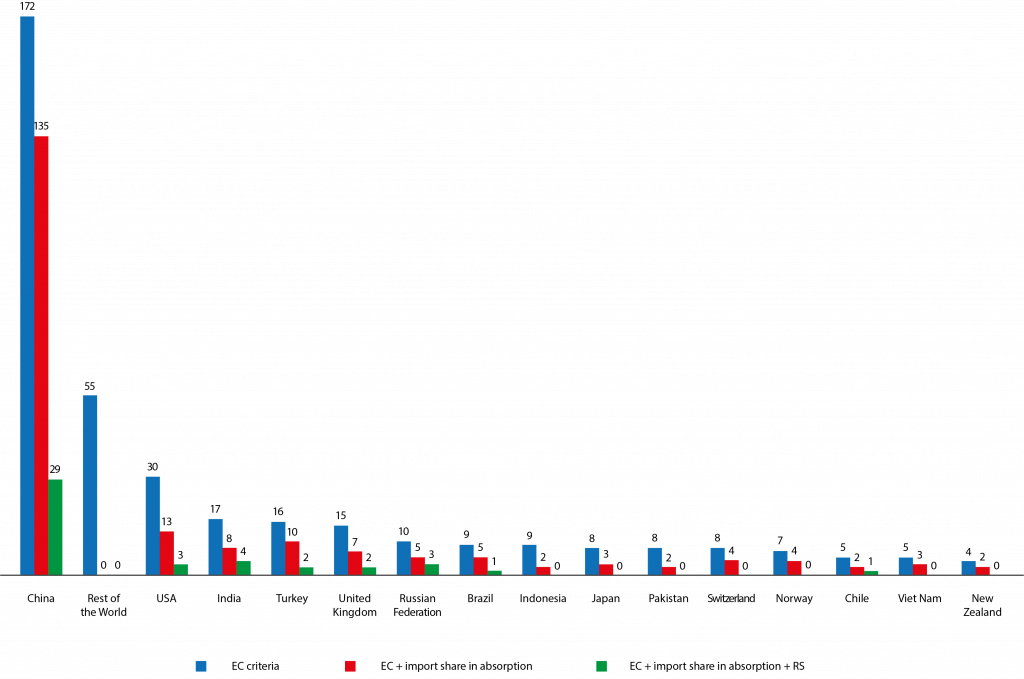

In a recent paper, Mejean and Rousseaux (2023) finally used the relationship stickiness index to identify trade dependencies exposing the EU to potential disruptions. The literature has proposed various heuristic measures to assess vulnerability associated with trade.

The European Commission (2021) thus identifies trade dependencies by the structure of global trade. Products imported from a limited number of producing countries are considered more vulnerable to trade shocks, especially when domestic absorption heavily relies on foreign producers. Applying these criteria to the EU context, the authors identify 228 products as potentially vulnerable to shocks.

Relationship stickiness can be used to refine the diagnosis of vulnerability. Traditional criteria used in the literature focus on the ex-ante structure of trade and production, which may offer limited diversification opportunities when concentrated on a small number of producing countries.

The degree of relationship stickiness serves as a complementary indicator regarding the possibility of ex-post diversification. Trade disruptions in concentrated product markets are likely to be particularly costly if the product also displays a high degree of stickiness. Adding this criterion restricts the list to 48 vulnerable products. As shown in Figure 4, a disproportionate share of these products is sourced from China.

Figure 4. Comparison of the geographical distribution of three lists of strategic dependencies

Note: The figure illustrates the geographical distribution of identified strategic dependencies, using the European Commission methodology (blue bars), the strategy augmented with an absorption criterion (red bars) and the list that further incorporates the stickiness indicator (green bars).

Source: Mejean and Rousseaux (2023).

Conclusion

The literature on global value chains has consistently highlighted multiple contractual frictions that contribute to a significant level of stickiness in trade partnerships. This stickiness is anticipated to influence the resilience of international trade ties, the adjustments of trade flows, and the scope and design of de-risking strategies.

Consequently, it is crucial to measure relationship stickiness in trade data. We propose such a measure that is available on our websites.

References

Antràs, P and D Chor (2013), “Organizing the Global Value Chain”, Econometrica 81(6): 2127–2204.

Antràs, P and E Helpman (2004), “Global Sourcing”, Journal of Political Economy 112(3): 552–580.

Baldwin, R and R Freeman (2022), “Risks and Global Supply Chains: What We Know and What We Need to Know”, Annual Review of Economics 14: 153-180.

Baldwin, R, R Freeman and A Theodorakopoulos (2023), “Supply chain disruptions: Shocks, links, and hidden exposure”, VoxEU.org, 29 November.

European Commission (2021), “Strategic dependencies and capacities”, Commission Staff Working Document, May.

Head, K and J Ries (2008), “FDI as an outcome of the market for corporate control: Theory and evidence”, Journal of International Economics 74(1): 2–20.

Martin, J, I Mejean, and M Parenti (2023), “Relationship Stickiness, International Trade, and Economic Uncertainty”, The Review of Economics and Statistics, forthcoming.

Mejean, I and P Rousseaux (2023), “Identifying European trade dependencies”, mimeo.

This article was originally published on VoxEU.org.