Seizing leadership in the net zero economy

Linda Kalcher and Neil Makaroff are respectively Executive Director and Director of Strategic Perspectives

The European Union stands at a pivotal juncture in its industrial history. As the continent prepares to advance its economic trajectory through the next phase of the European Green Deal, it faces a critical question: Will it lead the charge in the green economy or trail behind its global competitors in the US and China?

The European Green Deal as a basis for modernisation

The initial phase of the Green Deal helped Europe navigate through the aftermath of COVID-19 and the energy insecurities following Russia’s war on Ukraine. The policies adopted in the last five years are delivering results: renewable deployment is booming at an unprecedented scale.

In 2023, a total of 56 gigawatts (GW) of solar and 17 GW of wind capacity were added, marking an unprecedented pace of renewable deployment. For the first time, wind power generation surpassed gas power, significantly enhancing energy security and reducing reliance on imported fuels.

Progress is also evident with electric vehicles (EVs) and heat pumps, leading to the emergence of new industries and jobs. The Hauts-de-France region, for example, is becoming a significant battery manufacturing hub, generating 20,000 jobs and contributing to the EU’s goal of producing 90% of its batteries domestically by 2030.

Similarly, the regions of Silesia, northern Czechia and Slovakia are emerging as significant centres for heat pump manufacturing, which is crucial for reducing dependency on imported heat pumps and revitalising local economies. These regions are witnessing job creation and investment inflows that are setting a template for others to follow.

The European Green Deal is not just an environmental or energy initiative; it is a comprehensive modernisation agenda with concrete results: it has laid a robust foundation for Europe’s energy transition, cutting imports of oil and gas by one third by 2030 and making electricity more affordable.

The 27 EU countries are achieving significant milestones in renewable energy deployment, enhancing energy security by cutting fossil fuel imports, and delivering socio-economic benefits. These early successes are setting the stage for a prosperous and competitive future for the EU – but the job is not done yet.

EU risks falling behind in the global race to net zero

As the world moves faster towards a climate neutral future, Europe finds itself at risk of falling behind. China’s dominance in the production of key net zero technologies is evident, with 60% of mass production in strategic areas like solar photovoltaics and EV batteries controlled by China. 25% of electric vehicles and batteries and more than 90% of solar panels sold in Europe are imported from China.

China pursues this out of economic and security interests, aiming to supply global markets. The United States is trying to catch up by rapidly scaling up its EV production through the Inflation Reduction Act (IRA). Meanwhile, energy prices in Europe are twice as high compared with China and the US, another impact on the competitiveness of the EU’s industry.

The need for a holistic industrial strategy

To remain competitive, Europe needs a modern, holistic industrial strategy that combines decarbonisation goals with reindustrialisation. Such a strategy would ensure that Europe does not remain a passive consumer of imported zero-carbon technologies but rather, becomes a powerhouse of industrial innovation. Key components of this European industrial strategy should include:

Investing in a manufacturing base and creating jobs: building a robust manufacturing base is essential to ensuring the production of key net zero technologies within Europe. This investment will create millions of new jobs in the net zero industry, providing economic security and fostering regional development.

Using the single market with standards and creating lead markets: the next few years are key to leveraging the power of the single market through the implementation of stringent standards and lead markets for green products. This will encourage the use of domestically-produced clean technologies and materials, driving demand and investment in European-made products.

Decarbonising the existing industry: transforming the current industrial base to adopt low-carbon technologies is crucial. This involves producing green steel, chemical and glass, increasing energy efficiency and promoting the use of renewable energy sources. Decarbonising existing industries will reduce reliance on fossil fuels, enhance resilience to energy price volatility and ensure long-term competitiveness in the global market.

Such a comprehensive industrial strategy will not only help Europe catch up in the global race for zero-carbon technologies but also establish it as a leader in clean industrial practices.

Long-term vision as the compass for action

Defining the direction starts with the 90% climate target as proposed by the European Commission. This target is the cornerstone of a European Industrial Strategy, planning the decarbonisation of the economic base and identifying necessary net zero industries.

Strategic Perspectives’ latest report, Forging Economic Security and Cohesion in the EU (2024), shows that cutting net greenhouse gas emissions by 90% by 2040 addresses environmental concerns and drives economic and industrial transformation. Key to this goal is shifting to renewable energy, with plans to electrify half of the EU economy, decarbonise the electricity sector by 2037, phase-out coal by 2030 and achieve 80% renewable electricity by 2040, requiring 70 GW of new renewable capacity annually.

The economic and security benefits of reaching the 2040 climate target are substantial. By 2035, decarbonising the power sector is expected to reduce electricity prices by 12% and household energy bills by two-thirds, potentially saving European households approximately €449 billion by 2040.

This transition will enhance the competitiveness of European industries while also strengthening the EU’s energy independence and reducing its exposure to fossil fuel price volatility and geopolitical risks. The projected savings of up to €856 billion in fossil fuel imports between 2025 and 2040 underscore the economic advantages of this shift.

A comprehensive European Industrial Strategy is essential to complement the Green Deal. It can integrate political commitment, adequate funding and targeted investments to modernise the industrial base. This strategy can create a unified European value chain, support reindustrialisation in transitioning regions and generate new jobs in net zero industries by 2040. This approach can ensure the EU’s competitiveness globally and enhance economic resilience and cohesion across member states.

The time for decisive action is now; Europe must not hesitate. Investment cycles of companies are 10-15 years, so decisions taken in the next five years are vital for competitiveness and the path to climate neutrality

Investing in building net zero industries and value chains

Europe has maintained a strong share in wind power manufacturing and heat pumps, with domestic production covering 85% and 73% of market demand, respectively.

However, the European wind industry faces challenges due to value chain disruptions and inflation, leading to job losses and a weakened business case.

A European Industrial Strategy is an opportunity to also create net zero value chains. For example, currently, lithium extracted in Portugal is exported to China to be refined and then imported back in Europe in the form of a battery.

A pan-European Industrial Strategy would enable strategic partnerships across the continent, such as linking France’s burgeoning battery industry with lithium resources in Portugal and manufacturing capabilities in Spain. These alliances are crucial for developing a resilient and integrated European supply chain, from the material to the technology and recycling.

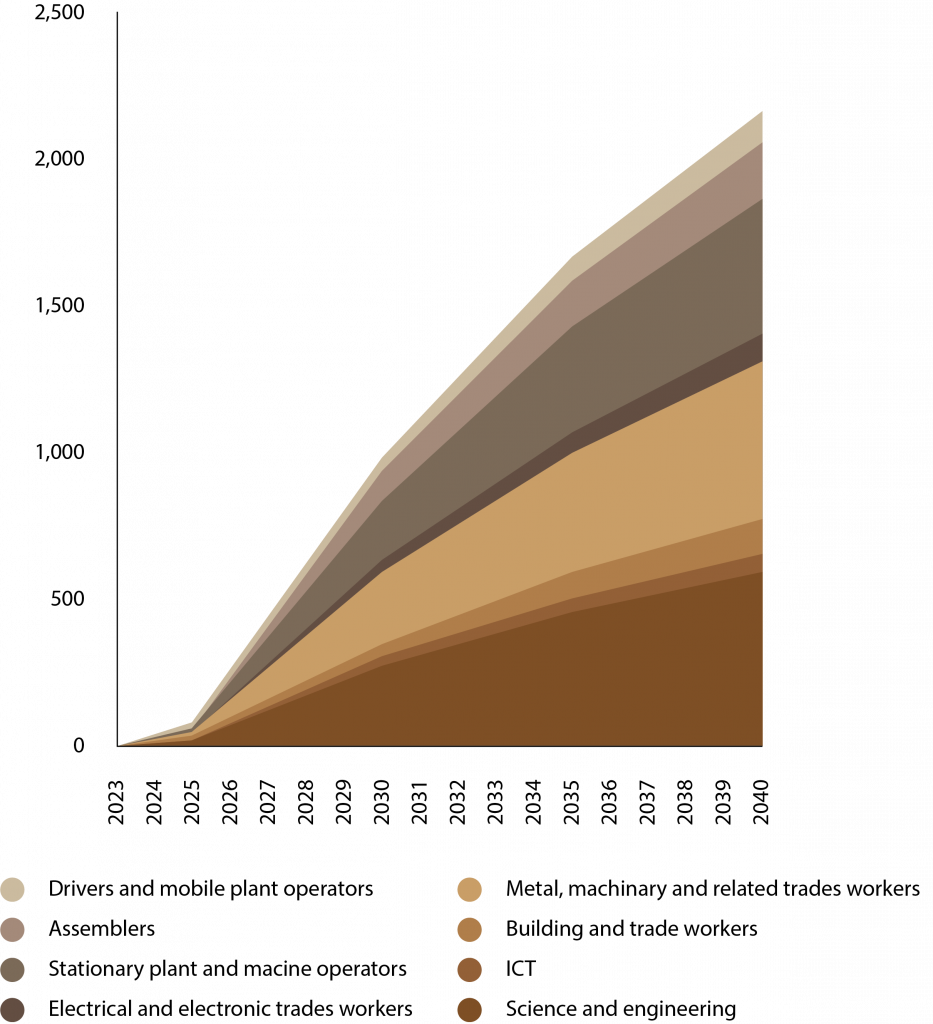

This has the potential to reindustrialise regions and create additional jobs. Our latest report shows that, with a European Industrial Strategy, 1.6 million additional green jobs can be created in manufacturing by 2035, with a total of 2.1 million by 2040.

This reindustrialisation can help regions in transition, such as those affected by the decline of traditional industries, by providing new economic opportunities and employment security.

Figure 1. New jobs created in the net zero industry under an industrial strategy (in thousands of jobs)

A single market fitted to net zero to support the demand

To support the demand for net zero technologies and materials, the EU could adapt its single market by setting high standards, creating lead markets and leveraging public procurement. These measures aim to reduce dependence on technology and fossil fuel imports, ensuring a resilient supply chain and fostering economic security.

Establishing rigorous standards and creating lead markets is crucial for competitiveness. By defining ‘green’ materials and setting quotas, ie. for green steel in key industries such as automotive and wind power, the EU can enhance innovation and predictability for manufacturers. This approach supports early adoption of green practices and drives the transition to a net zero economy.

Public procurement plays a pivotal role in boosting the market for EU-made green products. Including sustainability criteria in public tenders can drive demand for innovative technologies. With over 14% of gross domestic product (GDP), public procurement helps industries adopt new standards early, supporting local manufacturers and aligning public spending with environmental goals. Enhancing domestic manufacturing and the circular economy could save the EU billions annually in technology and material imports by 2040.

Abundant and affordable zero-emissions electricity to strengthen competitiveness

The ongoing energy crisis exacerbated by geopolitical tensions underscores the importance of energy security. The EU imported €640 billion in fossil fuels in 2022, and approximately €375 billion in 2023, even with reduced prices. Energy prices remain a critical issue, being significantly higher in Europe compared to China and the US, which pressures businesses alike.

Achieving abundant and affordable zero-emission electricity is crucial for strengthening Europe’s competitiveness. The EU’s current dependence on fossil fuels makes its economy vulnerable to price shocks. Electrifying the industry is essential to make it less vulnerable to international energy markets and restore competitiveness with China and the US.

Investments to make Europe’s industry thrive

To prevent deepening economic disparities and a fragmented single market, it is crucial to avoid a two-speed Europe where some countries advance faster than others due to differing fiscal capacities.

A new financial architecture should incorporate better coordination of national investments and the establishment of a European Green Deal Investment Fund that also strengthens cohesion. This fund would facilitate common investments into the transition, particularly in countries with more fiscal constraints.

This approach is especially important as the end of the NextGenerationEU program will reduce European investments in climate action by €35 billion per year from 2026.

By fostering a unified approach and ensuring all regions can remain prosperous and competitive, the EU can maintain cohesion and economic security while achieving its climate goals. To help Europe’s industry thrive, substantial investments are necessary.

Our report highlights that cumulative investments of €668 billion between 2023 and 2040 could generate €233 billion of new economic activity in industrial sectors, boosting the productivity of the economy by 10%. This new financial architecture should include better coordination of national investments and the establishment of a European Green Deal Investment Fund to support common investments into the transition, especially in countries with more fiscal constraints.

By ensuring a unified and pragmatic investment strategy, the EU can prevent a fragmented market, promote balanced economic growth and achieve its ambitious climate targets.

Europe’s path forward

Europe has the resources, the expertise and the economic framework to lead the world in zero-carbon technology and industrial innovation. By investing in a strategic, continent-wide industrial overhaul, Europe can secure a prosperous future and establish itself as a leader in the global zero-carbon economy. The time for decisive action is now; Europe must not hesitate. Investment cycles of companies are 10-15 years, so decisions taken in the next five years are vital for competitiveness and the path to climate neutrality. The upcoming EU elections and strategic decisions from EU institutions will determine whether Europe leads or lags in the global shift towards a zero-carbon future.