Decarbonisation of the energy system

Georg Zachmann is a Senior Fellow at Bruegel, Franziska Holz and Claudia Kemfert are respectively the Deputy Head of Department and Head of Department at DIW Berlin, Ben McWilliams is a Research Analyst at Bruegel, Frank Meissner, Alexander Roth and Robin Sogalla are respectively a Consultant and Researchers at DIW Berlin

Summary

Three quarters of the European Union’s greenhouse gas emissions stem from burning coal, oil and natural gas to produce energy services, including heating for buildings, transportation and operation of machinery. The transition to climate neutrality means these services must be provided without associated emissions.

It is not possible today to determine tomorrow’s optimal clean energy system, largely because the cost, limitations and capability developments of competing technologies cannot be predicted. Energy systems with widely diverging shares of ‘green fuels’, in the form of electricity, hydrogen and synthetic hydrocarbons, remain conceivable.

We find the overall cost of these systems to be of the same order of magnitude, but they involve larger investments at different stages of value chains. A large share of synthetic hydrocarbons would require more investment outside the EU, but less in domestic infrastructure and demand-side appliances, while electrification requires large investment in domestic infrastructure and appliances.

Current projections show an overall cost advantage for direct electrification, but projections will evolve and critical players may push hard for alternative fuels. Policy will thus play a major role in shaping this balance.

Political decisions should, first, push out carbon-emitting technology, primarily through carbon pricing. The more credible and predictable this strategy is over the coming decades, the smoother will be both divestment from brown technologies and investment in green technologies.

Second, policy needs to help ensure that enough climate-neutral alternatives are available in time. Clear public support should be given to three system decisions about which we are sufficiently confident: the massive roll-out of renewable electricity generation; the electrification of significant shares of final energy consumption; and rapid phase-out of coal from electricity generation.

For energy services where no dominant system has yet emerged, policy should forcefully explore different solutions by supporting technological and regulatory experimentation.

Given the size and urgency of the transition, the current knowledge infrastructure in Europe is insufficient. Data on the current and projected state of the energy system remains inconsistent, either published in different places or not at all. This impedes the societal discussion.

The transition to climate neutrality in Europe and elsewhere will be unnecessarily expensive without a knowledge infrastructure that allows society to learn which technologies, systems, and polices work best under which circumstances.

1 Introduction

For the European Union to become the first climate-neutral continent by 2050, the decarbonisation of the energy sector will be crucial. Production and use of energy accounts currently for more than three quarters of the EU’s greenhouse gas emissions1, and most of the EU energy system still relies on the combustion of oil, natural gas and coal.

Meanwhile, the potential to reduce demand for energy services is most likely limited and therefore most energy services currently based on fossil-fuels need to be replaced by climate-neutral alternatives. One of the open issues is the relative role of different non-fossil fuels2 – primarily electricity, hydrogen and synthetic methane – in final energy use.

We present three extreme scenarios to highlight the consequences of different energy-policy choices: first, the full electrification of the economy; second, the widespread use of hydrogen; and third, widespread use of synthetic methane. In practice, a combination of the three scenarios is most likely to be implemented, and the three scenarios are not equally probable.

Irrespective of the choices made, we emphasise three main ‘no-regret’ policies that should in any case be implemented3: (a) rapid deployment of more renewable electricity generation, (b) electrification of significant shares of final energy uses (such as heating and transportation), and (c) the swift phase-out of coal.

Our analysis also highlights that the current national energy and climate plans (NECPs) of EU countries are insufficient to achieve a cost-efficient pathway to EU-wide climate neutrality by 2050. Consequently, a strong commitment frame- work is needed to ensure that NECPs are aligned with European targets.

Political decisions, particularly on agreements with third countries for the future import of green fuels, act as commitment devices

2 Different scenarios

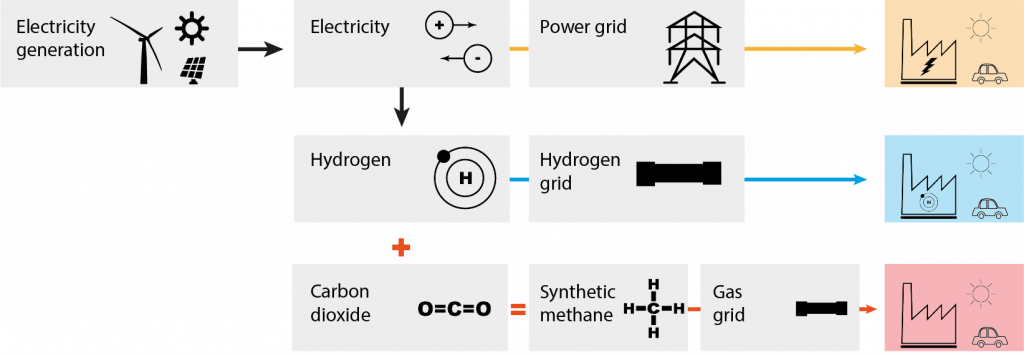

How the European energy system will develop over the next decades is highly uncertain. In particular, the roles in the future energy mix of hydrogen (H2), synthetic methane (CH4) and their derivate products (such as ammonia) remain hard to predict. These fuels can be produced using renewable electricity (and/or biomass). On this basis, they are referred to as ‘green’.

Hydrogen can be produced from electrolysis of water (Figure 1). Synthetic methane can then be produced via an additional electrochemical process known as the methanation of hydrogen. In this process, hydrogen and carbon dioxide are used as inputs (Götz et al 2016).

If the inputs are ’clean’ over their lifetime – for example, hydrogen obtained from electrolysis using renewable electricity, and CO2 captured from the atmosphere – the final product is considered greenhouse-gas-neutral. The additional methanation process makes synthetic methane more electricity-intensive and expensive than hydrogen (Evangelopoulou et al 2019).

Alternatively, synthetic methane can be produced from biogenic sources, ie. by increasing the methane concentration in biogas to almost 100 percent, but the potential for biogas production in the EU is rather limited4. The resulting synthetic methane might replace fossil natural gas, which is also almost pure methane.

Figure 1. Simplified overview of a low-carbon energy system

Source: Bruegel.

The main advantage of synthetic methane is that it can be fed into the existing natural gas transportation and storage infrastructure. Furthermore, it requires less investment on the demand side than hydrogen or direct electrification, since current natural gas heating systems or turbines could be fuelled with synthetic methane in the future.

However, beyond this initial capital stock advantage, synthetic methane appears significantly less attractive than hydrogen or direct electrification. There would be high investment costs for production facilities5, and substantial amounts of electricity required to run them, because of the poor overall energy efficiency6.

The energy efficiency of hydrogen produced from a unit input of renewable electricity is higher. However, hydrogen cannot be pumped through existing natural gas pipelines, which would need to be retrofitted to transport hydrogen safely.

Our three scenarios illustrate the uncertainty around the future energy system and find robust, no-regret developments that appear in all scenarios. We assume a plausible level of energy demand in 2050 and make extreme assumptions about the contribution of each of the three fuels to meeting this demand.

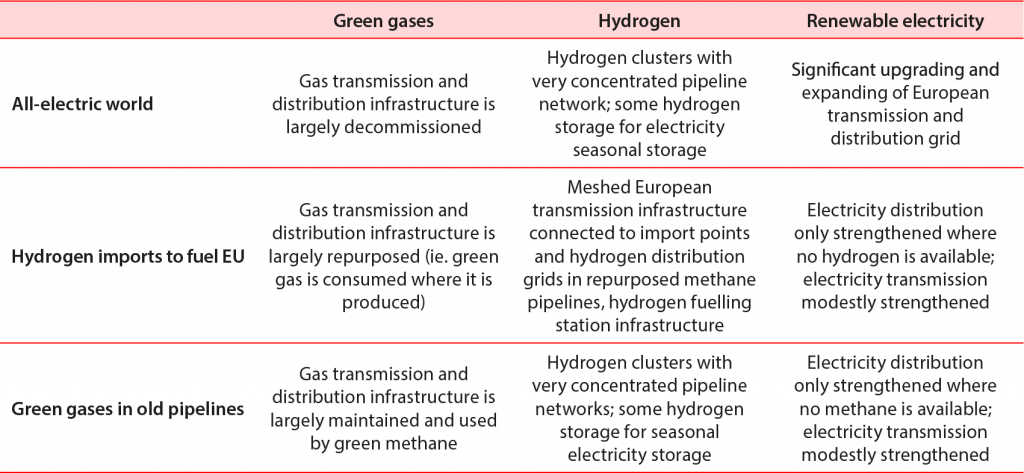

We distinguish: a) an ‘all-electric world’; b) a hydrogen-dominated world in which hydrogen demand is so great that hydrogen imports are required; and c) a ‘green gases’ world, in which synthetic methane plays a major role as a replacement for natural gas.

All scenarios rely on extensive electrification of energy supply and demand, and a phase-out of coal and fossil natural gas.

Table 1. Scenario assumptions

Source: Bruegel.

We assess the future energy system in 2030 and 2050 according to these three scenarios. We assume the same useful energy demand in all scenarios, but this demand would be satisfied with different technologies and from different sources (Box 1).

In addition, the role of energy imports varies across the scenarios; domestic energy demand is met from a mix of domestic renewable energy generation and imported fuels. In the scenarios focussing on transition to hydrogen and synthetic methane, energy imports would meet a large share of demand. This implies less demand for electricity generation domestically which is off-shored via production of these fuels abroad (Figure 2).

Box 1. Scenario analysis methodology

For each scenario, we calculated the required investments (2020-2030, 2030-2050) in the energy sector, ie. additional power generation capacities, investments in electrolyser and transmission grids, and investments in hydrogen grids – but not the cost of demand-side appliances. It is impossible to have a clear ordering of the cost of appliances that serve the same purposes but use different fuels. The corresponding energy system investment unit costs are taken from the ASSET project (Capros et al 2018). The investment volumes in the different scenarios are calculated based on the assumption that the amount of useful energy required in each sector is the same as that implied in the MIX-55 scenario results developed by E3Modelling (JRC, 2021). ‘Useful’ energy is the energy service finally made available to users (kilometres driven, square metres heated). As more efficient fuel systems (electricity) require less kWh of input to provide the same service (heating) than less efficient systems (hydrogen), a smaller system is required to provide the same service. For each major final use, we estimated for each fuel the required input. For each scenario, we estimated the share of each fuel in each use type. Based on this, we calculated required inputs of the different fuels for each sector and in total. This allowed us to calculate the necessary transmission and generation capacities. Ultimately, these capacities can be translated into investment figures.

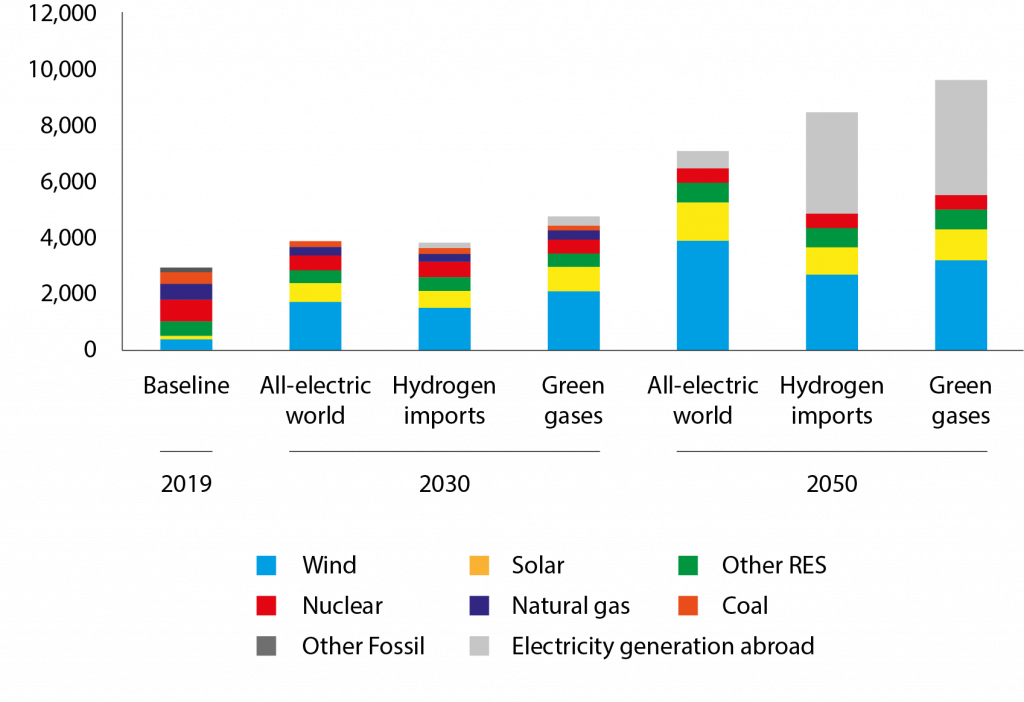

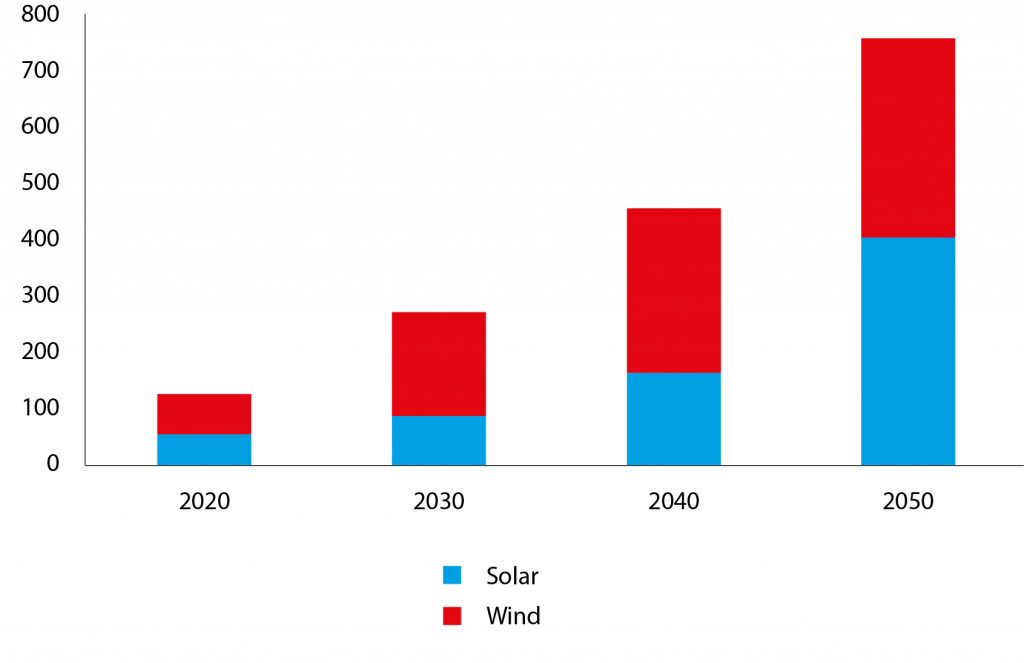

More importantly, a major increase in renewable electricity generation in the EU is required to achieve the emissions reductions from the energy sector. Figure 2 shows that electricity generation levels must at least double by 2050 compared to today (with potential deployment abroad in the case of energy imports).

We assume that all of the growth will come from renewables, mostly wind and solar. Electricity generation in the EU from coal and natural gas will have to be phased out in line with international commitments such as the Glasgow Climate Pact7.

Figure 2. Electricity generation in 2019, 2030, and 2050 in TWh

Note: RES = renewable energy sources.

Source: Bruegel (see Zachmann et al 2021).

The greater role of electricity will be visible in the future through more direct use of electricity in final energy use (‘electrification’, eg. of transportation) and through the introduction of hydrogen and synthetic methane produced from electricity (‘indirect electrification’).

Figure 3 shows that direct electrification will play a major role in all scenarios because it is a low-cost way of decarbonising many energy demand areas.

Due to their energy-inefficient production processes, hydrogen or synthetic methane will only become viable bulk-energy carriers if low-carbon electricity generation in Europe (or in the interconnected neighbourhood) turns out to be severely limited.

Even assuming learning and cost decreases, only small amounts of hydrogen and synthetic methane are no-regret decarbonisation solutions8 for sectors where electrification is impossible or hard to achieve.

Figure 3. Change in final energy consumption by fuel between 2020 and 2050 (TWh)

Source: Bruegel (see Zachmann et al 2021).

The scenario approach helps us to investigate the relative costs of each decarbonisation option. Clearly, there is too much uncertainty around key parameters (learning rates, future appliance costs, supply constraints, etc) to be able at this point to determine the optimal future energy system. However, some insights are gained from comparing the three scenarios.

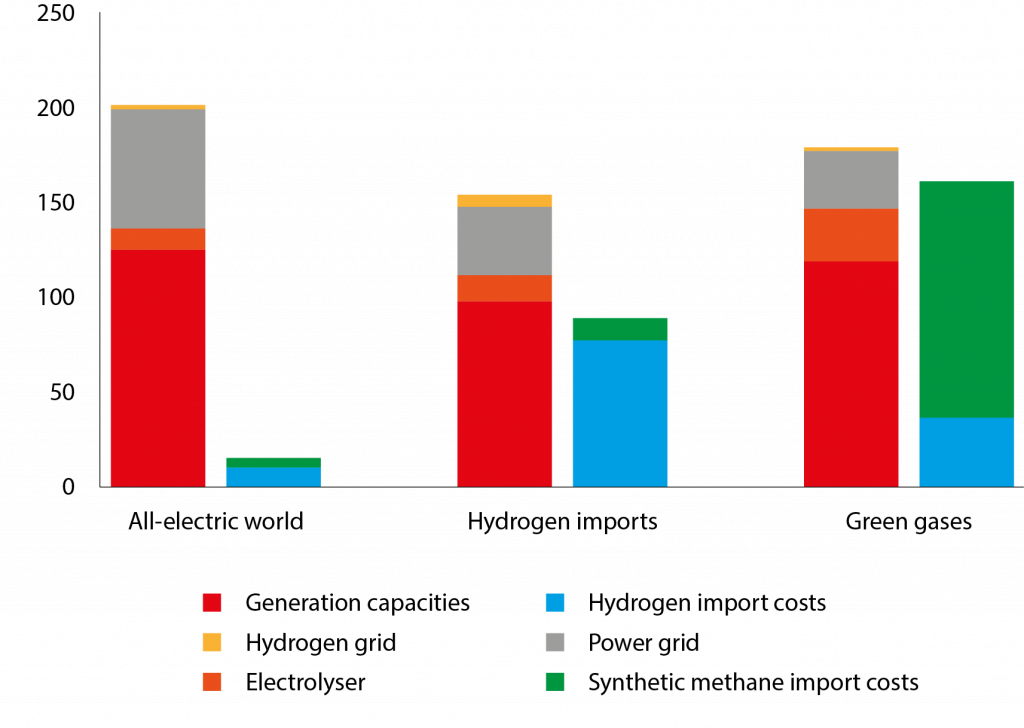

First, different scenarios have different investment needs (Figure 4). For example, the ‘all-electric world’ scenario with widespread electrification requires massive expansion of electricity grids, even more than in the other scenarios because of the interconnection of all possible demand areas.

In contrast, a hydrogen-focused energy system will incur costs for the retrofitting of pipelines to enable hydrogen to be transported.

Second, all scenarios require significant investment in low-carbon power supply. Expansion costs for low-carbon electricity generation are more than half the domestic EU investment costs in all scenarios.

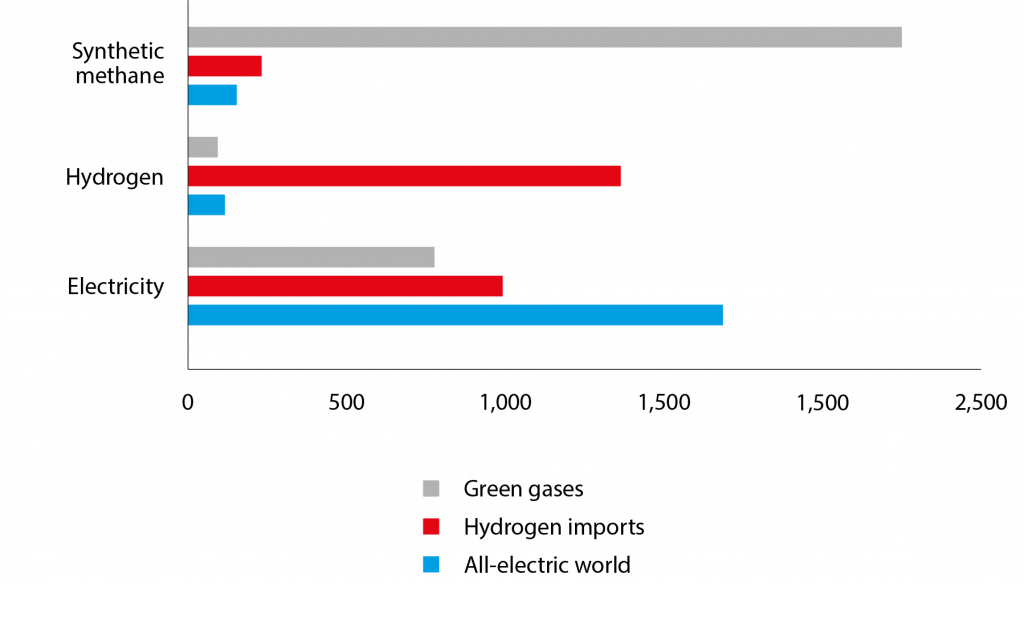

Third, the need for domestic generation investment would be even greater in the ‘hydrogen imports’ and ‘green gases’ scenarios, unless much of the electricity production is offshored and imported in the form of hydrogen and synthetic methane. This leads to high import costs (Figure 4).

Figure 4. Annualised investment costs (left-hand bars) and fuel import costs (right-hand bars) in the three scenarios, 2021-2050, € billions

Note: In each case, the left bar indicates the average annual investment cost and the right bar the annual fuel import cost.

Source: Bruegel.

In sum, electrification is a no-regret option across all three scenarios. In addition, the scenario focusing on widespread electrification has the lowest cost of the three scenarios. From a cost perspective, hydrogen use is more likely than synthetic methane use. Hydrogen can plausibly be a complement to widespread electrification, with hydrogen helping to decarbonise demand areas where electrification is hard or costly (eg. aviation).

An energy system biased towards synthetic methane would be the costliest choice. The advantages of re-using existing natural gas infrastructure would not compensate for the high investment and operation costs of synthetic methane production facilities.

3 Encouraging the needed private investment

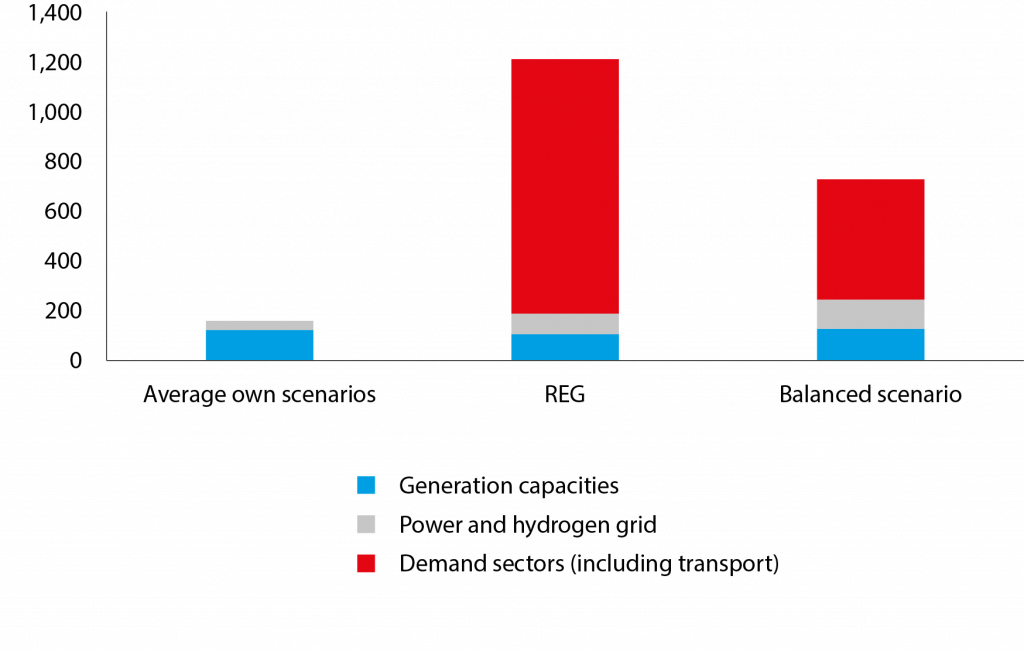

While our scenario analysis is focussed exclusively on the supply-side, previous modelling studies have shown that the vast majority of investment needs are on the demand side (Figure 5). Households must purchase clean vehicles and install clean heating systems, and firms must invest in clean production processes. Figure 5 shows that demand-side investment exceeds supply-side investment expenditures by a factor of at least five.

Figure 5. Required average annual investments (2031-2050)

Note: REG (regulatory-based) scenario comes from the European Commission (2020a); Balanced scenario is from Evangelopoulou et al (2019). All investments and costs are depicted in billions of 2020 €. Our scenarios do not consider demand-side investments.

Source: Bruegel.

In order to provide the private sector with sufficient confidence to make these investments, policy must pursue two complementary tracks. First, credible signals should indicate that the energy use of fossil fuels and the investment in the appliances that consume them will be relentlessly regulated out of the market. Simultaneously, policy should demonstrate that alternative low-carbon fuels will be available and cost-effective.

These policy tracks complement one another. Without convincing signals that fossil fuels will not be available in the future, investors will not be motivated to invest capital in switching, preferring instead to wait and see9. But announcing only fossil fuel phase-outs without credible commitments as to what new energy systems will be made available also will not work.

Social and political constraints imply that governments will ultimately never follow through on fossil-fuel bans or high carbon prices if no alternatives are in place to provide essential services (ie. governments will not permit household fossil energy bills to grow too large without alternatives available10).

3.1 Ending the use of fossil fuels

In our discussion on ending the use of fossil fuels, we differentiate between ‘neutral’ (no-regret) choices and policies that favour one of the described scenarios.

Technologically-neutral policies can contribute to ending the use of fossil fuels. These are policies that keep all pathways open and do not favour any clean fuel.

They include for example: greenhouse gas pricing, which increases the costs of carbon-intensive production, but is neutral about its alternatives11; bans on/strict standards for internal combustion engine vehicles and gas boilers, which phase out the use of fossil fuels but do not prescribe specific alternatives; and mandates to stop fossil-fuel investment that would only be economically viable if there is still unabated combustion after 2045, which do not prescribe a specific replacement technology.

However, such technology-neutral policies are not necessarily sufficient to end the use of fossil fuels, as shown by coal.

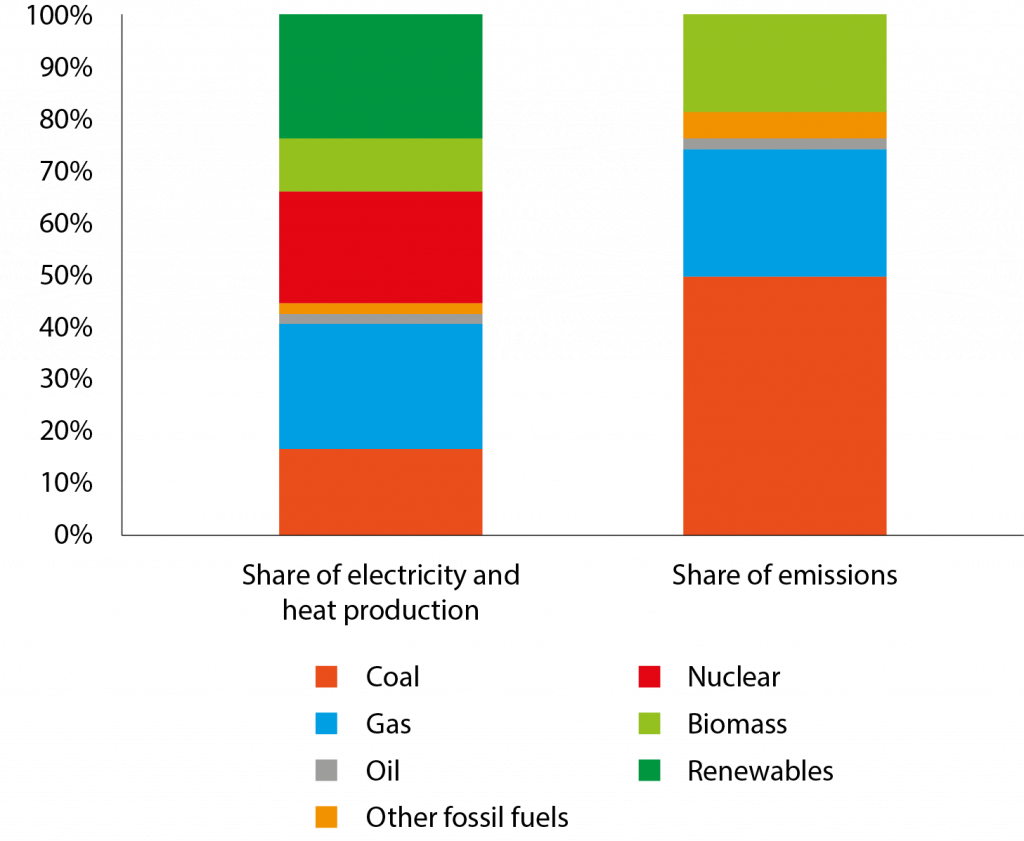

There exists no foreseeable future in which coal will play any (significant) role in the European energy system. Especially in electricity and heat production, which presently uses almost half of hard coal12 and almost all lignite in the EU, a coal phase-out must be achieved swiftly to not over-exploit Europe’s carbon budget and to maintain international credibility.

Using coal to generate electricity and heat is highly emissions-intensive: coal provides only 17 percent of total electricity and heat production in the EU, but generates half of the greenhouse-gas emissions in this sector (Figure 6).

Figure 6. Share of coal in emissions and electricity and heat production (2019)

Note: Renewables are without biomass and renewables waste; biomass includes renewables waste; ‘other fossil fuels’ includes non-renewable waste.

Source: Bruegel based on Eurostat (ngr_bal_peh) and EU CRF Tables reported to UNFCCC.

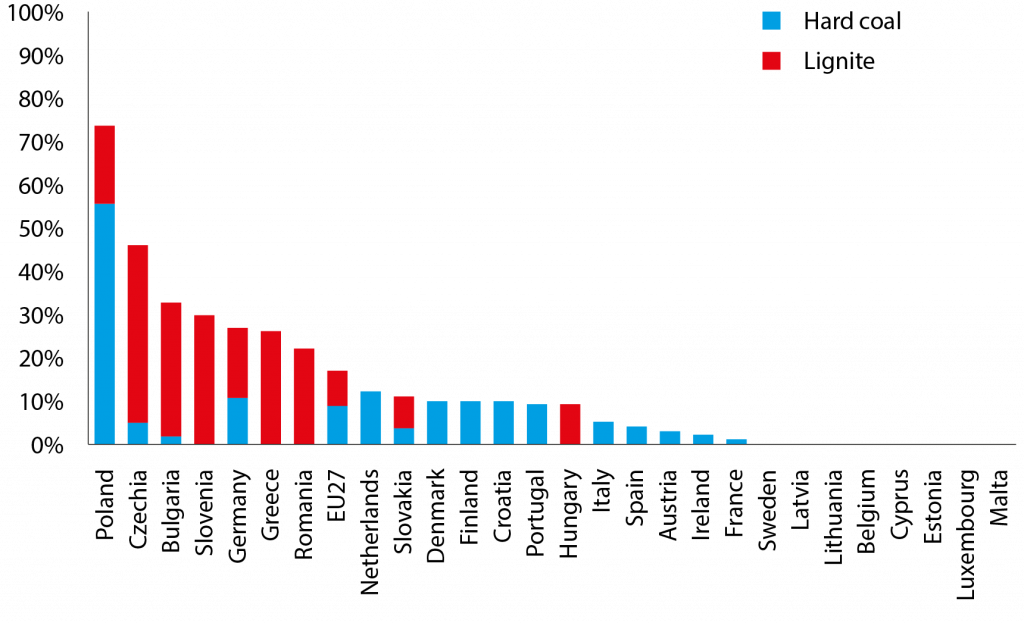

The importance of coal in electricity and heat production varies across the EU, with many countries – predominantly in North and West Europe – having no or almost no coal in their systems, and a few countries – in Central and East Europe – with very high shares (Figure 7).

Seven EU countries (Poland, Czechia, Bulgaria, Slovenia, Germany, Greece and Romania) have coal shares above 20 percent. On the other hand, twelve EU countries have shares around 10 percent. Germany has the fifth largest share of coal, but due to its size has the second-largest coal-sector in the EU.

Figure 7. Share of coal in electricity and heat production in the EU (2019)

Source: Bruegel based on Eurostat (dataset ngr_bal_peh).

Because of an annual reduction factor, the annual issuance of emission allowances into the EU emissions trading system (ETS) will continue to decline, reaching zero in less than 30 years. This provides a clear and powerful signal to national and regional administrations and companies that coal combustion will have to be phased out.

Regarding the short-term operation of existing coal plants, increasing carbon prices affect the equilibrium13 between coal, gas and electricity prices – incentivising a reduction in the operating hours of coal units.

In longer-term decision making, tightening emission budgets will not only prevent new-builds of coal assets but also encourage the early closure of existing ones.

However, if this process is left entirely to market forces and individual operators, the resulting closure schedule is likely to be inefficient. Political uncertainty over future policy direction, and notably the ability of large companies to influence this, implies that companies face some incentive to continue running coal plants at negative profit margins to avoid paying large decommissioning costs today.

In this case, a strict time schedule for phase-out is required to avoid the postponement of closure decisions. On the other hand, rapid and uncoordinated plant closures may threaten (regional) security of supply.

Therefore, a geographically determined phase-out schedule is crucial to manage the physical limitations of electricity grids as dispatchable generation drops offline. The need to manage the regional economic and social repercussions also calls for a planned phase-out.

Most EU countries already have national coal phase-out policies, usually with a phase-out schedule and a terminal date for coal-fired power plants. Only a few EU countries in central and eastern Europe do not have an end date (including Bulgaria, Slovenia, and Croatia), or have a very late end date (such as Poland, 2049, and Germany, 2038)14, for phasing out coal from electricity generation.

Finally, without a clear vision of publicly acceptable and competitive alternative power supplies, the phase-out plans are not credible. Here, public support for alternatives reduces the cost of the transition (eg. through accelerated learning) and also serves as a public commitment.

High carbon prices are thus an efficient driver of a coal phase-out, but can only be credible and hence successful if it is made sure realistic alternatives will be phased in at the same time.

3.2 Ensuring availability of low-carbon alternatives

Policy must focus not only on ending the use of fossil fuels, but also on providing credible low-carbon alternatives. To do so, certain actions are essential under all scenarios.

The first is to build out low-carbon electricity generation capacity. At least an additional 2,000 terawatt-hours of domestic electricity generation in 2050 compared to 2019 is required in all scenarios, which is approximately a 70 percent increase.

Second, in certain areas, direct electrification appears likely to be the optimal solution, including for passenger vehicles15, large shares of household heating16 and low-temperature industrial heat17.

Here, policymakers should be willing to do what is needed to provide the policy framework (infrastructure, regulation, support for research, development, demonstration and deployment) to enable the fast roll-out of decarbonised systems.

This does not imply that policy will blindly favour one system, but that the burden of proof will be on alternative technologies to provide not-yet-seen evidence of their superiority. Direct electrification will work for a substantial percentage of EU’s decarbonisation needs and this should be swiftly exploited.

The coal phase-out is a prime example highlighting the need for significant deployment of new low-carbon electricity capacity. The deployment record in the past two decades indicates that renewable electricity is the cost-efficient option18.

However, as wind and solar PV power plants have structurally lower full-load hours (hours in which the entire power capacity of a power plant is used), the overall capacity of the power plant fleet has to be substantially increased to provide the same amount of energy.

Among EU countries, the need to deploy renewable power plants in order to phase-out coal varies. Countries with a low share of coal in electricity and heat production will be able to replace coal with modest investments in additional renewable energy capacities.

Countries with high shares of coal (especially Poland, Czechia, Bulgaria and Slovenia) must invest aggressively in renewable energy capacities so they can phase-out coal in the next decade. Renewable capacities need to be multiplied by a factor of at least six by 2050 in the seven most coal-intensive EU countries (Figure 8).

However, all EU countries need to increase renewable energy deployment rates substantially to achieve climate neutrality by 2050.

Figure 8. Wind and PV power plant capacities needed for decarbonisation in the seven most coal-intensive EU countries (in GW)

Note: The data covers EU countries with significant shares of coal in electricity and heat production: Bulgaria, Czechia, Germany, Greece, Hungary, Poland, Romania and Slovenia.

Source: Zachmann et al (2021).

As the coal phase out progresses, gas-fired power plants could play an important transitional role. They have relatively low capital costs (about half that of coal plants) and can be dispatched more quickly than coal plants when needed to back-up fluctuating wind and solar PV power plants. They can thus support the system for the few days/weeks of the year when demand exceeds renewable energy production.

However, new gas power plants risk becoming stranded assets if they cannot be operated commercially under strict carbon-neutrality constraints.

Depending on the needs of the future power sector, three different types of gas fired power plant are conceivable: 1) plants with relatively low capital costs and low planned load factors, and which can be switched to carbon-neutral fuels such as synthetic methane or hydrogen; 2) plants designed to recover their fixed costs over a short period; 3) very efficient plants with higher load factors that can be commercially operated with carbon capture and storage.

Given the legacy power plant fleet and the decreasing cost of renewables, the first niche currently appears to be the largest. A predictable regulatory environment and a well-functioning electricity market is the best approach to identify efficient solutions.

Beyond these two uncontroversial solutions (direct electrification where appropriate and the massive deployment of renewable electricity generation), the most promising solutions for other energy uses (including significant industry applications, aviation or seasonal energy storage) are less clear.

Hence the approach should be two-pronged: to provide a European and national policy framework encouraging the rapid deployment of the uncontroversial solutions and encouraging companies to explore in depth different solutions in the less-clear areas.

In the next decade, this two-pronged approach will be particularly important for industry and households (including transport). In these sectors, emissions reductions have so far been too slow; in order to meet 2030 targets, a step change is necessary.

The major focus on these areas in the European Commission’s fit-for-55 policy push, and the spending plans of countries under Next Generation EU (Darvas et al 2021), reflect this. The policy challenge is to strike the right balance between allowing fair competition between low-carbon technologies while providing enough of a technologically-specific push for the required solutions to be deployed at scale in time.

For comparison, the 2005 launch of the EU ETS placed neutral pressures on the power sector to decarbonise, but was accompanied by the roll-out of massive support schemes for renewable power generation. These policies favoured the development of those renewable technologies that were already mature enough to compete for subsidies, and were very successful in dramatically bringing down their costs.

Without this complementarity, the ETS would have led to a stronger temporary switch from coal to natural gas, while increasing prices and dependencies might have undermined the political sustainability of European carbon pricing.

In a similar vein, policies to end the use of fossil fuels in industry and households19 must be accompanied by a second category of policies providing clear signals on the future availability of clean fuels.

This requires governments to make credible commitments to facilitate the necessary infrastructure for new fuels (both physical and institutional), which will be laid out through a series of path-nudging choices over the coming years.

First, access to energy will be determined increasingly by low-carbon sources of electricity and the fuels derived from this. Therefore, new infrastructure is essential to connect supply and demand of these energy vectors.

The signals sent by policymakers today regarding infrastructure roll-out provide a signal for private-sector investment (eg. greater electricity transmission capacity, roll-out of hydrogen transmission pipelines). We argue that bold decisions need to be taken today to stimulate a wave of new infrastructure investments.

This includes questions for policymakers outside the current comfort zone, such as: should competition concerns be temporarily ignored and should vertical integration of the generation, pipeline transportation and consumption of new green fuels be permitted, in order to allow nascent markets to grow quickly?

How can EU countries be made more cooperative and ambitious when constructing projects of common interest and transmitting clean fuels across borders? Beyond transmission-level infrastructure, there will also be a role for government support for/permitting of investments to reinforce distribution grids and final infrastructure, eg. charging for electric vehicles.

Second, energy markets are not self-organised institutions but are designed by policy. The current market design for electricity and natural gas reflects the ambition of gradually realising a European energy market by coupling short-term markets – and expecting that these price signals will ultimately lead to coordination of energy-sector investments in different EU countries.

But so far, national instruments to support specific technologies (eg. solar in Germany; nuclear in France; gas in Italy) have superseded European market signals. The net zero transition will require a substantial rethink about how investments are coordinated to result in an energy mix that is relatively efficient.

Most attention should be given to getting right the electricity market design and sector rules, as electricity will in any scenario be the most important future clean-energy fuel. But rules for other fuels also require a rethink. For natural gas, the main question is how to manage the phase-down with as little disruption as possible (eg. no uncontrolled death spirals of decreasing use and higher per-unit infrastructure cost).

Meanwhile emerging fuels such as hydrogen, which has historically been treated as a chemical input product, will have to be re-considered as a fuel.

Finally, political decisions, particularly on country-level agreements with third countries for the future import of green fuels, act as commitment devices. Signing such agreements sends a message that a government believes in a particular green fuel and is prepared over the coming years to back it through the different stages of production (or import), transport and consumption.

For example, Germany has signed a number of bilateral deals to import green fuels20. The volume of agreements suggests that Germany intends to emphasise imports in its future fuel mix. Choices will have to be made on the extent of the value chain exported.

Importing green hydrogen implies off-shoring the stages of electricity generation and electrolysis, while importing green ammonia or synthetic hydrocarbons implies off-shoring another stage of the value chain. Fuels that are the subject of political agreements are therefore revealing of the political perspective on the future domestic energy infrastructure.

4 Enhancing the transition toolbox

As Europe decarbonises, lessons must be learned to provide guidance to the later stages of European decarbonisation and also to third-countries that want to follow Europe’s path.

As a bloc of 27 countries with different geographies, economies and politics, there is likely to be significant divergence in the pathways EU countries follow to reach net zero. While coherence and collaboration in certain areas are important for efficient investments, in certain areas a diversity of approach should be celebrated.

The pursuing of different policies, and ultimately fuel mixes, by EU countries will provide important data on the pros and cons of respective pathways.

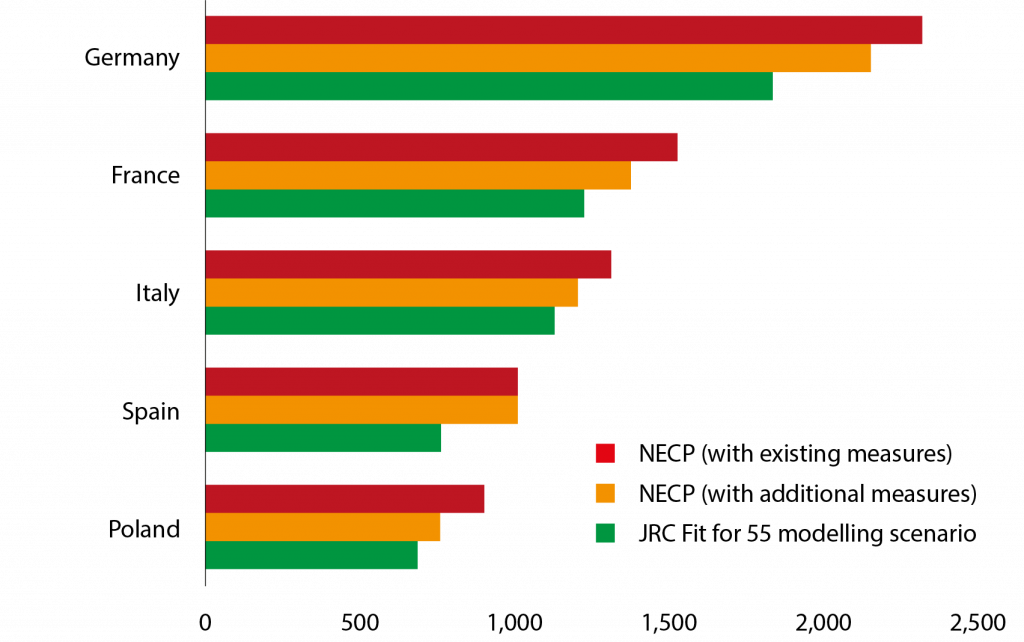

However, country-level plans must conform to minimum levels of ambition. So far, EU countries’ national energy and climate plans (NECPs) are insufficient as net zero pathways. For example, Figure 9 shows that NECPs consistently miss required energy efficiency gains.

Member states that will fall short in terms of energy efficiency gains must demonstrate that they are able to make up for this shortcoming with alternative policy, eg. more rapid deployment of renewable capacity.

Figure 9. Final energy consumption projections in 2030 (TWh), selected countries

Source: Zachmann et al (2021).

Finally, efforts should be made at EU and member state level to improve the collection and transparent communication of relevant data. Currently, NECPs are difficult to compare and not structured coherently.

The European Union should consider creating a European Energy Agency (similar to the United States Energy Information Administration), which would be responsible for detailed analyses of NECPs and all other aspects of the EU’s low-carbon energy transition.

The policies implemented over the coming years will fundamentally reshape the lives of every European citizen. A transparent reference point for the often very technical issues will be essential to ensure high quality political discussions.

Endnotes

1. See IEA, ‘Greenhouse gas emissions by source sector’ dataset, ‘energy’ value. Note this includes fuel combustion for power generation, transport and industrial applications. Measured in CO2 equivalent.

2. For simplicity’s sake, by ‘fuel’, we mean the three energy vectors of electricity, hydrogen and synthetic methane.

3. Full details can be found in Zachmann et al (2021).

4. The JRC (2018) estimated a “realistic biogas potential” of 18 billion cubic metres in Europe, corresponding to about 5 percent of current natural gas consumption; see Scarlat et al (2018).

5. Schiebahn et al (2015) explored the costs of synthetic methane production.

6. The efficiency of the process, from renewable electricity, via hydrogen and methanation, into the energy contained in methane is about 64 percent (Schaaf et al 2014).

7. See https://ukcop26.org/cop26-presidency-outcomes-the-climate-pact/.

8. To be precise, the term ‘defossilisation’ should be used instead of decarbonisation when describing a system with synthetic methane. Indeed, methane is a carbon-containing energy carrier. CO2 is emitted from its combustion and CH4 is a greenhouse gas itself, which might leak during transportation.

9. The IEA highlights this challenge when contrasting the required reductions in oil and gas investments in a net zero scenario with the required increases in clean energy and infrastructure. While the world appears on track for the former, it is markedly missing the latter (IEA, 2021).

10. While current European government subsidies are in response to high gas prices, they indicate the measures governments are willing to take in the case of high energy prices (Sgaravatti et al 2021).

11. In the EU, emissions of carbon dioxide, hydrofluorocarbons and nitrous oxide from large point-emission sources are capped and priced under the EU emissions trading system. Methane, another potent greenhouse gas emitted from coal mines and oil and gas infrastructure, needs to be limited too; see European Commission (2020b).

12. Half of the hard coal used serves as an input to industrial processes, which will be difficult to abate; however, technological alternatives are being developed.

13. This equilibrium is complex and non-linear and affected by many exogenous factors including electricity demand development, global energy market developments and public decisions to support/close other electricity generation assets, such as nuclear and renewables.

14. The 2021-2025 German coalition agreement states that the coalition wants to “accelerate” the phase-out and complete it “ideally already by 2030” (Koalitionsvertrag 2021–2025).

15. The share of electric cars in new registrations already reached 10 percent for the EU, Iceland, Norway, and the UK in 2020, and is increasing quickly, see European Environment Agency, ‘New registrations of electric vehicles in Europe’, 18 November 2021. The share is also above 10 percent for the global market; see Nathanial Bullard, ‘Electric Vehicles Are Going to Dent Oil Demand—Eventually’, Bloomberg Green, 9 December 2021.

16. For example, Flis and Deutsch (2021) explored clearly the financial benefits of heat pumps at household level.

17. Madeddu et al (2020) found that 78 percent of existing industry energy demand is electrifiable with existing technologies, while 99 percent of the demand is electrifiable with the addition of technologies currently under development.

18. The Lazard Levelized Cost of Energy Report shows significant cost-advantages for new-build solar and wind (Lazard, 2021).

19. For example, strengthening the ETS price, roll-out of second ETS/national-level carbon pricing, combustion-engine vehicle bans.

20. The European Commission in December 2021 approved Germany’s H2Global plan, which mobilises €900 million for investment in green hydrogen production in non-EU countries with the intention of importing into the EU. See https://ec.europa.eu/commission/presscorner/detail/en/ip_21_7022

References

Capros, P, E Dimopoulou, S Evangelopoulou, T Fotiou, M Kannavou, P Siskos and G Zazias (2018) Technology pathways in decarbonisation scenarios, ASSET Project, study for the European Commission, Directorate-General for Energy.

Darvas, Z, M Domínguez-Jiménez, A Idé Devins, M Grzegorczyk, L Guetta-Jeanrenaud, S Hendry … P Weil (2021) ‘European Union countries’ recovery and resilience plan’, Bruegel Datasets.

European Commission (2020a) ‘Impact assessment accompanying the document Stepping up Europe’s 2030 climate ambition: Investing in a climate-neutral future for the benefit of our people’, SWD(2020) 176 final.

European Commission (2020b) ‘An EU strategy to reduce methane emissions, COM(2020) 663 final.

Evangelopoulou, S, A De Vita, G Zazias and P Capros (2019) ‘Energy System Modelling of Carbon-Neutral Hydrogen as an Enabler of Sectoral Integration within a Decarbonization Pathway’.

Flis, G and M Deutsch (2021) 12 Insights on Hydrogen, Agora Energiewende and Agora Industry.

Götz, M, J Lefebvre, F Mörs, A McDaniel Koch, F Graf, S Bajokr, R Reimert and T Kolb (2016) ‘Renewable power-to-gas: A technological and economic review’, Renewable Energy 85: 1371–1390.

IEA (2021) World Energy Outlook 2021: Executive Summary, International Energy Agency.

JRC (2021) ‘Energy Scenarios – Explore the future of European energy’, Joint Research Centre, European Commission.

Koalitionsvertrag 2021 – 2025 (2020) Koalitionsvertrag 2021–2025 zwischen SPD, BÜNDNIS 90/DIE GRÜNEN und FDP.

Lazard (2021) Lazard’s Levelized Cost of Energy Analysis – Version 15.0.

Madeddu, S, F Ueckerdt, M Pehl, J Peterseim, M Lord, K Ajith Kumar, C Krüger and G Luderer (2020) ‘The CO2 reduction potential for the European industry via direct electrification of heat supply (power-to-heat)’, Environmental Research Letters 15(12).

Scarlat, N, F Fahl, J-F Dallemand, F Monforti-Ferrario and V Motola (2018) ‘A spatial analysis of biogas potential from manure in Europe’, Renewable and Sustainable Energy Reviews 94: 915-930.

Schiebahn, S, T Grube, M Robinius, V Tietze, B Kumar and D Stolten (2015) ‘Power to gas: Technological overview, systems analysis and economic assessment for a case study in Germany’, International Journal of Hydrogen Energy 40(12): 4285-4294.

Sgaravatti, G, S Tagliapietra and G Zachmann (2021) ‘National policies to shield consumers from rising energy prices’, Bruegel Datasets.

Zachmann, G, F Holz, B McWilliams, F Meissner, A Roth, R Sogalla and C Kemfert (2021) Decarbonisation of Energy: Determining a robust mix of energy carriers for a carbon-neutral EU, study requested by the ITRE Committee, European Parliament.

This article is based on Bruegel Policy Contribution Issue no01/22 | February 2022, which was written building upon a study prepared for the European Parliament’s Committee on Economic and Industry, Research and Energy (ITRE).