COVID-19 and GVCs

Laura Lebastard is an Economist at the European Central Bank, Marco Matani is a Consultant at Halle Institute for Economic Research, and Roberta Serafini is the Principal Economist at the ECB

COVID-19 triggered a debate on whether supply value chain trade is primarily a source of vulnerability or a source of resilience. This column uses data on French firms over the period January 2020 to December 2021 to show that participation in global value chains increased firms’ vulnerability to the pandemic shock in terms of both export sales and probability of survival in the export market – especially when supply bottlenecks were more salient.

Firms located relatively more downstream in the value chain were more severely affected by supply disruptions. At the same time, the results suggest that exporting firms benefited from sourcing their core inputs from different countries, supporting the hypothesis that diversification in global value chains fosters supply chain resilience.

The outbreak of the COVID-19 pandemic resulted in a sharp contraction in both demand and supply, driven by lockdown measures adopted in many countries across the globe in response to the severity of the contagion and its geographical spread.

The global nature of the crisis meant that firms engaged in international trade were exposed to international disruptions on top of domestic ones, with weaker foreign demand for exporting firms, and a reduction in supply translating into shortages of intermediate inputs for importing firms.

Firms involved in global value chains (GVCs) – namely, firms that both import intermediate inputs and export goods – faced these two additional challenges to their ability to produce and therefore sell their goods (Baldwin and Tomiura 2020).

In this context, the further upstream the disruption occurs, the greater is the potential for supply bottlenecks to propagate negative shocks. Thus, the COVID-19 pandemic has triggered a debate among academics and policymakers on whether supply value chain trade is primarily a source of vulnerability or a source of resilience (Mirodout 2020, Baldwin and Freeman 2022).

In our recent paper (Lebastard et al 2023), we exploit rich customs data covering all French firms engaged in international trade to estimate the impact of supply chain linkages on exporting activity during the pandemic1.

The monthly frequency of the data allows us to differentiate between three periods during the unfolding of the COVID-19 crisis. The first phase was between February and April 2020, when lockdowns caused activity to come to an abrupt halt in a number of non-essential manufacturing and services sectors.

The second phase was between May and August 2020, when exports recovered to some extent in response to the gradual lifting of pandemic-related restrictions.

The third phase was from September 2020 to the end of 2021, when disruptions to global supply chains emerged and progressively intensified. We focus on all firms that had exported every month between July and December 2019.

Within this sample, our treatment group comprises all exporting firms that had imported intermediate inputs at least once over the same period. We assess firms’ performance during the crisis, in terms of export sales and probability of survival in the export market. The richness of the dataset allows us to then deepen our analysis and look at several sources of heterogeneity.

In particular, we investigate the extent to which the pandemic had a differential impact depending on whether firms are located more upstream or downstream along the value chain and on whether they diversify the countries from which they source their inputs.

Firms in global value chains: comparing the COVID-19 crisis and the great financial crisis

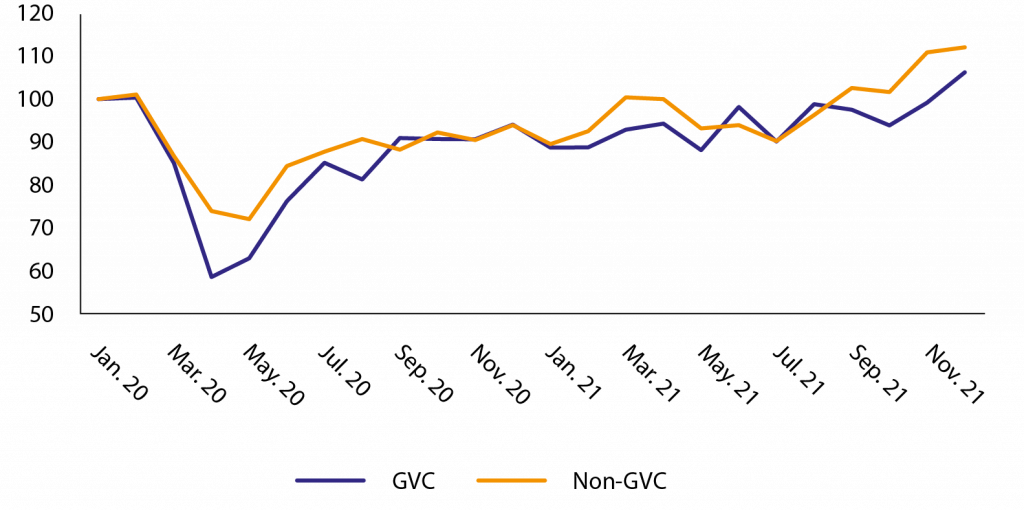

Our data show that firms involved in global production networks in the pre-crisis period experienced the sharpest fall in exports at the onset of the COVID-19 crisis, and recovered at a slower pace than non-GVC exporters after the economic reopening (Figure 1, panel a).

In April 2020 GVC exporters recorded export volumes that were 42% lower than the levels recorded in January 2020. For non-GVC exporters, the cumulative decline was less drastic, reaching a trough in May 2020 at 28% below the level recorded in January 2020.

The two groups diverged further when the pandemic-related restrictions were lifted in the summer of 2020 and when the recovery took shape over the following year. By March 2021 nominal exports of firms not involved in global value chains had reached their January 2020 levels and by September 2021 they had recovered well beyond their pre-pandemic levels, while it took until December 2021 for GVC firms to exceed their January 2020 export levels.

Figure 1. Export performance over time of GVC firms and non-GVC firms

a) COVID-19 crisis (total exports, January 2020 = 100)

b) Global financial crisis (total exports, August 2008 = 100)

Notes: The charts are based on firm-level data for France. We only include firms that exported every month in the pre-crisis period. GVC firms are included if they imported at least once during the six months before the crisis.

Sources: Direction générale des douanes et droits indirects and authors’ own calculations.

Interestingly, during the 2008 global financial crisis the situation was reversed (Figure 1, panel b), with GVC firms recording much smaller reductions in their nominal exports than their non-GVC counterparts. Compared with August 2008, nominal exports of GVC firms had fallen by 19% in August 2009, while exports of similar non-GVC firms had fallen by a quarter at their lowest point in May 2009.

In comparison with the COVID-19 crisis, the collapse in trade in 2008 was less sizeable and less abrupt, although it was more persistent for both types of firm, suggesting that whether supply value chain trade is mainly a source of vulnerability or a source of resilience ultimately depends on the nature of the crisis.

The pandemic had a relatively greater impact on GVC firms’ exports, especially when supply disruptions intensified

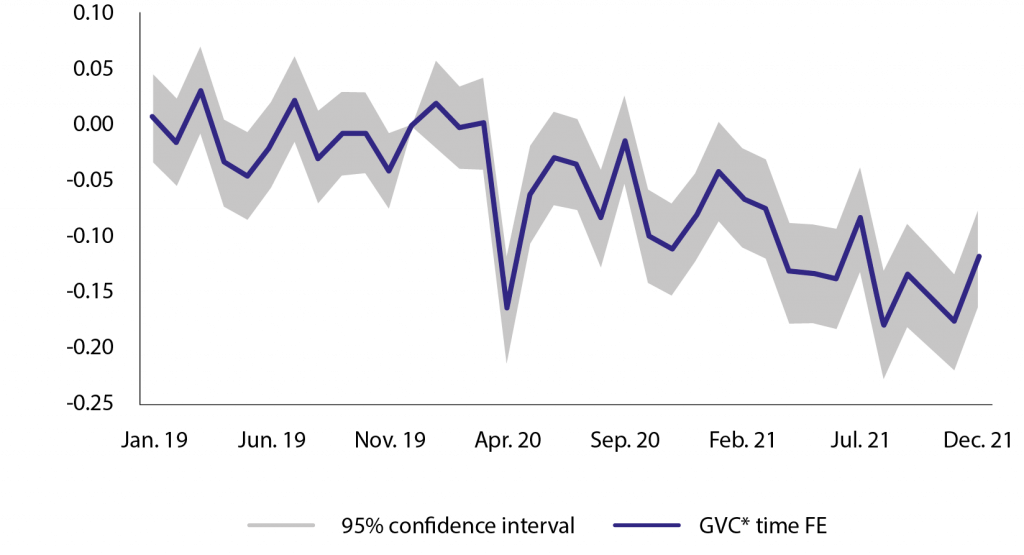

Figure 2 illustrates the estimated effect of participation in global value chains on firm-level exports. Our treatment group includes all continuous exporters that had imported at least once between July and December 2019; the control group is the remaining exporting firms in the dataset, ie. those that did not import over that period.

Our results point to the emergence in April and May 2020 of the first negative and significant effect of being part of a global value chain during the pandemic, and a new more sizeable and persistent decline in exports starting in October 20202.

Estimates from a difference-in-differences model show that indeed over the latter period exports by non-GVC firms benefited from the pent-up demand and accumulated savings, while those of GVC firms remained constrained owing to protracted unavailability of imported inputs3.

Figure 2. Event study, effect of the pandemic on GVC firms’ exports

Notes: The estimated effect is computed as in Lebastard et al (2023), where the dependent variable is the natural logarithm of exports. The treatment group comprises all exporting firms involved in global value chains (GVCi is equal to 1 if the firm imported at least once in the six months immediately before the crisis) while the control group comprises the other continuous exporters. The econometric model controls for the size of the firms by including firm fixed effects and for time-specific shocks using time fixed effects (FE). The reference month is December 2019.

Sources: Direction générale des douanes et droits indirects and authors’ own calculations.

Additional evidence shows that firm survival followed a similar trend to that observed for exports, pointing to a greater discontinuity of trade flows for GVC firms.

Firms further downstream hit the hardest

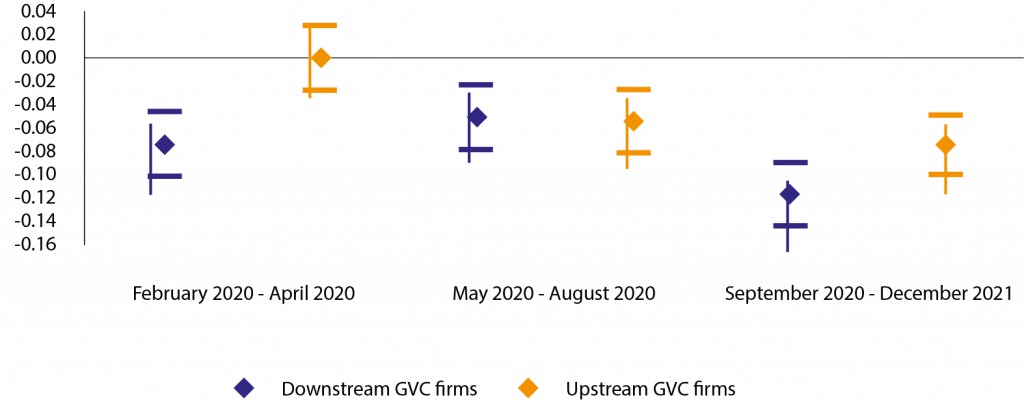

We exploit the richness of the dataset to deepen our analysis and assess whether the negative impact of GVC participation on export performance differed depending on firms’ position along the value chain.

In particular, based on Antràs et al (2012) we use the latest OECD Input-Output Tables to compute an index of upstreamness of production for 45 sectors. We then combine this measure of industry-level upstreamness with product-level information on firm trade flows following Chor et al (2021), computing for each firm an average of the respective index of import and export upstreamness.

We find that participation in GVCs increased firm vulnerability during the pandemic, with the negative impact of supply disruptions being greater for firms located relatively more downstream in the value chain. In particular, GVC firms in the lower half of the index distribution saw their exports decrease by about 8% compared with non-GVC exporters during the lockdown, while the remaining – more upstream – GVC firms did not have significantly worse export performances than non-GVC firms (Figure 3).

Both upstream and downstream GVC firms were strongly negatively affected during the period from September 2020 to December 2021, when disruptions along value chains were at historically high levels, although downstream firms were most affected.

Figure 3. Difference-in-differences, effect of being downstream or upstream

Notes: For the basis of the the coefficient estimates, see Lebastard et al (2023).

Sources: Direction générale des douanes et droits indirects and authors’ own calculations.

The fact that downstream firms were hit harder would seem to confirm that, although negative shocks occurred in both demand and supply during the pandemic, supply shocks were indeed predominant.

In this respect, the COVID-19 crisis differed from the global financial crisis, which was mainly a result of a demand shock propagating up the value chain via adjustments of firms’ inventory holdings (the so-called bullwhip effect, as in Altomonte et al 2012).

More diversified sourcing networks for core imported inputs partially shielded firms from shocks

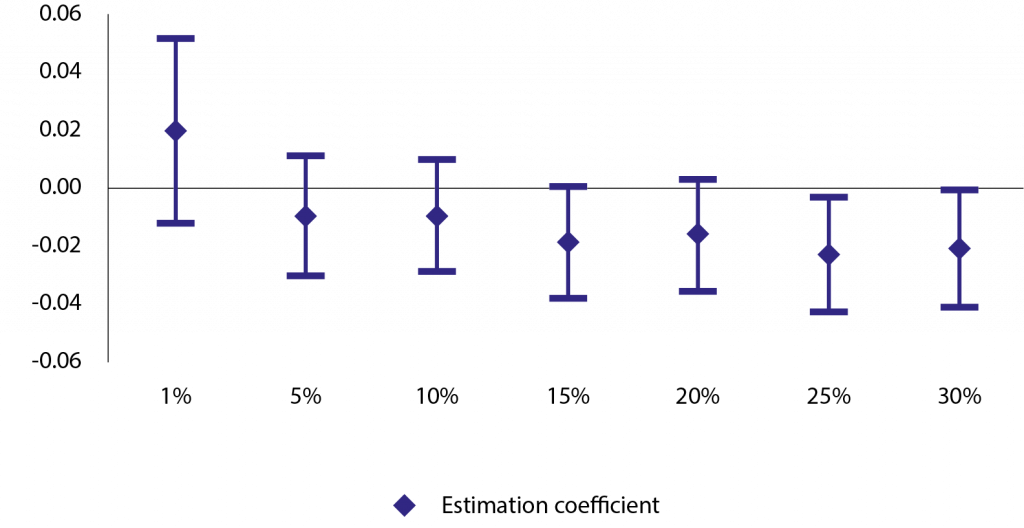

The pandemic has raised the question of whether diversification would foster supply chain resilience and therefore help reduce countries’ vulnerability to future external shocks. We try to shed some light on this by estimating the effect of diversification of imports among GVC firms on their export performance.

We follow the approach in Lafrogne-Joussier et al (2022), where a firm is considered as diversifying its GVC involvement whenever its ‘core’ imported products (ie. representing at least 1% of its imports before the pandemic) are sourced from at least two countries.

In our study, however, we test the effect of diversification by allowing the threshold for a product to be identified as ‘core’ to vary between 1% and 30% of total imports between July and December 2019.

Our results, as shown in Figure 4 below, suggest that exports of GVC firms suffered from the lack of diversification for products representing more than 15% of total imports.

Figure 4. Difference-in-differences, effect of diversification of source countries for core inputs

Notes: For the basis of the coefficient estimates, see Lebastard et al (2023). Core products are defined as products representing a minimum percentage (as indicated on the x-axis) of the total imported products in the six months before the crisis.

Sources: Direction générale des douanes et droits indirects and authors’ own calculations.

Conclusions

In this column we investigate the impact of supply chain linkages on exporting firms during the pandemic. Highly granular data for the universe of French exporters allow us to provide one of the first firm-level quantifications of the impact of supply bottlenecks that occurred in 2021, when disruptions along value chains were at historically high levels.

We find that exporters in global value chains suffered relatively more than other exporters during the COVID-19 crisis. This was the case both in terms of export losses and in terms of the greater likelihood of discontinuity in export relations, particularly when supply disruptions were at historically high levels.

This additional negative effect was mostly driven by exporters at downstream production stages, whereas diversifying sourcing networks for core imports helped to buffer the impact.

Endnotes

1. Our analysis is based on French customs data, known as “Statistiques du Commerce Extérieur”, provided by Direction générale des douanes et droits indirects; access to firm-level confidential data from France has been made possible within a secure environment offered by CASD – Centre d’accès sécurisé aux données (Ref. 10.34724/CASD).

2. The absence of any pre-trend before the pandemic confirms the comparability of our treatment group and control group.

3. As detailed in Lebastard et al. (2023), our results prove robust to a number of robustness checks, including more stringent criteria for GVC involvement.

References

Altomonte, C, F di Mauro, G Ottaviano, A Rungi and V Vicard (2012), “Global Value Chains are not all born identical: Policymakers beware”, VoxEU.org, 4 January.

Antràs, P, D Chor, T Fally and R Hillberry (2012), “Measuring the Upstreamness of Production and Trade Flows”, American Economic Review 102(3): 412–16.

Baldwin, R and E Tomiura (2020), “Thinking ahead about the trade impact of covid-19”, Chapter 5 in Economics in the Time of COVID-19, CEPR Press.

Baldwin, R and R Freeman (2022), “Global supply chain risk and resilience”, VoxEU.org, 6 April.

Chor, D, K Manova and Z Yu (2021), “Growing like China: Firm performance and global production line position”, Journal of International Economics 130.

Lafrogne-Joussier, R, J Martin and I Mejean (2022), “Supply Shocks in Supply Chains: Evidence from the Early Lockdown in China”, IMF Economic Review 4.

Lebastard, L, M Matani and R Serafini (2023), “GVC exporter performance during the COVID-19 pandemic: the role of supply bottlenecks”, ECB Working Paper Series No. 2766, January.

Mirodout, S (2020), “Resilience versus robustness in global value chains: Some policy implications”, VoxEU.org, 18 June.

Authors’ Note: This column first appeared as a Research Bulletin of the European Central Bank. The author gratefully acknowledges the comments from Alexander Popov. The views expressed here are those of the author and do not necessarily represent the views of the European Central Bank or the Eurosystem. This article was originally published on VoxEU.org.